Market update

With sentiment around the CLARITY Act improving, crypto markets have continued to edge higher. The risks to the global economy from the war against Iran remain, but stock markets appear priced for perfection, and Kalshi now puts the odds of a US recession this year at just 17.5%. CoinShares reports the improved odds of CLARITY passing were likely the catalyst for a sixth straight week of inflows into global digital asset funds of A$1.18B/US$857.9 million.

Santiment notes that Bitcoin has just experienced the fastest decline in holders in nearly two years, losing 245,000 wallets in just five days. But it said capitulation was “one of the key ingredients to the beginning of bull runs” and that similar declines in the past have preceded the next leg up. CryptoQuant, meanwhile, believes Bitcoin is in profit-taking territory, with hodlers realising net profits of more than 20,000 Bitcoin over the past month. However, the firm believes the recent price action is more indicative of a “bear market rally” than the start of a new bull market.

Bitcoin finished the week up 2.1% to trade around A$112,625 (US$81,342), while Ethereum was flat at around A$3,228 (US$2,360). XRP gained 5.4%, having this week secured a A$276M/US$200 million credit facility to expand the lending capacity of its institutional prime brokerage business. Solana gained 13.2%, Dogecoin was flat, and Cardano increased by 12.4%. The Crypto Fear and Greed Index is at 49, indicating Neutral sentiment.

The past three weeks have seen one of the biggest reversals in US stock market history, with around A$10.8 trillion/US$7.8T added to the S&P 500, bringing it to its highest level on record. But spiking inflation and high energy costs are also increasing the odds of a financial crisis, depending on how long the Iran war continues. While the US blockade is successfully piling pressure on the Iranian government, and its oil storage capacity is nearing full, IRGC hardliners have taken charge of negotiations and seem ill-disposed towards compromise.

On the positive side of the ledger, a pro-crypto Federal Reserve chair, Kevin Warsh, could be confirmed this week, and a Who’s Who of administration officials are speaking at the annual Bitcoin conference in Las Vegas. There are also rumours of a major announcement regarding the US national Bitcoin reserve “in the next few weeks.”

Santiment reports that Bitcoin wallets holding between 10 and 10,000 Bitcoin have been “accumulating rapidly” over the past two weeks, snapping up 40,967 Bitcoin.

Bitcoin has neared the A$100K+/US$80K mark a couple of times this week, but quickly retreated. It finishes the week up 1.5% to trade around A$107,548 (US$77,264). Ethereum fell less than 1% to trade around A$3,210 (US$2,305). XRP lost 2.2%, Solana 1.1%, Cardano -0.5%, while Dogecoin clawed back 3.7%. The Crypto Fear and Greed Index is at 33, or Neutral, having recovered from just 8 at the start of the month.

Stocks rose back to record highs, and Bitcoin surged close to A$109,000 (US$78K) late last week after President Trump and Iran’s government declared the Strait of Hormuz open. But the IRGC quickly overruled the politicians and closed it again, with the outcome of negotiations to end the war later today likely to set the direction for markets this week. Despite rising tensions, Bitcoin is holding up well, thanks in part to Strategy’s massive Bitcoin buy, and it finishes the week up 1.8% to trade around A$105,616 (US$75,785). Ethereum processed a record high of 200.4 million transactions in the first quarter, but its sales pitch as the future of finance has taken a battering after a swathe of DeFi projects were caught up in the contagion from the KelpDAO hack. ETH finishes the week down 2.6% to trade around A$3,220 (US$2,311). XRP gained 3.2%, Solana fell 0.9%, Dogecoin gained 1.5%, and Cardano was flat. The Crypto Fear and Greed Index is at 33, or Fear.

Bitcoin and Ethereum both trended up significantly overnight. The just-implemented US blockade of the Strait of Hormuz could see a resumption of hostilities at any moment. The war has contributed to the University of Michigan index of US consumer sentiment falling to the lowest level recorded since 1952.

There are some promising signs, however. On-chain analyst Willy Woo reports “capital inflows into BTC just flipped positive, the first time since January.” Ash Crypto says an ETH weekly MACD (Moving Average Convergence Divergence) bullish cross has been confirmed and “the last 2 times this happened, ETH pumped 183% and 75%.” Ethereum also saw a record 3.6M daily transactions on April 12. But Michael Nadeau from the DeFi Report says he doesn’t see the conditions for a sustained turnaround just yet, with spot volumes at the weakest levels of the bear market and negative funding rates for perps on 30% of trading days so far this year.

Bitcoin finishes the week up 8% to trade around A$104,823 (US$74.3K) while Ethereum gained 11.8% to A$3,335 (US$2,365). XRP gained 3.2%, Solana was up 7.3%, Dogecoin (2.9%), while Cardano was flat. The Crypto Fear and Greed Index is at 21, or Extreme Fear.

Crypto markets rose this week, but seem unlikely to settle on a clear direction until the Iran conflict heats up or cools down. A potential 45-day ceasefire agreement looks unlikely at the time of writing, with Trump’s latest deadline for knocking out Iran’s power grid and bridges expiring later today. Bitcoin got a 2.5% bump on Monday after the last deadline was extended. Concern is growing about oil price-linked stagflation if the stalemate continues, but Citrini reports from a hotel overlooking the Strait of Hormuz that many more oil tankers – 15 per day – are getting through than previously believed. Bloomberg reports that some of the ships are paying tolls to Iran in crypto. Meanwhile, US manufacturing is looking healthier, with the US ISM manufacturing PMI coming in at 52.7%, which was above expectations of 52.5%. It’s the third month in a row above 52%, which has preceded big moves from stocks, gold and altcoins in the past. Bitcoin finished the week up 2.2% to trade around A$99,380 (US$68,722), and Kalshi prediction markets suggest Bitcoin is on track to reach A$108.4K/US$75K by the end of the month. Ethereum gained 3.7% to trade around A$3,052 (A$2,109). XRP, Cardano, and Dogecoin were flat, while Solana lost 3.4%. The Crypto Fear and Greed Index is at 11, or Extreme Fear.

Despite some ups and downs this week, Bitcoin is still trading around the same level it started the month. That’s a pretty solid effort considering there’s a war going on and the Crypto Fear and Greed Index has been stuck at Fear for 60 days. Almost half the supply is underwater at these prices, and around 40% of altcoins are near all-time lows. Depending on where the price heads today, Bitcoin may see its sixth monthly close in the red. Publicly, the White House remains committed to its six-week timetable for ending the war, which, if true, would mean the conflict winds up in a couple of weeks. If not, surging energy prices and long-term inflation could plunge many countries into recession

The world is in flames, trillions have been erased from stock markets, petrol prices are through the roof, and somehow Bitcoin is up almost 25% from the lows.

It’s a welcome change after a year in which everything seemed to be breaking all-time highs except for crypto. Bitcoin saw an unbroken week of daily gains and is up 8.3% this week to trade around US$74,312, while Ethereum raced ahead of the top ten, gaining 16.4% to trade around US$2,331.

Oil futures have been volatile amid conflicting reports around how definitive Iran’s closure of the Strait of Hormuz is. The US has bombed Kharg Island’s defences, a facility that accounts for 90% of Iran’s oil exports, and threatened to seize it in a game of tit for tat with unpredictable consequences. Until the oil supply situation is resolved, financial volatility seems set to continue.

In Australia, pundits have tipped that the Reserve Bank will increase interest rates. XRP, Solana, Cardano, and Dogecoin each gained between 11% and 13%. The Crypto Fear and Greed Index is at 28, which is still in fear territory, but finally heading in the right direction.

Global markets have had a tumultuous start to the week, with oil prices trading like a pump-and-dump memecoin. Oil prices gained almost 30% yesterday, trading at four-year highs, amid fears that the war in Iran will dramatically squeeze oil supplies through lower production and the closure of the Strait of Hormuz. Stock markets plunged, and NAB analysts warned Australian inflation could surge to 5% as a result. Bitcoin, however, held up well, leading some analysts to suggest the bottom is in.

But oil prices have subsequently reversed most of the surge and fallen back below US$90 a barrel. After G7 countries discussed releasing up to 400M barrels from their reserves to shore up supplies, it emerged that oil tankers are crossing the strait with transponders off and after President Trump told CBS, “the war could be over soon.” The Kobeissi Letter says this fits the Trump crisis playbook to a tee, although stopping a multi-country war is clearly a lot more difficult than walking back tariffs. We’re not out of the woods yet, with US jobs data suggesting the country lost 92,000 jobs in February, and oil prices remain much higher than a month ago.

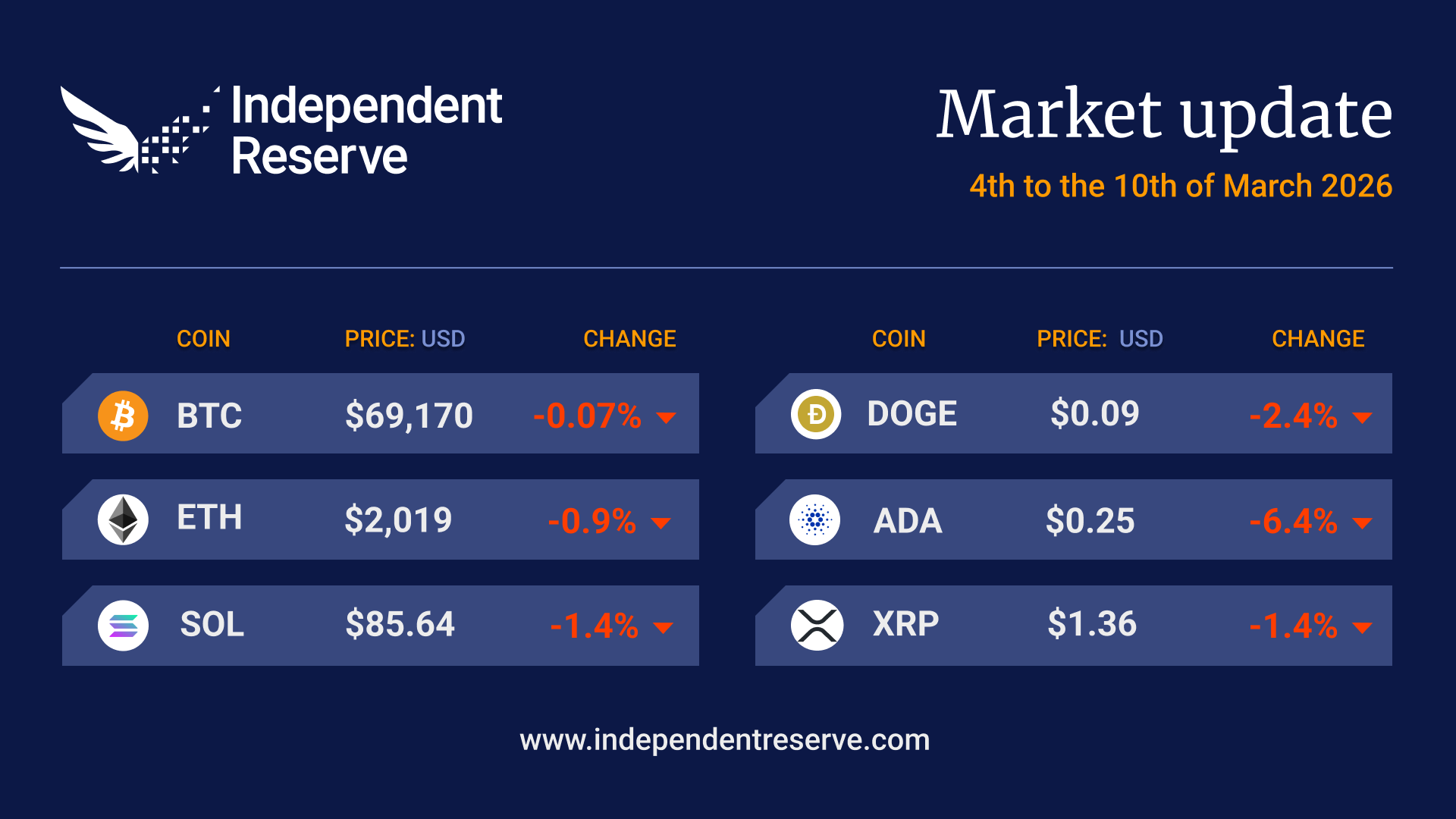

Bitcoin attempted a breakout above A$104K (US$74K) mid last week, but it didn’t hold. After all the drama, Bitcoin finishes the week pretty much where it began – around A$97,820 (US$69.1K). ETH fell by 1% to trade around A$2,856 (US$2,019). XRP lost 1.4%, Solana (-1.4%), Dogecoin (-2.4%) and Cardano (-6.4%). Strategy bought another 17,994 Bitcoin for A$1.8B (US$1.28B), in the largest acquisition since January, and the Crypto Fear and Greed Index is at 13, or Extreme Fear.

Bitcoin has held up well amid the conflict in the Middle East. While it fell sharply as news broke that the US was bombing Iran, it recovered fast, too. Bitcoin surged 5.9% overnight and is now trading above its pre-conflict levels. Analysts suggest the overnight move may be short covering by options traders rather than a decisive move to the upside. With the conflict set to last weeks, and the Iranians closing the Strait of Hormuz – a vital trade route for around 20% of global oil – risks are piling up.

The weekend’s conflict has highlighted the advantages of “non-custodial, always-on trading infrastructure”, as media began reporting on commodity price moves on Hyperliquid with traditional markets closed.

Prior to the Iran situation, Bitcoin surged 11.5% over a little over a day last week, providing hope that prices could recover as quickly as they had fallen. “Bitcoin is capable of making very big moves, very fast,” analyst Scott Melker observed.

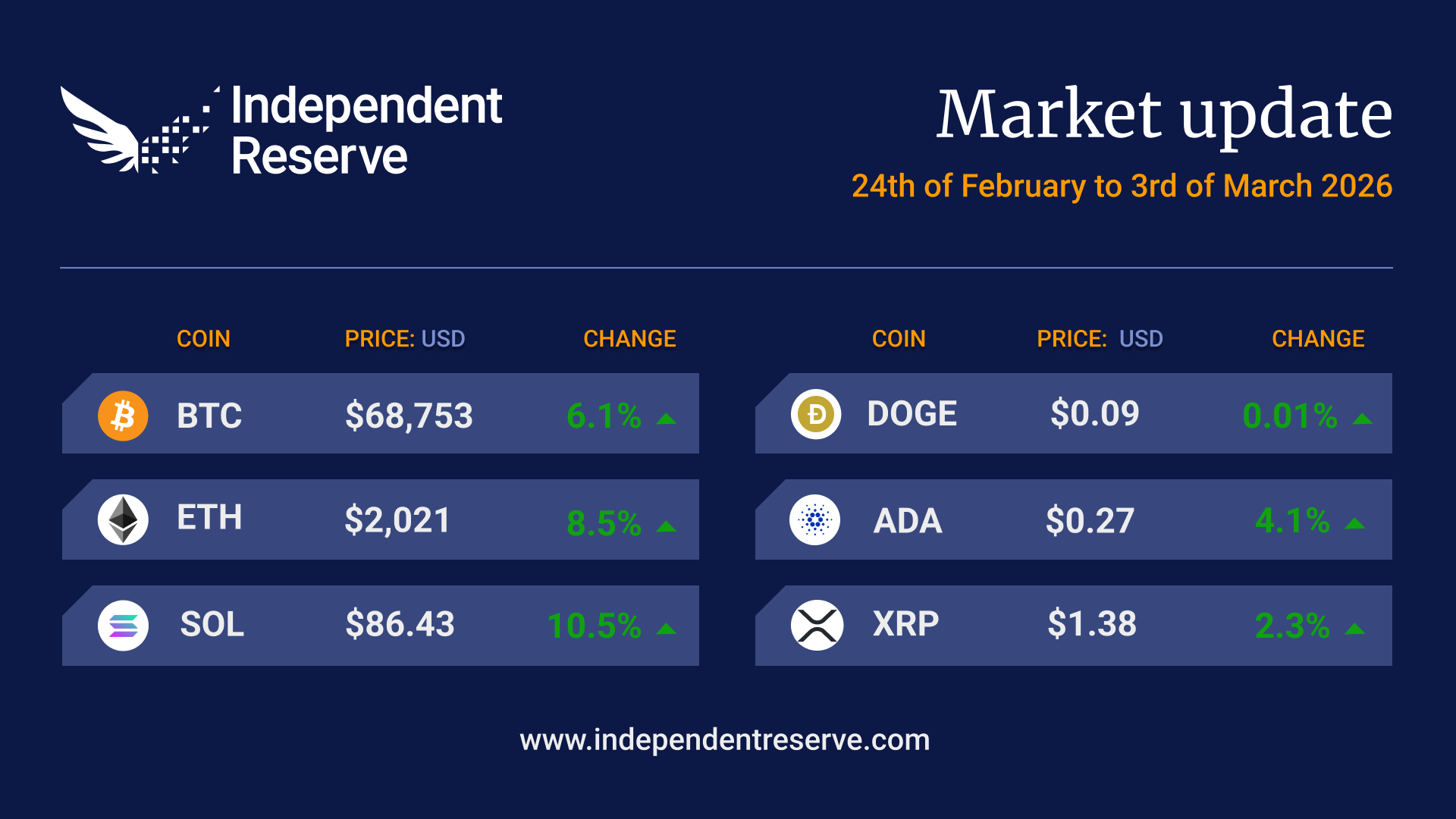

Bitcoin finishes the week up 6.1% to trade around A$96,928 (US$68,753) while Ethereum is up 8.5% to trade around A$2,852 (US$2,021) — but it has just marked six months in a row in the red. XRP gained 2.3%, Solana was up 10.5% and Cardano has overtaken Bitcoin Cash again by market cap, with a 4.1% gain. Both Strategy and BitMine added to their positions this week. The Crypto Fear and Greed Index is at 14, or Extreme Fear.