Market update

Oil prices have begun to ease after the Iran-US war descended once again into an uneasy stalemate. Polymarket suggests there’s now a 72% chance of a ceasefire by 31 August.

Bitcoin neared US$67,000 earlier in the week, but has finished down 2.6% on seven days to trade around US$63,609. Ethereum is down 1.2% for the week to trade around US$1,882, while spot Ether ETFs raised US$104 million last week, three times the US$33.9 million raised by Bitcoin ETFs. The ETH/BTC ratio continues to improve, up 1.7% this week and 13% this month.

Key US inflation data will be released this week, but the US Federal Reserve is expected to keep rates on hold for now. Some analysts believe crypto is starting to decouple from other risk assets, while others say the small rebound lacks the buying conviction typically seen ahead of genuine rallies. XRP was down 4.4% for the week; Solana fell 5.0%; Hyperliquid lost 10.1%; and Dogecoin was down 2.3%. The Crypto Fear and Greed Index is at 30, or Fear

Bitcoin has climbed back above US$65,000, despite the Iran war intensifying and the Houthis threatening to block another major oil shipping route.

A surprise fall in the US consumer price index helped restore confidence, even as oil prices rose again. CryptoQuant data suggests large holders added another 66,700 Bitcoin over the past 60 days, while mid-sized wallets sold. This pattern has shown up before previous rallies.

Spot trading on the world’s 10 biggest exchanges plunged 27.9% in the second quarter to US$1.95 trillion, according to CoinGecko. Figures from The Block show seven-day moving average volumes are now down 80% from the all-time high in October.

But sentiment is beginning to shift. JPMorgan analysts report there are “encouraging signs” for Bitcoin’s price, with increased institutional demand for Bitcoin futures and concerns over Strategy abating after it increased its cash reserves to pay dividends. The spot Bitcoin ETFs saw a second week of inflows, taking in US$75.7 million, while the Ether ETFs saw even more, taking in US$105.4 million.

Some big options traders are now betting billions that Bitcoin will climb to US$72,000 by the end of the month.

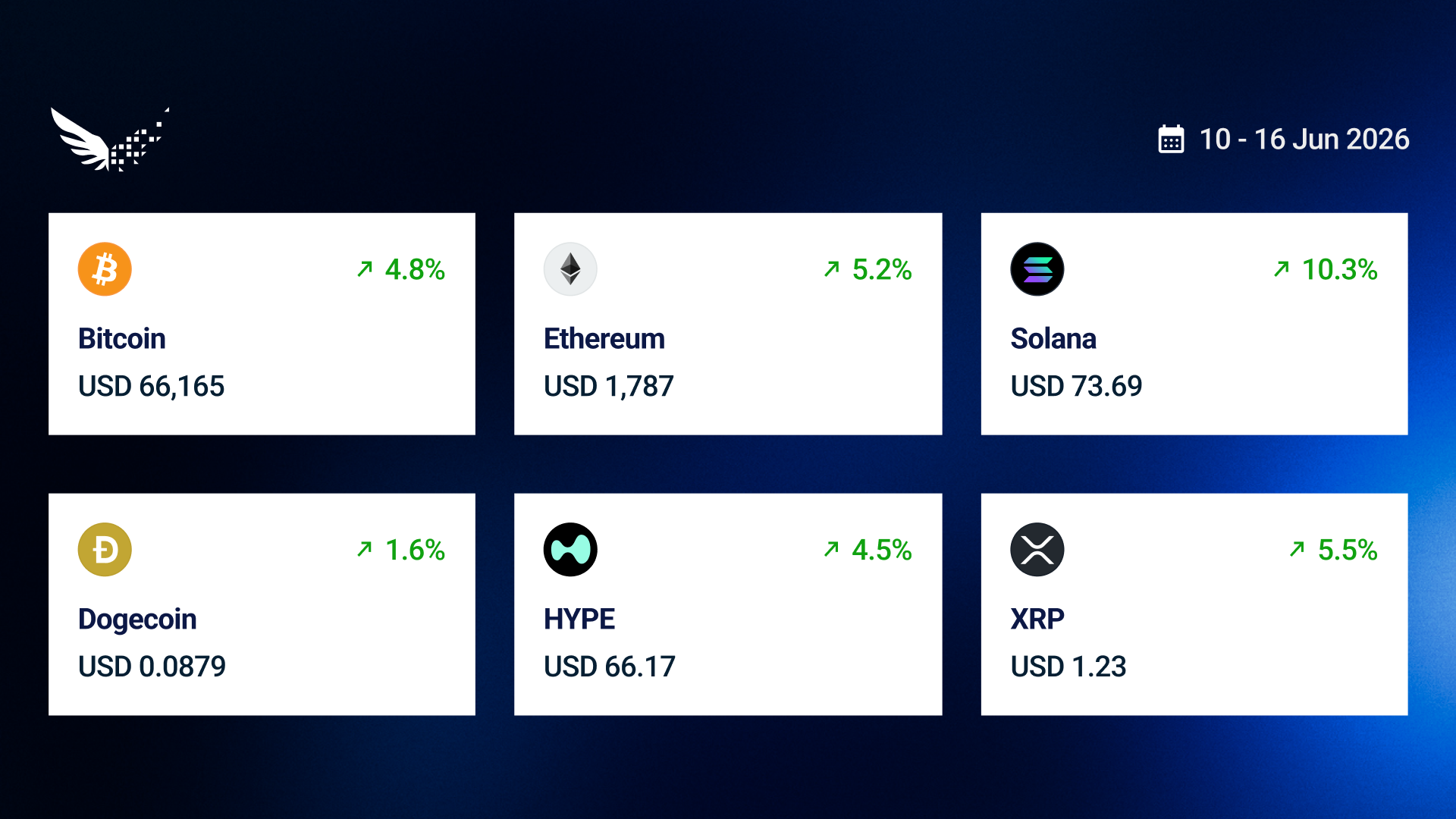

Bitcoin finishes the week up 5% to trade around US$65,214, while Ethereum gained 7.5% to trade around US$1,902. XRP, which has just gained a license to offer services across the EU, gained 4.7%, while Solana increased 4.1%. Hyperliquid lost 1.4%, and Dogecoin was flat. The Crypto Fear and Greed Index is at 25, or Fear.

There was a renewed sense of optimism in crypto markets this week. Bitcoin rose 10% in the month to date, marking the best July in four years, and the Bitcoin ETFs snapped an eight-week outflow streak, taking US$197 illion, while the Ethereum ETFs took US$84.42 million.

But storm clouds have also appeared, with the US Federal Open Market Committee’s meeting minutes discussing elevated inflation levels, and bond rates in Japan hit 30-year highs.

The US/Iran war has officially restarted, posing a threat to the global economy in the months ahead. Oil prices surged 9% after President Trump announced the US is reimposing the blockade and will charge its own 20% toll.

Bitcoin poked its head above US$64,000 a number of times, but had eased back to US$62,047 at the time of writing, to finish the week with a 3.3% fall.

Excitement around Robinhood Chain helped Ethereum post a smaller weekly loss, with ETH down 2.3% and trading around US$1,763. Open interest for Hyperliquid’s RWAs climbed to a record $3.6 billion, but HYPE itself fell 10.6% for the week. Solana lost 9.2%, XRP (-7.4%) and Dogecoin (-7.2%). The Crypto Fear and Greed Index is at 22, or Fear.

Crypto markets turned a corner this week, with the total market cap rising from US$2.06 trillion to US$ 2.21 trillion. Even with Strategy selling a few thousand Bitcoin, and a disappointing US jobs report, it does not appear to have dented the cautious optimism just yet, with Bitcoin gaining 6.5% this week to trade around US$64,098.

The move up came after Bitcoin’s realised profit and loss ratio fell to a 43-month low of -0.35, a figure that CryptoQuant said has historically coincided with market bottoms. The Bitcoin ETFs also flipped positive on Thursday for the first time since May, taking US$223.5 million, and there’s even renewed talk about a US Bitcoin Reserve, despite unresolved legal questions.

The ETH/BTC ratio recovered 6.6% over the week, after creator Vitalik Buterin announced the whole chain will be overhauled as Lean Ethereum. Ethereum finishes the week up 12.1% to trade around US$1,803, and some analysts believe it could push much higher if it can hold above the US$1,750 support level. Ethereum rejoined the world’s top 100 assets by market cap, just ahead of BHP.

XRP was up 8.4%, Solana gained 9.6% — with its 137.5 million daily transactions nearing 2026’s high water mark — Hyperliquid increased 6%, and Dogecoin gained 4.8%.

The Crypto Fear and Greed Index is at 27, or Extreme Fear.

With the ceasefire between the US and Iran looking shaky and crypto market sentiment hitting rock bottom, Bitcoin fell below the psychological US$60K mark this week but found support around US$58K and trended back up. It finishes the week down 6.5%, trading around US$59,765. Ethereum lost another 7.5% to trade around US$1,596, and was briefly overtaken again in market cap by USDT.

Crypto has erased around US$8.8 billion of value every day since the October high, with the overall market cap falling by more than 54%. Bitcoin also lost 18.2% in June, making it the worst month of the year so far. History suggests that every negative June since 2013 has been followed by a bounce in July.

CryptoQuant data shows that more than 550,000 Bitcoin were deposited on Binance and OKX after falling below US$60K, suggesting some investors are prepping for a fire sale if prices slip further.

But while short-term traders and TradFi have been selling in bulk, on-chain indicators suggest long-term holders have been accumulating.

Altcoin investors remain at max pain levels, with analyst Michael van de Poppe pointing out that the altcoin market cap has erased all gains since 2023. “No wonder the markets are completely utter garbage in terms of sentiment,” he said

XRP lost 7% this week, Dogecoin fell 11.5%, but Solana gained 3.9%. The Crypto Fear and Greed Index is at 15, or Extreme Fear. A slew of US manufacturing and jobs data comes out this week, which could impact markets.

Crypto gained ground after the shaky US-Iran negotiations concluded with a roadmap to a permanent deal and progress on the nuclear issue. The US Federal Reserve has kept interest rates on hold, but the prospect of rate rises later this year has weighed on markets.

Tech stocks fell on Monday, with SpaceX erasing more than Ethereum’s entire market cap, but the Russell 2000 small-cap index is now trading at all-time highs. This has traditionally been a strong indicator for crypto, but there’s little sign that’s happening this time around.

Concerns over Strategy’s STRC eased overnight, as the company bought more Bitcoin and added A$429M/US$300 million to its cash pile to pay dividends. The bleeding from Bitcoin ETFs also slowed considerably this week, but they still saw A$323M/US$226M in outflows.

Glassnode summed up the week’s price action as volatile but range-bound, with the “market caught between fading momentum and underlying strength, awaiting its next directional catalyst.”

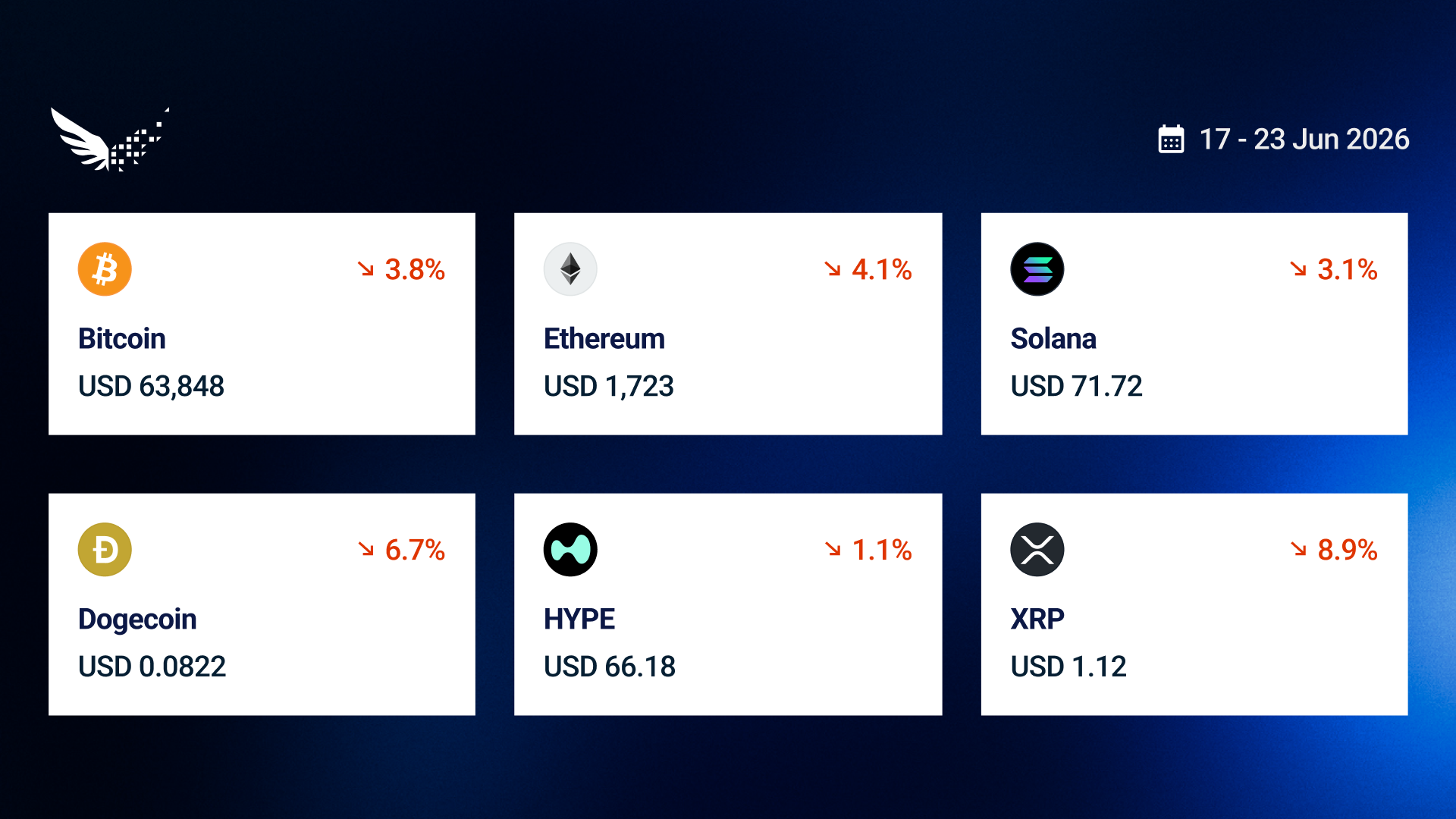

Bitcoin and Ethereum are both at risk of notching up a third consecutive negative quarter. Bitcoin finishes the week down 3.8% to trade around A$91,292 (US$63,848) while Ethereum lost 4.1% to trade around A$2,465 (US$1,723). XRP was down 8.9%, Solana fell 3.1%, and Dogecoin lost 6.7%. The Crypto Fear and Greed Index is at 23, or Extreme Fear.

The collapse of the US-Iran peace talks, along with news that Michael Saylor had committed heresy by selling some of Strategy’s Bitcoin, sent BTC prices down almost 4% in 24 hours. President Trump says the ceasefire will likely be extended following moves to dampen the conflict between Israel and Hezbollah, but hopes of a speedy resolution are fading.

Even as crypto prices tank, the S&P 500 and Nasdaq are hitting record highs, with the Shiller PE ratio at 42.78 — the highest reading since just before the dotcom bubble popped.

Large outflows from Bitcoin ETFs suggest “institutions aren’t just reducing exposure, they’re doing it urgently and at scale,” according to Glassnode. But crypto analyst Maartuun says smart money buyers may see value, with a “short-term relief rally looking increasingly possible.”

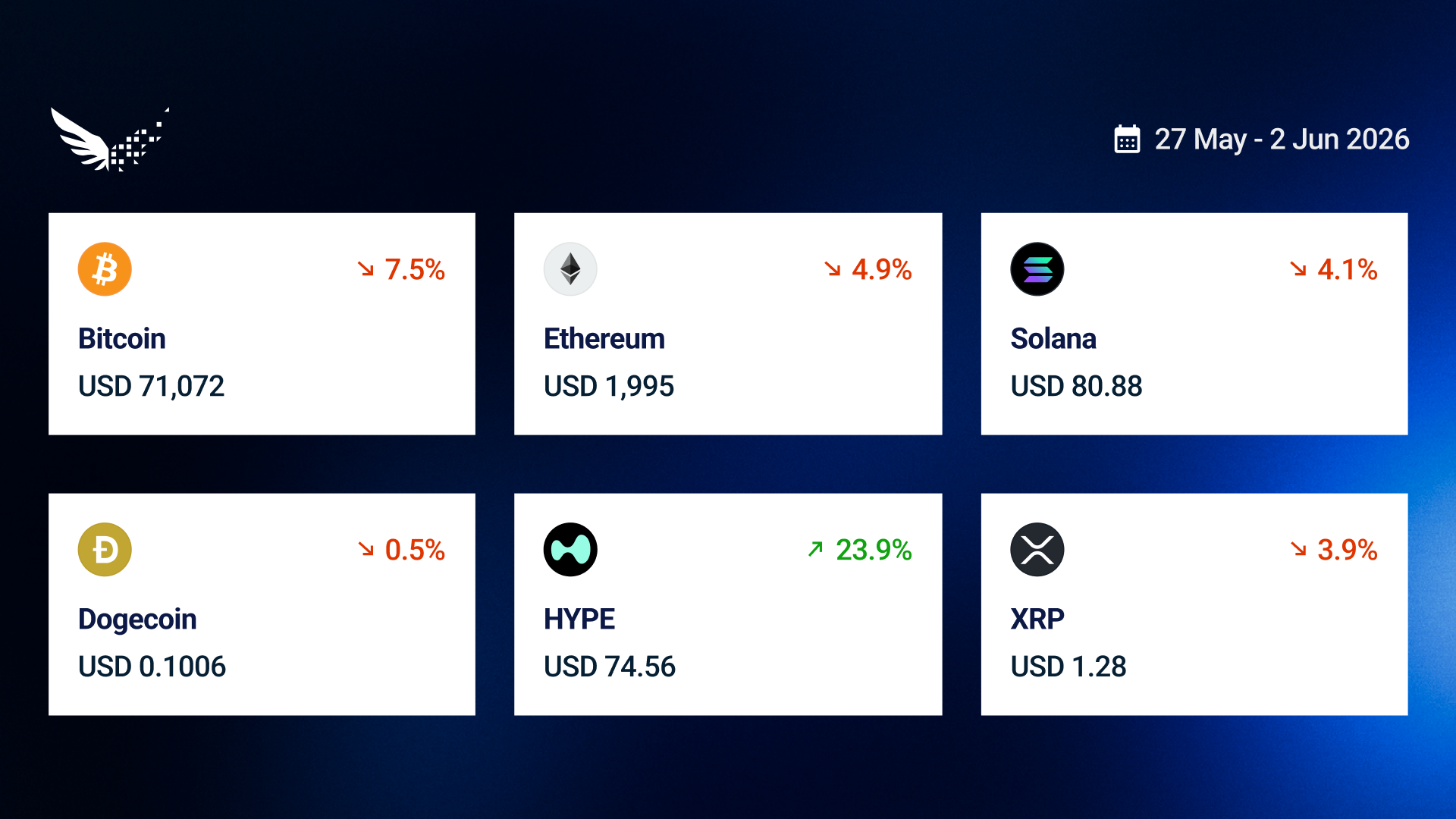

Bitcoin finishes the week down 7.5% to trade around A$99,294/US$71,072, while Ethereum lost 4.9% to trade around A$2,793/US$1,995. Bitcoin’s dominance has fallen to 59.25%, with altcoins trading at their highest relative levels since the October crash. Hyperliquid is the biggest winner and is now firmly ensconced in the top 10 with a 23.9% gain this week, thanks to healthy ETF inflows. Solana lost another 4.1% this week and has seen its eighth consecutive month in the red, while Cardano dropped 5.2% and now languishes at No. 17. XRP lost 3.9%, and Dogecoin fell 0.5%. The Crypto Fear and Greed Index is at 23, or Extreme Fear.

With sentiment and transaction volumes tanking, Bitcoin fell to A$104.1K/A$74.2K over the weekend, before taking the express elevator back up to A$108K/US$77K on hopes of a peace deal between the US and Iran.

We’ve been here before, though, and the agreement still only has a 36% chance on Polymarket of being finalised this month.

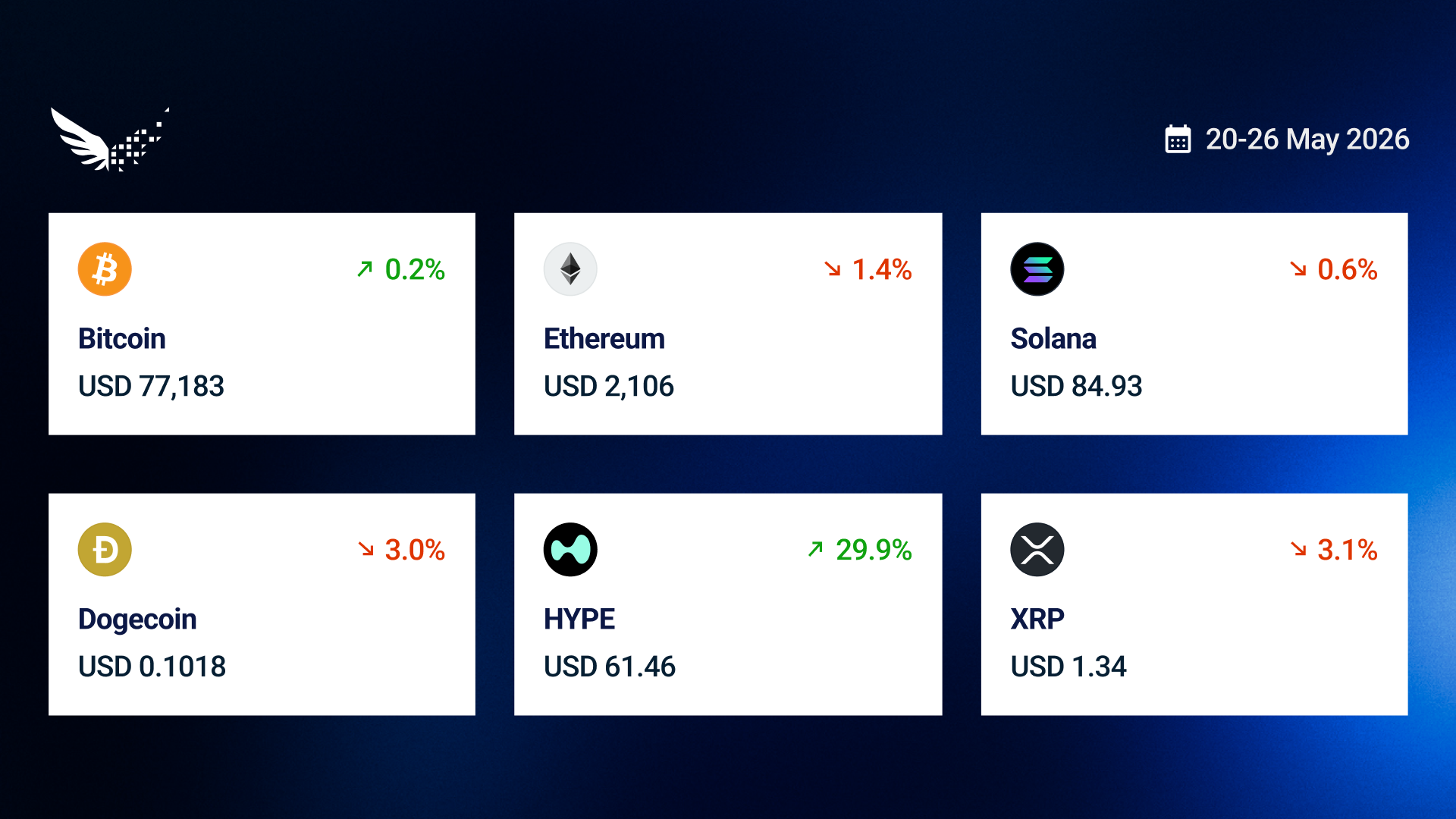

The spot Bitcoin ETFs shed A$1.75B/US$1.26 billion in outflows last week, and the Ether ETFs racked up ten straight days of outflows. CryptoQuant reports Bitcoin demand has fallen to its most bearish level this year, but Glassnode sees signs of “stabilisation” and notes long exposure is increasing. Cycle theory proponents warn of a fall to A$75K/US$54K, with at least three months of bear market left. Bitcoin ended the week flat at A$108,058 (US$77,183).

The ETH bears grew louder this week, but Ether only dropped 1.5% to trade around A$2,948 (US$ 2,106). XRP transactions over A$/1.4M/US$1M fell by 57% in the past week, and the price eased by 3.1%. Solana was flat, Dogecoin fell 3%, and a debate over Cardano’s valuation sent its price down 3.4%. The Crypto Fear and Greed Index is at 34, or Fear.