Bitcoin and blockchain technologies have received a lot of press coverage in recent times, and it is important to understand the relationship and differences between the two.

In this article, we aim to explain and demystify some of the key concepts underpinning these technologies.

What is Bitcoin?

Bitcoin is a Digital Currency and a peer-to-peer payment network. Transactions are verified by nodes on the network and stored on a global, public ledger called the blockchain.

A bitcoin refers to a unit of account on the blockchain. It is a digital currency created and held electronically, that is produced by people running specialised computers all around the world. This creation process is referred to as ‘mining’ and consists of using computing power in the distributed network to solve mathematical problems. The mining process is very computationally intensive, and it is what provides security for all the transactions on the Bitcoin network.

Bitcoin is decentralised and completely transparent thanks to the Bitcoin blockchain, which stores details of every single transaction that has ever occurred on the network. There are many free websites available online where anyone can inspect and view any transaction which has ever taken place on the Bitcoin network.

Bitcoin was created in 2009, by a pseudonymous programmer (or group of programmers) known as Satoshi Nakamoto. Satoshi’s true identity has never been verified. However, as Bitcoin was released to the world as ‘open source’, it is possible for any skilled programmer to work and contribute to Bitcoin. Currently there are hundreds of programmers around the world collaborating with each other to further improve and enhance the capabilities of Bitcoin.

Let’s dive a little bit deeper into some of the key concepts behind Bitcoin.

How does a Bitcoin transaction work?

Bitcoin transactions rely on well-established computer science concepts such as peer-to-peer networking, cryptographic hashing and public-key cryptography to securely and reliably broadcast private data across a public network. These technologies are very similar to those used in other familiar areas such as SSL, the scheme behind the https protocol, which secures the vast majority of electronic commerce that happens online.

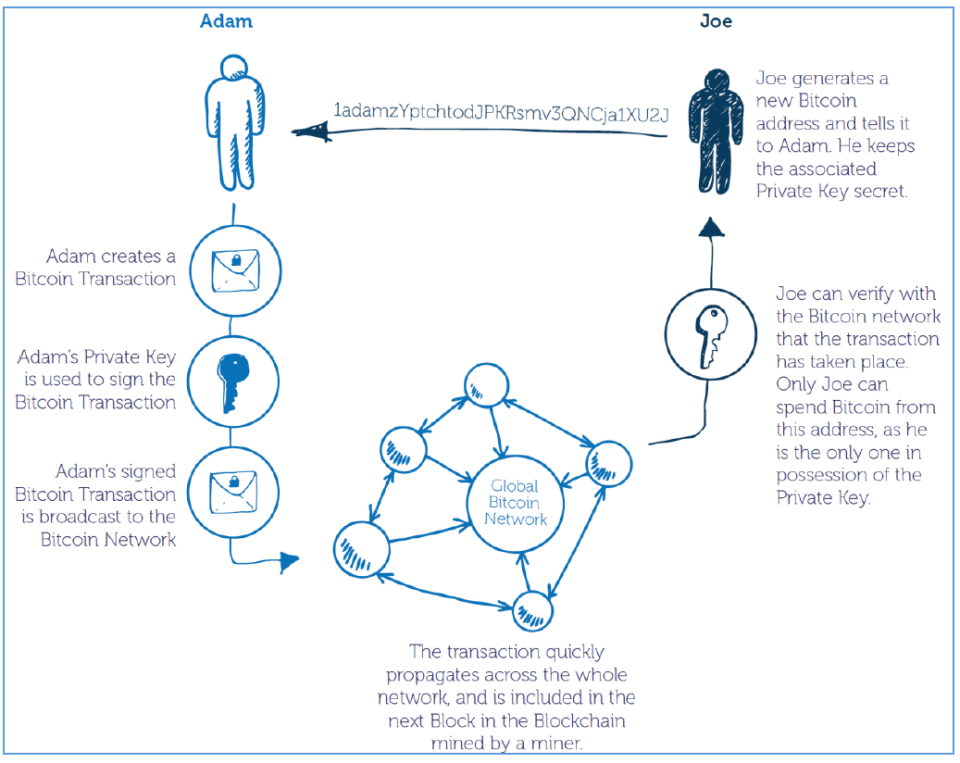

A Bitcoin transaction is initiated by a person using a Bitcoin wallet, which is a piece of software that can run on a computer or a phone. There are many free wallets available to choose from. A wallet stores the private key which is used to verify that the person who created the transaction is the owner of the bitcoin that are stored at a specific address on the blockchain, and is therefore authorised to spend the bitcoin.

The diagram below illustrates an example Bitcoin transaction from Adam to Joe:

It is important to note, that because Bitcoin is global and based on the internet, the physical locations of the participants in the transaction are irrelevant. Adam and Joe could be in the same room, or they could be on the opposite ends of the world and in either case the transaction would still occur almost instantly and settle on the blockchain within a matter of minutes.

How is bitcoin generated?

Most traditional payment systems rely on a central authority to provide security and settlement of transactions. Since Bitcoin has no central authority, it relies on a process called mining. Mining refers to the process of grouping newly incoming transactions into what is known as a ‘block’, and then repeatedly attempting to add a random piece of data to this block, known as a ‘nonce’ which then produces a cryptographic hash which meets certain pre-defined criteria. Although this process sounds complicated, the important take away is that anybody can freely participate in it, and due to its computationally intensive nature it provides security to transactions on the network without the need for a central authority to verify the authenticity of transactions.

Although the software used for Bitcoin mining is free, the process itself is expensive. It requires the miner to invest in computer hardware and pay for the electricity needed to run this hardware.

To entice people to mine bitcoin, the Bitcoin network provides an incentive for people to participate in mining. This incentive is in the form of a reward for the successful mining of a block, as well allowing the miner to collect all transaction fees which were specified in the transactions which were included in the mined block. Bitcoin transaction fees are optional, but they ensure that a transaction is included in a block in a timely manner.

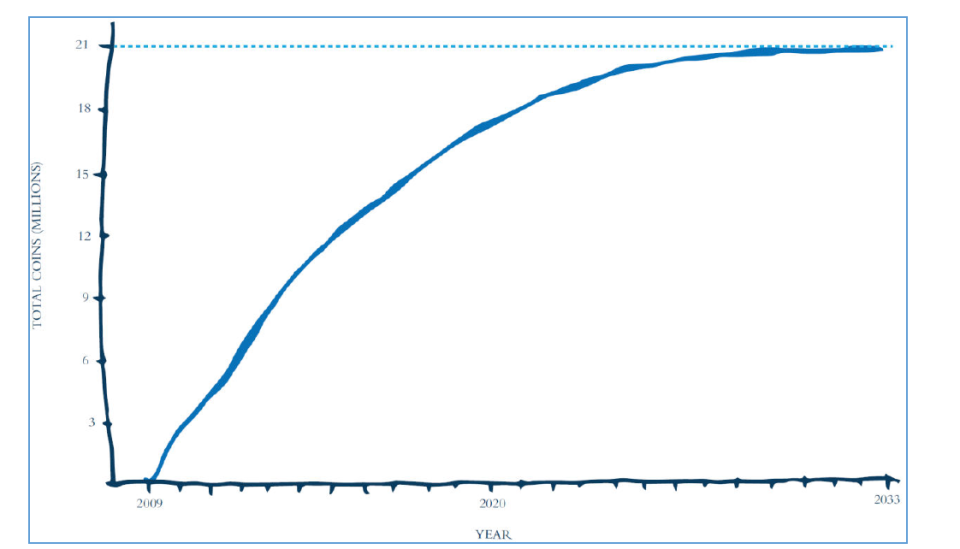

The ‘block reward’ which the miners receive is the only way in which new Bitcoin can be generated and added into the Bitcoin economy. The reward amount is designed to halve approximately every four years until the amount of Bitcoin in circulation reaches 21 million in approximately the year 2140. At the time of writing, around 16.2 million Bitcoin have been mined.

What is the blockchain?

The blockchain is a distributed public ledger, which stores every transaction that has ever occurred on the Bitcoin network.

The blockchain is created by the miners. Every time a new block is mined, it is appended onto the blockchain, with a link onto the previous block and then broadcast across to everybody on the network. Thus, every node participating in Bitcoin can have their own full copy of the blockchain, enabling anybody the check the validity of any transaction. The structure of the blockchain ensures that all published transactions are immutable and cannot be tampered with or altered. It is essentially the ‘settlement layer’ of Bitcoin.

The immutability of the blockchain allows for many uses, completely separate to the Bitcoin Digital Currency. There are innovative companies right now attempting to use the blockchain for applications such as identity verification, asset trading and smart contracts.

There has also been great interest from banks and financial institutions looking to utilise blockchain technology to create more efficient settlement networks and potentially replace and improve upon existing systems such as SWIFT, which currently underpins the majority of international wire transfers.