Market update

Bitcoin briefly topped the A$105.4K/US$70K mark earlier today, but is yet to convincingly break out above. We’ve been consolidating in this region since March, albeit with some dips below A$90K/US$60K. Bitfinex analysts suggest that long-term holders’ selling was a key reason for Bitcoin’s retreat from all-time highs, but on-chain data suggests these holders have begun to reaccumulate. The amount of Bitcoin and Ethereum on exchanges has fallen roughly 10% this year to historically low levels. Unfortunately, Bitcoin’s active addresses are also at five-year lows. Bitcoin finishes the week flat at A$102,495 (US$69,037), while Ethereum lost 2.8% to trade around A$5,582 (US$3,772). Most other coins eased back a little: Solana fell 5%, XRP (-2%), Dogecoin (-6%), Cardano (-2%) and Shiba Inu (-3.5%). The Crypto Fear and Greed Index is at 73 or Greed.

The past week was arguably one of the most historic for crypto in a decade, with SkyBridge Capital’s Anthony Scaramucci summing it up as “a big year this week in crypto.” Pro-crypto legislation passed with bipartisan support in the US House of Representatives, the Ethereum ETF was approved, and Donald Trump promised to defend crypto from critic Elizabeth Warren and her “goons.” It suggests a sea change in crypto’s political fortunes and is a potential catalyst for the second stage of the bull run. Bitcoin topped the A$106K (US$70.6K) mark earlier today but at the time of writing the price was flat on seven days ago to trade at A$104,210 (US$69.5K). Ethereum gained 6.9% over the past week and is trading around A$5,839 (US$3,883). The ETF approval appears to have taken some of the gloss off of ETH killer Solana which pulled back 8.4%, and ETH competitor Cardano (-6.1%), XRP was flat, Dogecoin gained 2.5%, and Shiba Inu was flat. The Crypto Fear and Greed Index is at 74 or Greed.

Crypto markets surged this morning after reports the SEC may actually approve an Ether ETF this week. At the time of writing Bitcoin was up 13% for the week to A$106,790 (US$70.5K) and Ethereum was up 24% to A$5,535 (US$3,661) — however markets were rising fast. Everything else was up including Solana (26%), XRP (6%), Dogecoin (9.6%), Cardano (14%) and Shiba Inu (9.1%). The Crypto Fear and Greed Index is at 76 or Greed.

It was a choppy week for Bitcoin, with the Orange Coin trading between A$97.2K (USD$64K) and A$91.4K (US$60K), with sudden lurches either way. FxPro trader Alex Kuptsikevich warns that Bitcoin could see a panic sell-off if it closes under A$90.8K (the psychological US$60K mark) in the coming days, with traders looking for a break above A$98.3K (US$65K) to signal bullish conditions have returned. All eyes will be on the release of April’s US inflation data this week, with analyst Seth saying “Jerome Powell likely pump our bags” if inflation trends lower. Bitcoin finishes the week down 1.1% to trade around A$94,765 (US$62,752), while Ethereum lost another 4.5% to hit A$4,443 (US$2,942) amid waves of negativity from rivals and expectations of an ETF denial. Solana lost 4.7%, XRP (-7.1%), Dogecoin (-5.6%), Cardano (-4.2%) and Shiba Inu (-3.5%) The Crypto Fear and Greed Index is at 57 or Greed.

After a dismal few days in which Bitcoin plunged to A$87.5K (US$56.8K) as flows to the Bitcoin ETFs dried up and inflation fears surged, everything took a sharp turn for the better on Saturday. Bitcoin rose 5% off the back of cooler-than-expected US jobs numbers, easing inflation and interest rate fears. Bitcoin has just notched up one billion transactions, the 200-day moving average has just hit a new all-time high, and the ETFs broke a long streak of outflows with hundreds of millions added on Friday. Former Bitmex CEO Arthur Hayes believes we’ve seen the local bottom, and he predicts range-bound price action between US$60K and US$70K (A$90K to A$106K) until August. Bitcoin finishes the week relatively flat at A$95,182 (US$63.5K), while Ethereum lost 3.9% over the week to trade around A$4,620 (US$3,081). Solana gained 13.1%, XRP was up 5.1%, Dogecoin (9.4%), Cardano and Shiba Inu were flat. The Crypto Fear and Greed Index is at 71 or Greed.

A renewed assault on crypto by US authorities has seen markets flag, and April’s negative return is on track to be Bitcoin’s worst month so far this year. MicroStrategy has again bought the dip of course. Bitcoin finished the week down 4.8% to trade around A$97,411 (US$63,906), while Ethereum was flat at A$4,904 (US$3,217). It was a sea of red elsewhere with Solana down 13.1%, XRP (-7.8%), Dogecoin (-27.7%), Cardano (-12.2%) and Shiba Inu (-11%). The Crypto Fear and Greed Index is at 67 or Greed.

This week saw another mini crypto crash, with Bitcoin dropping to around A$94K (US$60K) as Israel struck back after Iran’s attack. However, prices recovered, and it became clear Iran did not want to escalate further. The region remains on a knife edge, though, with any escalation able to turn markets on a dime. Traditional markets were also hit, with concerns that the conflict would pump energy prices, which would hit interest rates and inflation. Bitcoin finishes the week up 6% to trade around A$103,455 (US$66,900) in the wake of Saturday’s halving, while Ethereum gained 4% to trade at A$4,967 (US$3,213). Everything else was up, including Solana (16%), XRP (13%), Dogecoin (1.1%), Cardano (13%) and Shiba Inu (24%). The Crypto Fear and Greed Index is at 73 or Greed.

Visions of a crypto-funded retirement got pushed back a little this week after the prospect of interest rate cuts in the US this year began to dim, and markets sold off due to tension in the Middle East. That was before Sunday morning’s 8.4% BTC plunge when news broke that Iran had launched a slow-motion attack on Israel. Despite being the largest deleveraging event since mid-2023, Glassnode analyst Checkmate says it “looks a lot more like your garden variety correction” than the start of a new bear market. With the immediate threat of escalation diminishing, and crypto ETFs approved in Hong Kong, markets began to recover. Bitcoin is currently 12% down on a week ago and trading around A$98,750 (US$63,193), while Ethereum lost 17% to trade around A$4,804 (US$3081). Solana lost 24%, XRP fell 25%, Dogecoin (-21%), Cardano (-25%) and Shiba Inu (-24%). The Crypto Fear and Greed Index is at 74, or Greed.

Even after the US Government spooked markets by moving US$2 billion (A$3B) in Bitcoin confiscated from Silk Road, BTC finished the week up 2% to trade at A$107,796 (US$70,939). Ethereum had a sudden surge overnight to A$5,584 (US$3,680), finishing up 6% on seven days ago. Did ETH just bottom out after falling below the 0.05 BTC mark for the first time since 2021? Who knows, but options data suggests there’s potentially another A$454 (US$300) of upside by the end of the month. Solana pulled back 1%, while XRP and Shiba Inu were flat, and Dogecoin reversed by 1.5%. The Crypto Fear and Greed Index is at 76, or Extreme Greed.

Bitcoin closed out the month and the quarter above US$70K (A$107.6K) for the first time — that’s higher than the 2021 peak. The halving is less than three weeks off, and the stars are aligning for the bulls. However, this cycle is very different, with Bitcoin hitting a peak prior to the halving for the first time, and the usual rotation into ETH and altcoins apparently skipped in favour of degens trading memecoins. Bitcoin finished the week down 1% on seven days ago at A$107,570 (US$69,753), while Ethereum eased back 2% to A$5,388 (US$3,500). Solana gained 1%, XRP dropped 5%, Dogecoin gained 15.7%, and RektCapital believes it’s now in a “macro uptrend.” The analyst also predicts a bright future for Shiba Inu (-1%). April is usually a good month for crypto prices, with Bitcoin’s historical increase averaging 14.03% while ETH usually increases by 23.97%. The Crypto Fear and Greed Index is at 79, or Extreme Greed.

Bitcoin has been on a rollercoaster ride lately. It dropped sharply from its recent all-time high but rallied 10% mid-week on news of three potential US interest rate cuts this year. Then it fell to near the A$93K (US$61K) level following a week of outflows from the Bitcoin ETFs, recovered slowly and suddenly surged back above A$108K/US$70K overnight. Santiment reports that almost 52K Bitcoin was accumulated by wallets holding 10-10K Bitcoin on Sunday US time alone. One swallow does not a Summer make, but Rekt Capital is already musing about whether the surge marks the end of the traditional “Pre Halving Retrace “, which would make it -18% this cycle compared to -19% in 2020. At the time of writing, Bitcoin was up 5% on seven days ago to trade at A$107,729 (US$70,433), while Ethereum gained 5% to trade at A$5,541 (US$3,622). Solana pulled back 2%, Avalanche lost 6.3%, XRP and Cardano gained 2%, and Dogecoin gained 22.7%. Independent Reserve has just listed Shiba Inu, which gained 7.1% this week. The Crypto Fear and Greed Index is at 75 or Greed.

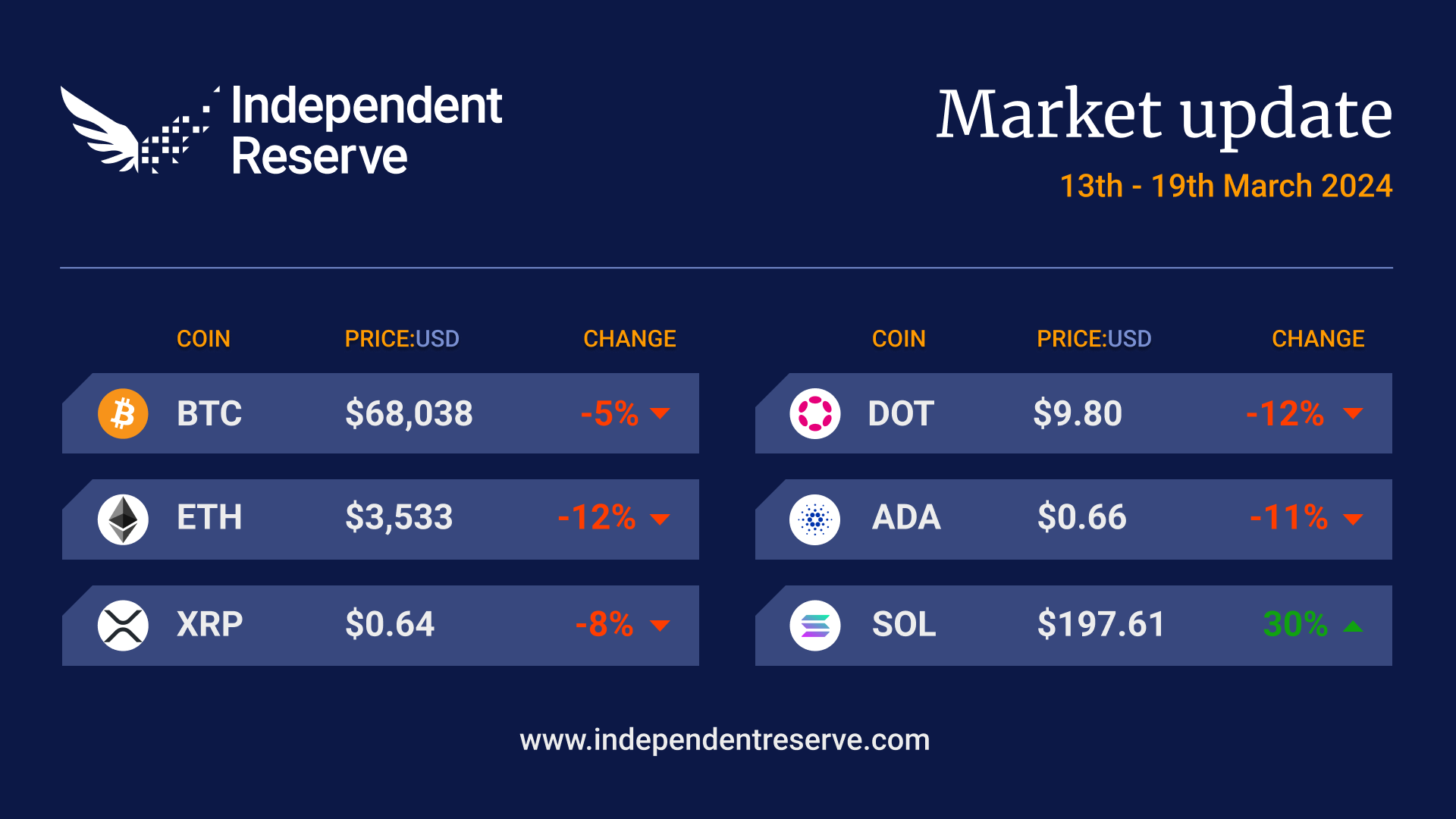

Bitcoin pulled back 5% this week — but remains up 31% over the past 30 days and is currently trading at A$103,770 (US$67.6K). Ethereum fell 12% to trade at A$5,388 (US$3,517) despite the network’s Dencun upgrade reducing fees to sub-cent levels. Part of the issue was that Solana’s soaring activity and price saw social media users comparing it very favourably to ETH’s slow and expensive L1, rather than ETH’s cheap and fast L2s. Solana surged 30%, hit a record-high market cap, and is now the fourth-largest cryptocurrency. XRP lost 8%, Cardano fell 11%, Avalanche gained 25%, and Dogecoin lost 19%, even though Elon Musk said Telsa plans to add it as a method of payment at some point. The Crypto Fear and Greed Index is at 77, or Extreme Greed.