In Markets

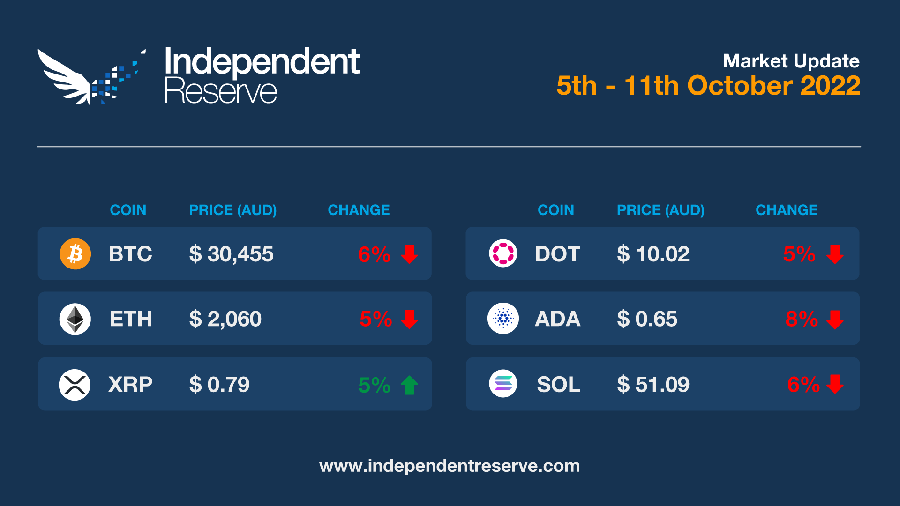

The S&P 500 has been on one of the longest slides in history and has dropped 24 weeks of the year in 2022, putting it second only to 1931 when it dropped for a total of 33 weeks (five years have seen worse total losses). Given all that, crypto isn’t doing too badly: Bitcoin dropped just 3.11% in September while the S&P 500 lost 9.34% and the Nasdaq lost 10.5%. It also outperformed most other asset classes throughout Q3. Bitcoin finishes the week 5.5% down at just over A$30,400 (US$19.15K) and Ethereum is down 5.4% to A$2,060 (US$1.3K). XRP gained 4.7%, Cardano lost 8%, Solana lost 5.9% and Polkadot -4.5%. In good news the total supply of Ether dropped 0.02% (annualised) in the past week, and we are 60% of the way to the next Bitcoin halving which historically always provides a bullish narrative. The Crypto Fear and Greed Index is at 24, or Extreme Fear.

From the IR OTC Desk

Risk assets continue to drift lower on the back of robust US economics data and coordinated OPEC+ supply restrictions.

Last week we highlighted the importance of the US labour market data: specifically, the job opening data (JOLTS) for August; the ADP employment change for September; and the US Non-Farm Payrolls and unemployment rate for September.

Despite falling from 11.117 million job openings in July to 10.053 million job openings in August, job openings in the US remain historically high. It must be noted that the JOLTS economic release is one month lagged and appears to be falling rapidly. The FOMC has previously communicated a willingness to close the ratio between active job seekers and job openings in their attempt to return inflation back to the 2% policy target.

ADP (non-farm private employment in the US) surprised to the upside, with 208k private jobs being created in September versus 185k in August. In last Friday’s Non-farm payrolls series, 263k jobs were created in September, relative to a market expectation of 250k. Additionally, the unemployment rate moved back to 3.5% in September versus 3.7% in August. In terms of wages growth, Average Hourly Earnings continue to remain highly elevated, growing at 0.3% MoM and 5% YoY (September). The US labour market remains highly resilient to monetary tightening.

In commodities, OPEC+ have lowered their oil production target by 2 million barrels per day – circa 2% of global consumption! This has resulted in the US Congress preparing a consultation on energy prices and anti-competitive behaviour. US Treasury secretary (and former Fed Governor) Janet Yellen stated that the ‘decision is unhelpful and unwise’ and may become an issue for ‘developing countries and the problems they face’.

In New Zealand, the Reserve Bank (RBNZ) has increased their underlying cash rate by 50bps to 3.5%. With core inflation in New Zealand being at a very similar level to Australia (where the RBA have most recently slowed their pace of cash rate increases) the RBNZ are taking a different path in policy assessment – continuing to tighten aggressively. The topic of conversation at the RBNZ meeting, as derived from the Meeting Statement was whether a 50bp or 75bp increase would be most appropriate. This hawkish rhetoric suggests that the RBNZ has more tightening in store.

On the OTC desk, volumes remain day dependent, and devoid of consistency. With cryptocurrencies continuing to perform well against other high beta assets – it is important to qualify that cryptocurrency performance has been relative and not outright. The reality has been stable price action, as BTC and ETH have maintained above key support – USD $18k for BTC and USD $1,200 for ETH. This has resulted in BTC and ETH vol. nearing the low of the historical range. With macroeconomics continuing to drive price action, we turn our attention this week to US CPI on Thursday.

For any trading needs, please don’t hesitate to get in touch.

In Headlines

Glass half full

Bad news can be good news according to Santiment, which has done extensive backtesting and found that the more positive the social media sentiment is about an asset, the less likely it is to rise. Conversely the more the crowd thinks something is dead and buried the more likely it is to go on a run. That’s good news then for Solana, TRON and BNB as, according to Santiment, social media hates them right now.

Bitcoin mining to expand

According to Arcane Research, publicly listed Bitcoin miners plan to expand their hashate by 50% by the end of the year. That would make their capacity around 80.7 EH/s out of around 250 EH/s. Arcane cautions however that miners often overestimate their ability to get new mining equipment online. With the hashrate already at an all time high, difficulty has just been increased by 13.55%. Mark Morton, CEO of Scilling Digital Mining said the adjustment “suggests that miners are still finding sufficient profit margins to turn on new machines and are likely capitalising on plummeting machine prices.””

MICA gets the nod

Ambassadors for 27 European Union member states have given approval to the Markets in Crypto Assets Regulation bill which prohibits stablecoins not denominated in euros that have a supply greater than 200M euros or more than 1 million transactions. Tether, USD Coin and Binance USD are already way above these levels. The wording could still change and the Parliament needs to vote on the legislation, expected in December or early next year.

ZK EVMs launching

Hold on to your hats because ZK EVMs are about to launch and supercharge the Ethereum network. The layer two solutions use zero knowledge proofs (also known as validity proofs), which can securely rollup thousands of transactions into one transaction on ETH. And because they are almost totally compatible with existing Ethereum DApps, there’s little friction for projects to port over. Polygon launched its zkEVM testnet this week, while zkSync launches its mainnet at the end of the month. zkSync is already looking to test out recursive scaling on Layer 3 – which is where “infinite” scaling becomes possible. They each have hundreds of millions in funding to help realise their visions.

12K zombie coins

According to Nomics more than 12,100 cryptocurrencies recorded no trading volume at all for at least one month this year. Bloomberg described these currencies as “zombies” as they’re not “dead technically” but “not quite alive either.” In 2018’s crypto winter the figure was 136, which increased to 766 in 2019, 1500 in 2020 and 3700 in 2021.

38 Metaverse users

Widely shared data suggests that there were just 38 daily active users in the US$1.3B (A$2.06B) Decentraland metaverse on October 8. The similarly valued The Sandbox had 522 users on the same day. ‘Active users’ refers to those making a transaction, and the devs say Decentraland attracts about 8,000 total users just having a look per day. The highest number of users making a transaction was 675, while on the Sandbox it was just over 4,500.

Solana to be fixed

Solana saw another partial network outage this week but co-founder Anatoly Yakovenko says a fix is on the horizon in the form of a second client called Firedancer. It’s a separate team with separate code so it’s unlikely to have the same bugs at the same time. It’ll take one to two years to complete though. But it turns out Ethereum has not had 100% uptime either. Cofounder Vitalik Buterin said: “Technically the chain was unavailable for very-gas-heavy applications for a week or two during the 2016 Shanghai DoS wars, and an accidental 12-hour chain split happened a month later due to a consensus bug.”

Bitcoin whales bounce off bottom

In late September Bitcoin whale holdings hit a 29-month low of 45.72% of BTC’s circulating supply. The good news is there has been a big turnaround since, with whales embarking on their longest sustained accumulation streak since May, gobbling up around 46,173 BTC (US$884M/A$1.4B) since September 27.

Until next week, happy trading!