Market update

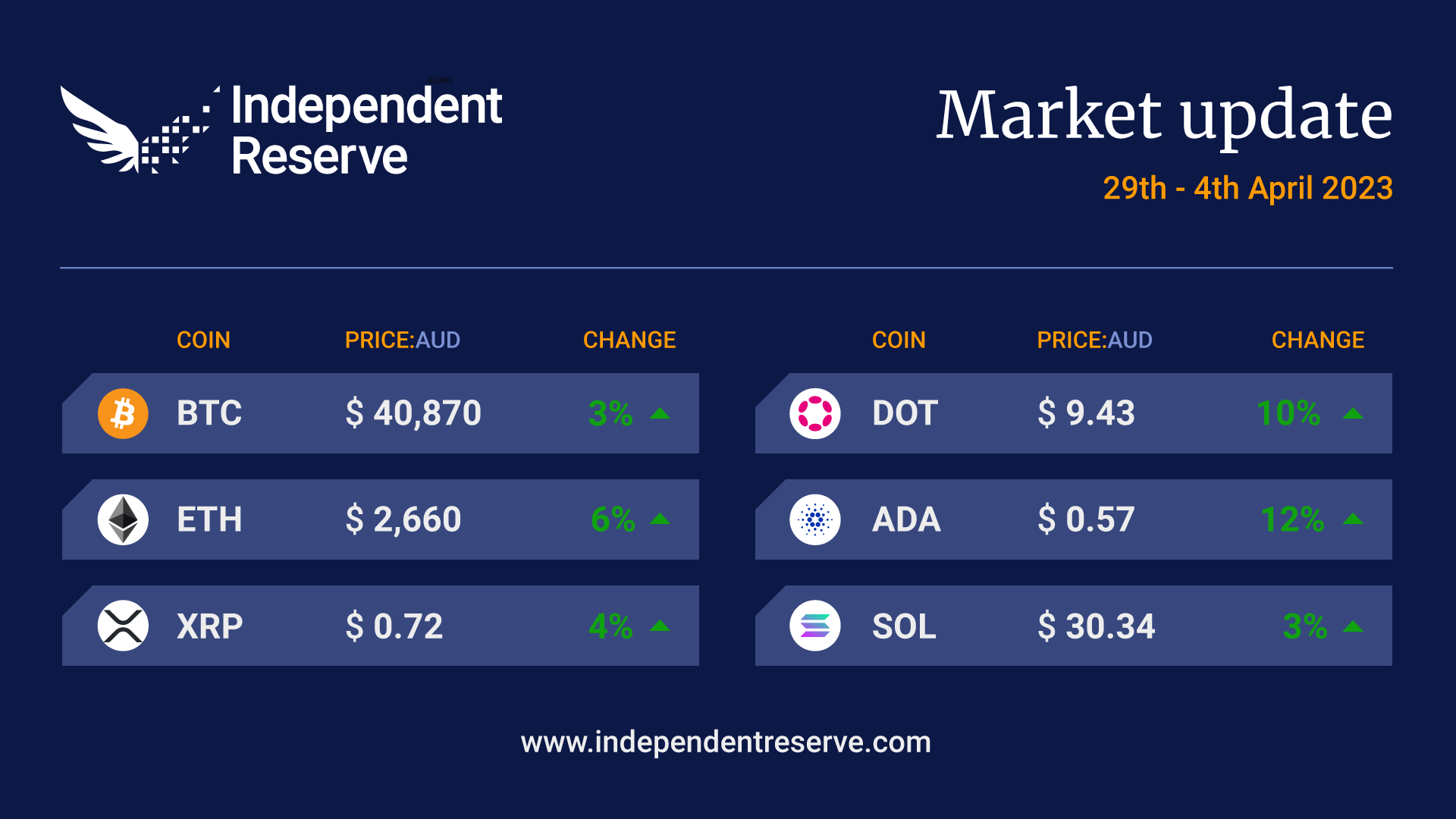

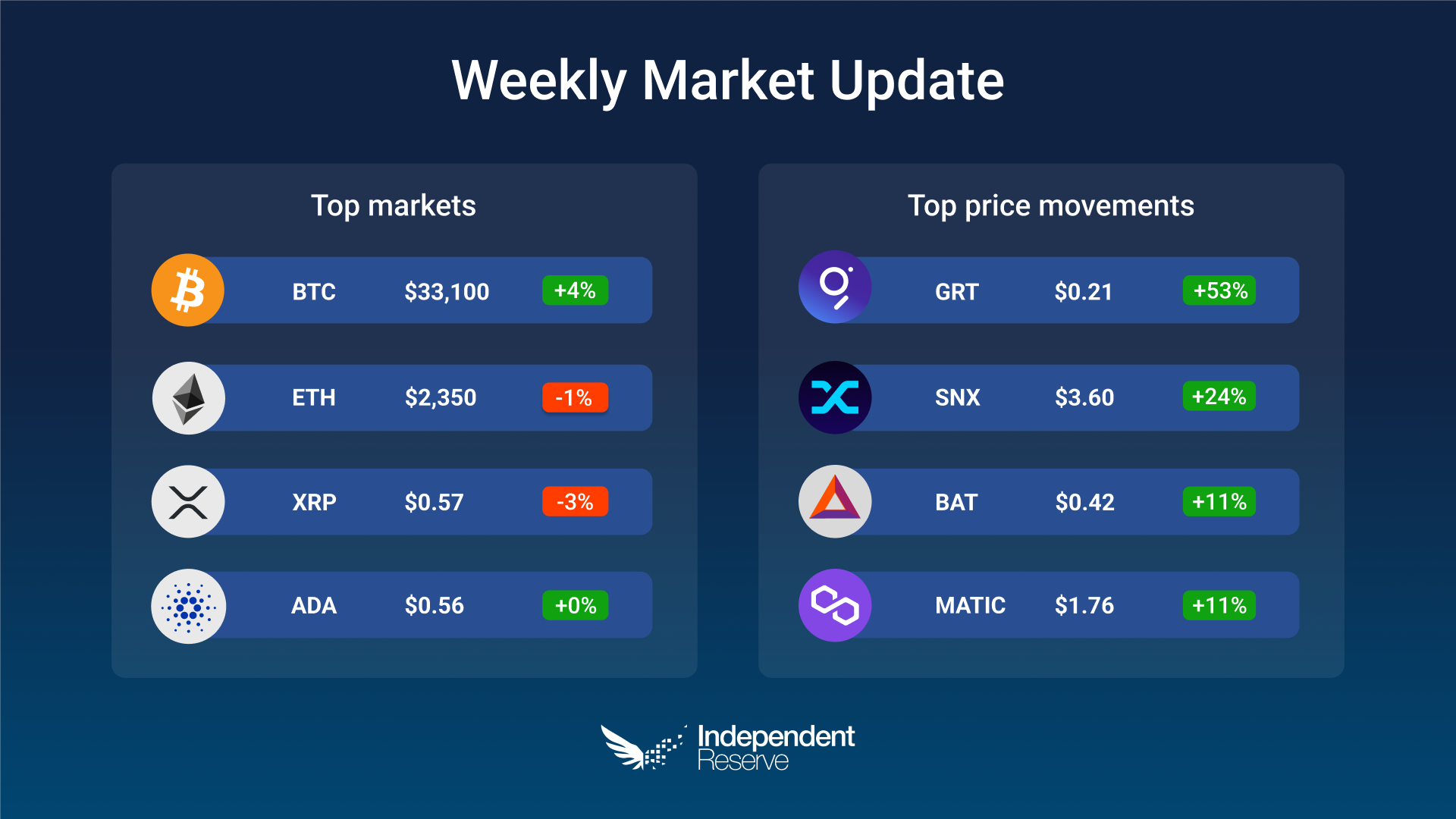

Signs suggesting that inflation is coming down and interest rate hikes will pause are gathering, with the February US Personal Consumption Expenditures (PCE) index modestly beating expectations in some areas. The White House claimed inflation: “Was down by nearly 30 percent from this summer, against a backdrop of low unemployment and steady growth.” Closer to home, inflation has fallen to 6.8%, which is the best reading in eight months. Analysts are now looking ahead to a potential “Fed pivot” when rates start to decrease. The average one-year return for the S&P 500 following a pivot since 1984 was 18.9% (although the data is more mixed further back.) Bitcoin finishes the week up 2.8% to trade around A$41,170 (US$27.9K), and Ethereum gained 5.7% to trade around A$2670 (US$1810). Ripple gained $5.3%, Cardano was up 13.2%, Dogecoin gained 30.2% thanks to Elon Musk (again), and Polygon was up 5.6%. The Crypto Fear and Greed Index is at 63, or Greed. Historically speaking, April is a good month for crypto prices, with monthly gains in six of the last 10 years averaging 17%, according to Matrixport.

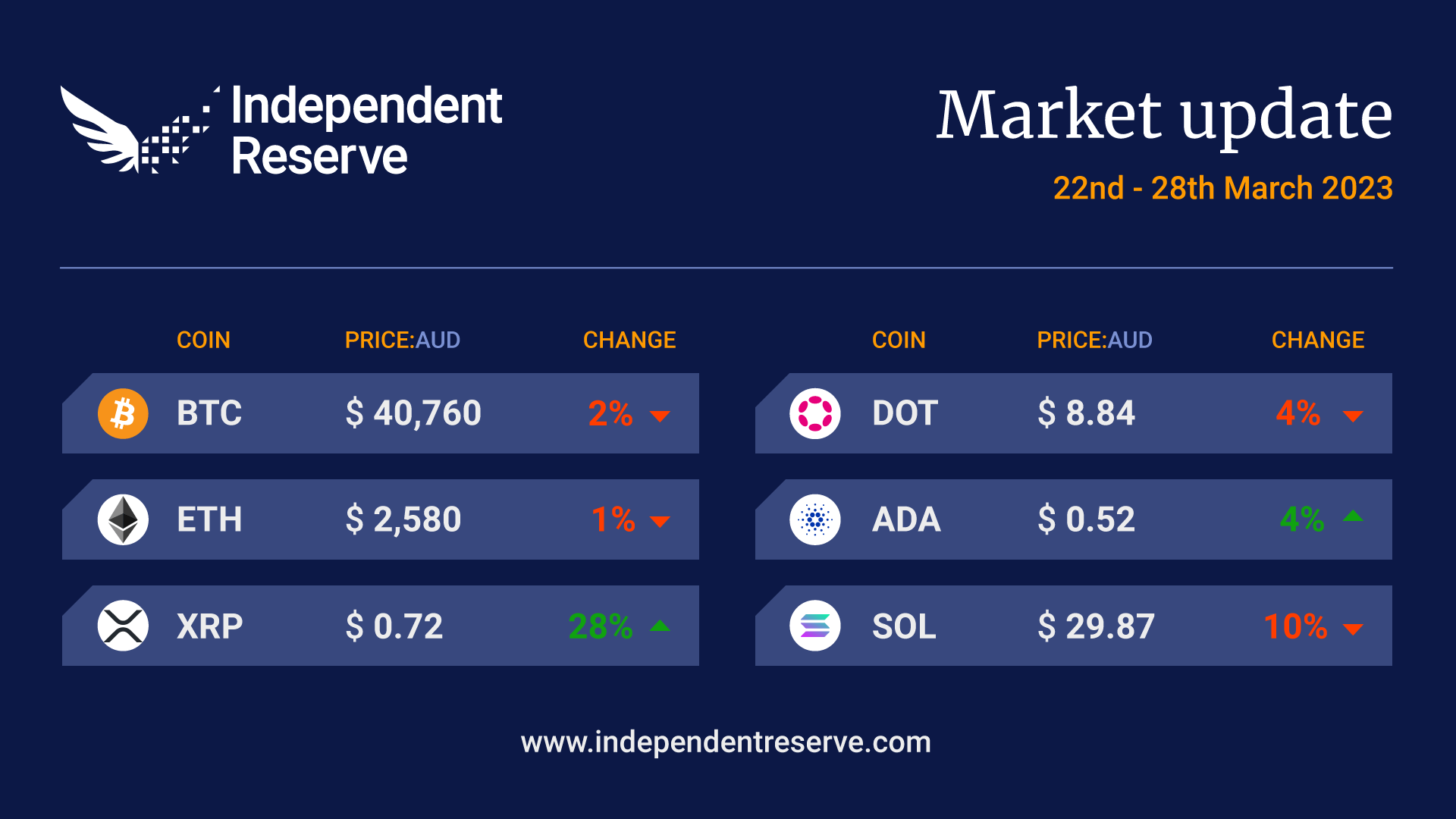

Bitcoin sank below US$27K (A$40.5K) today as news emerged the war on crypto has expanded to Binance, but it has since recovered slightly. It finishes the week down 3.3% to trade at A$40,790 (US$27.1K), while Ethereum is down 2.5% to A$2570 (US$1710). MicroStrategy is still a believer, though, buying another 6455 BTC for US$150 million (A$225M). It was a mixed picture on markets at the time of writing, with Ripple up 26.3% for the week, Cardano up 2.5% and Dogecoin (1.2%). Polygon fell 6.7%, Solana lost 11.8%, and Polkadot was down 4.8%. US interest rates have risen to 5%, with markets evenly divided between those expecting a 25bps increase at the next meeting and those expecting a pause. Bitcoin’s hashrate briefly spiked to almost 400 exahash and is currently at 335 EH/s. The Crypto Fear and Greed Index is at 64 or Greed.

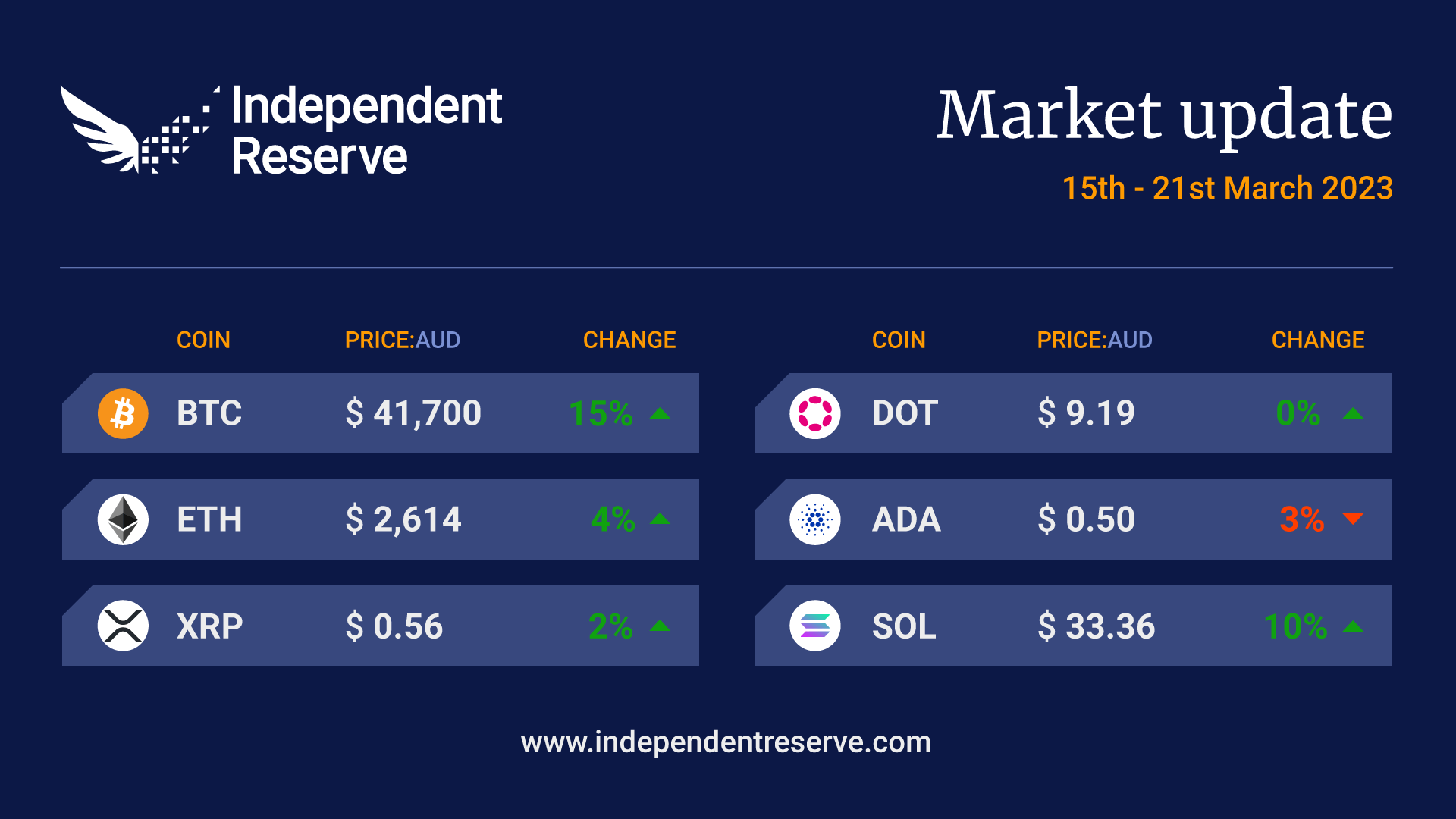

A long-held fantasy of Bitcoiners appears to be coming true (at least in a small way), with Bitcoin surging in the midst of fears over the collapse of the banking sector. Bitcoin is up 40% since the crisis began and reclaimed the US$28K (A$41.7K) mark this week for the first time since June 2022. The Crypto Fear and Greed Index has topped 66 (Greed), the highest level since November 2021 (Bitcoin’s ATH). The crisis has lessened the chances of further steep interest rate rises in the US, with the market tipping a 25-basis point rise this week. What some characterise as backdoor money printing from the Fed’s Bank Term Funding Program (BTFP) may also be having an impact. The overall crypto market cap is A$1.74T (US$1.17 trillion). Bitcoin surged 16.3% this week and is currently trading at A$41,760 (US$27,980), while Ethereum was up 4.3% to US$2,620 (US$1,755). Bitcoin is leaving the other coins in the dust, with Ripple flat, Cardano down 3.5%, Polygon (-6.3%) and Dogecoin (-1.9%). Solana increased by 10%.

You might have assumed three crypto-linked banks collapsing and the government taking aim at crypto mining would put downward pressure on markets, but you’d be wrong. So is it really ‘long Bitcoin, short the bankers’ as economist Alex Kruger tweeted today, alongside a graph of bank stock prices plunging by double digits and Bitcoin surging? As usual, nobody is 100% sure, and there are a lot of moving parts: traditional markets now expect interest rate hikes to be lower to avoid putting more pressure on the banking system. USDC’s wobbles this week have woken Bitcoiners up to the fact it might not be a safe place to park money and some investors have been converting to BTC.

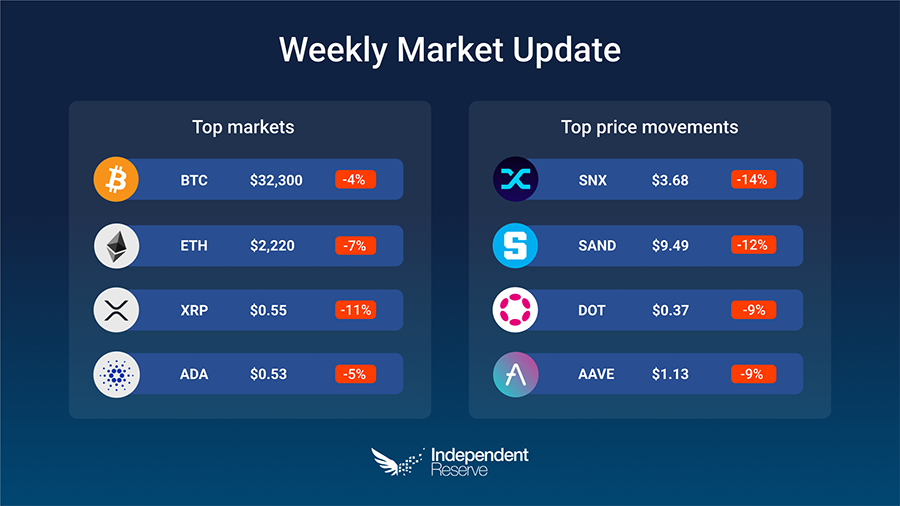

Investors seemed a little ambivalent this week, with Glassnode data showing that US$3.9 billion (A$5.78B) of Bitcoin flowed into exchanges over the past week… while US$3.8 billion (A$5.64B) flowed out. The macro picture was complicated by the release of a US Department of Commerce report indicating that the personal consumption expenditure price index rose 0.6% in January. Bitcoin finishes the week down 5.4% to trade around A$34,690 (US$23,385), while Ethereum was down 4.2% on the same time last week at A$2,410 (US$1,624). Ripple fell 4.9%, Cardano was down 10.2%, Dogecoin lost 7.9%, and Solana fell 13.5%, after the network was halted for the tenth time. The Crypto Fear and Greed Index is at 50 or Neutral.

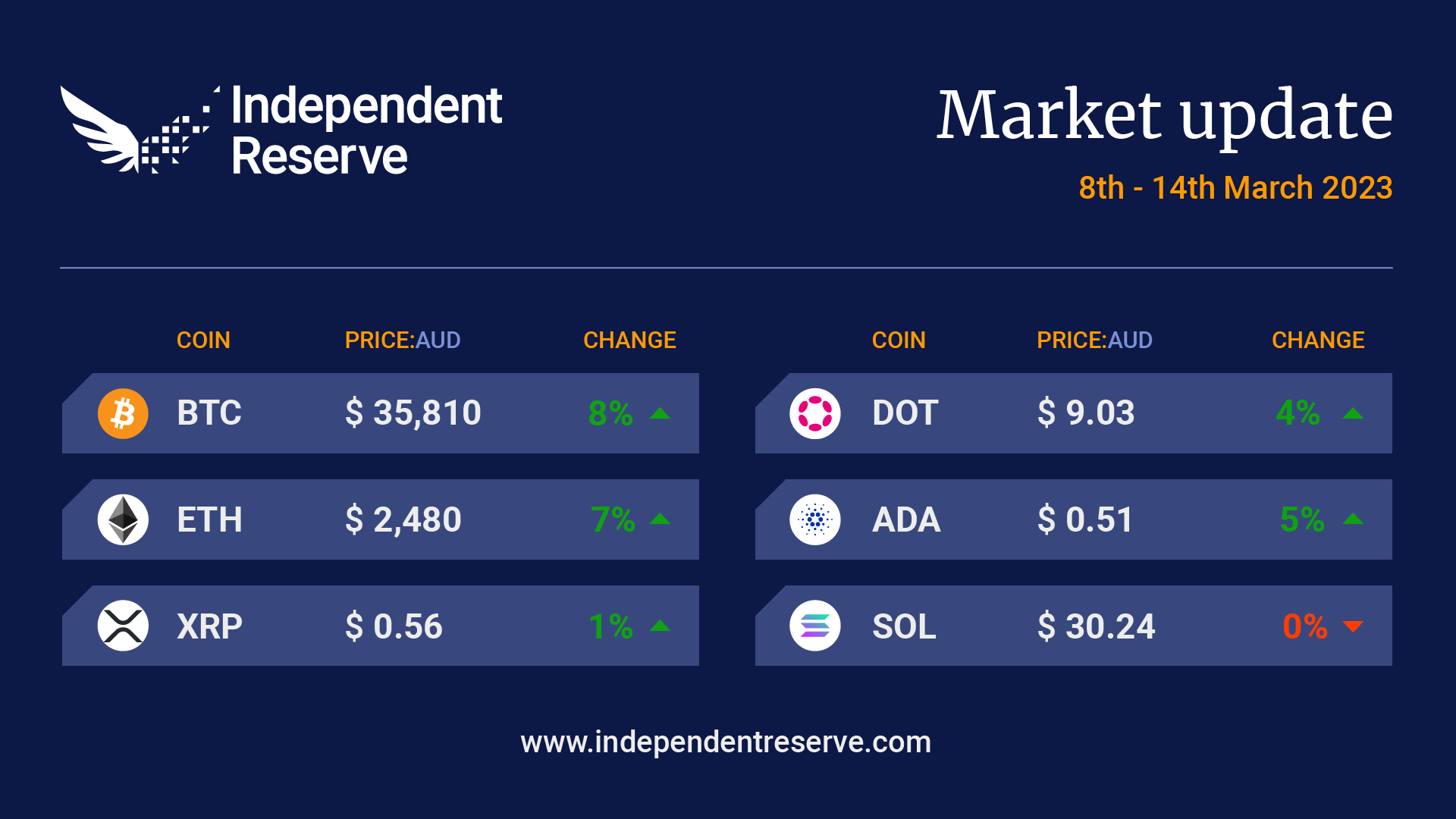

Amid the great crypto crackdown in the US, Bitcoin spiked above US$25K (A$36.2K) this week. Various theories have been advanced about why the price is up when the news is bad: They include the return of the ‘China narrative’ as Hong Kong warms up to crypto, improving macro conditions, an influx of money from big funds , and a hypothesis that users who are unable to redeem Binance-issued BUSD for dollars (after it was declared a security by the SEC) have been dumping it into Bitcoin and Ether. At the time of writing, Bitcoin had recorded a 14.4% gain on a week ago to trade at A$35,810 (US$24.8K), while Ether was up 13.8% to A$2,455 (US$1,700). Everything else was up, including Ripple (6.9%), Cardano (12.5%), Polygon (24.6%) and Dogecoin (7.1%). The Crypto Fear and Greed Index is at 58 or Greed.

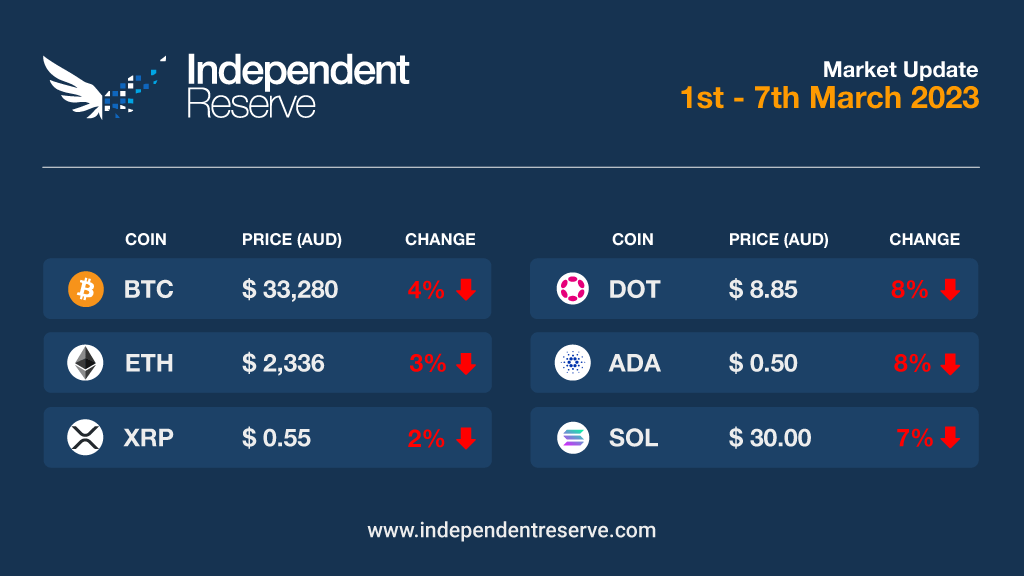

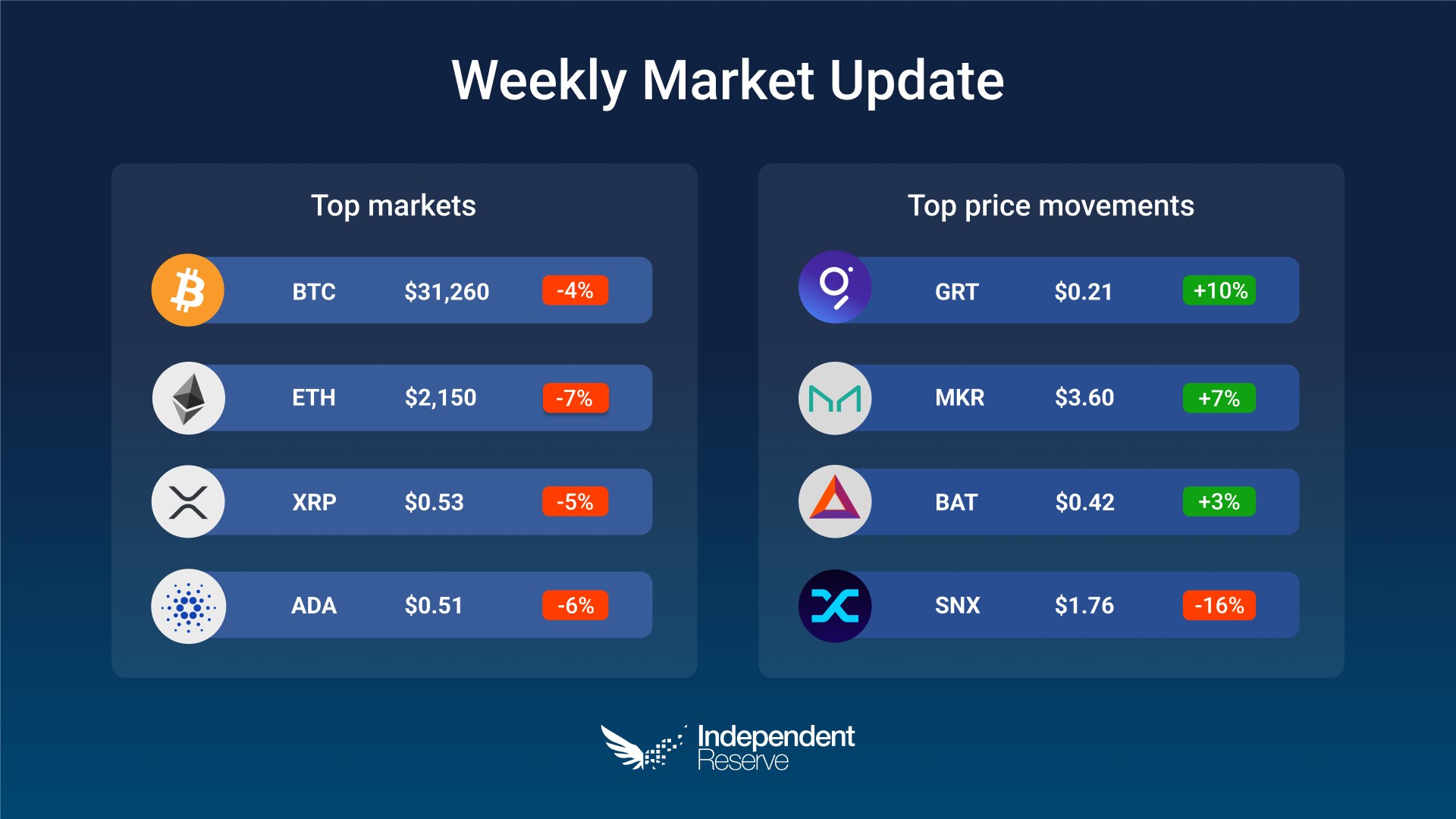

Regulatory action in the US took centre stage this week, with Bitcoin falling 4.1% to A$31,260 (US$21,755). Ethereum dropped 7.1% to A$2,150 (US$1,500). Despite the crackdown the big market mover is likely to be the imminent release of inflation figures in the US, with anything indicating an increase likely to weigh heavily on prices. XRP lost 5.1%, Cardano was down 6.1% and Dogecoin lost 8.1%. The Crypto Fear And Greed Index is at 48 or Neutral.

Crypto markets saw a boost earlier in the week after the US Federal Reserve raised rates by the expected quarter of a percent and officials started to talk about “disinflation”. Bitcoin poked its head above US$24K (A$34.6K) while ether traded above US$1,700 (A$2,450) for the first time since September. However, the good vibes came to a halt after unexpectedly strong job numbers on Friday raised fears that rates will continue to rise. Nonfarm payroll jobs jumped 517,000 in January, much higher than the 185,000 predicted and US unemployment is now at its lowest level since 1969. Closer to home the Reserve Bank is expected to raise interest rates again today. Bitcoin finishes the week down 4.1% to trade at A$32,760 (US$22,755) while ether was down 1% to A$2,333 (US$1,620). XRP lost 3.5%, Cardano was relatively flat, Doge gained 2.6% and Polygon was also up, by 2.2%. The Crypto Fear and Greed Index is at 56 and has been at ‘greed’ for the past week.

With the first four weeks of the year green, you’d be forgiven for thinking that Crypto Spring had sprung, but the Bitcoin price rise came to a shuddering halt today with a dip below US$23K (A$32.6K), perhaps on fears the Federal Reserve might throw a curveball with its interest rate decision this week. However most pundits seem to expect a soft quarter point hike. Earlier this week around 64% of Bitcoin holders were in profit, but that’s fallen below 50% today according to IntoTheBlock. Crypto stocks including Silvergate, Coinbase, MicroStrategy and Block all surged by double digit percentages earlier this week. Bitcoin finishes the week down 4% to trade at A$32,300 (US$22,775) while Ethereum lost 7% to trade at A$2,220 (US$1,565). XRP was down 11%, ADA lost 5%, MATIC increased 5%, and SOL was down 5%. At the time of writing the Fear and Greed Index was at 51 or Neutral.

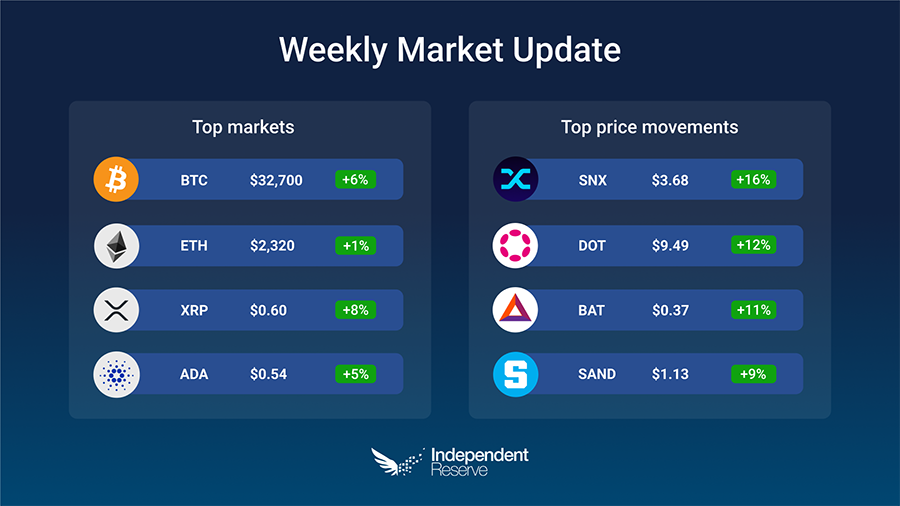

Back in early 2018 all of crypto was pinning its hopes on a post Lunar New Year recovery that never came. Well, in 2023 the markets keep going up and much of Crypto Twitter seems united in disbelief. Is this just a bull trap? Bitcoin is now up 38% in the year to date and hit US$23,230/A$33K on the weekend for the first time since August 2020. The total crypto market cap is once again above US$1 trillion – it’s currently A$1.5T – and Gold and the S&P 500 are also recovering, up 19% and 13% respectively. Bitcoin finished the week up 6% to trade around A$32,700 (US$22,980) while Ethereum gained 1% to trade at A$2,320 (US$1,630). Almost everything else was up including XRP (8%), ADA (5%), DOGE (4%), SOL (4%), but MATIC lost 4%. The Crypto Fear and Greed Index remains at 52 or ‘neutral’.

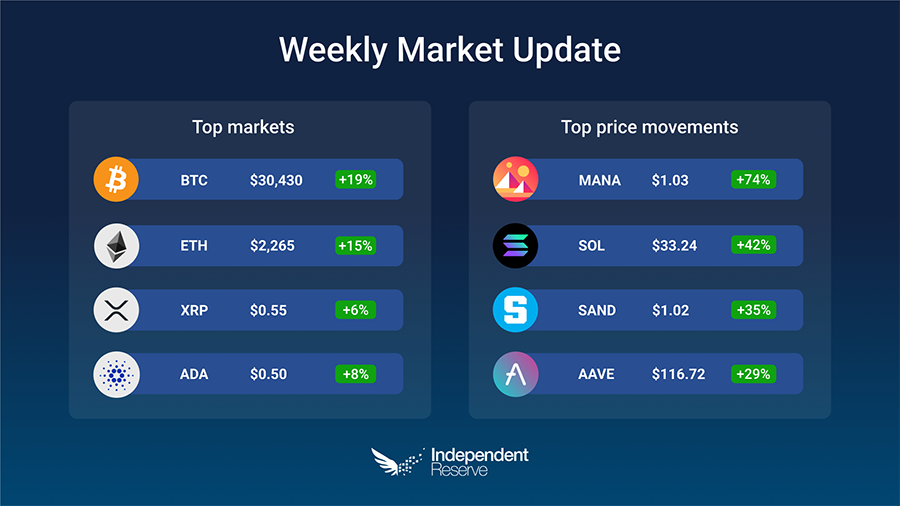

Is Crypto Winter over? Bitcoin suddenly broke through US$20K (A$28.7K) on Saturday and then US$21K (A$30.2K) on Sunday. Bears were rekt with US$500 million (A$718M) in liquidations. Bitcoin is again trading above the 2017 top and has recovered its losses from the FTX collapse. Pundits point to inflation moderating by 0.1% in December, FTX finding US$5B (A$7.18B) in assets, whales growing more confident and the Bitcoin halving in May 2024 as possible reasons for the rally. Bitcoin is currently trading at A$30,430 (US$21.2K), up 19% for the week, while Ethereum is at A$2,265 (US$1,577), up 15% on seven days ago. Everything else increased: XRP (7%), MATIC (17%) and SOL (39%). The overall crypto market cap is at $1.425 trillion (US$992B). After 10 months the Crypto Fear and Greed Index hit 52 or ‘neutral’ two days ago; it currently sits around the same at 51 at the time of writing.