Market update

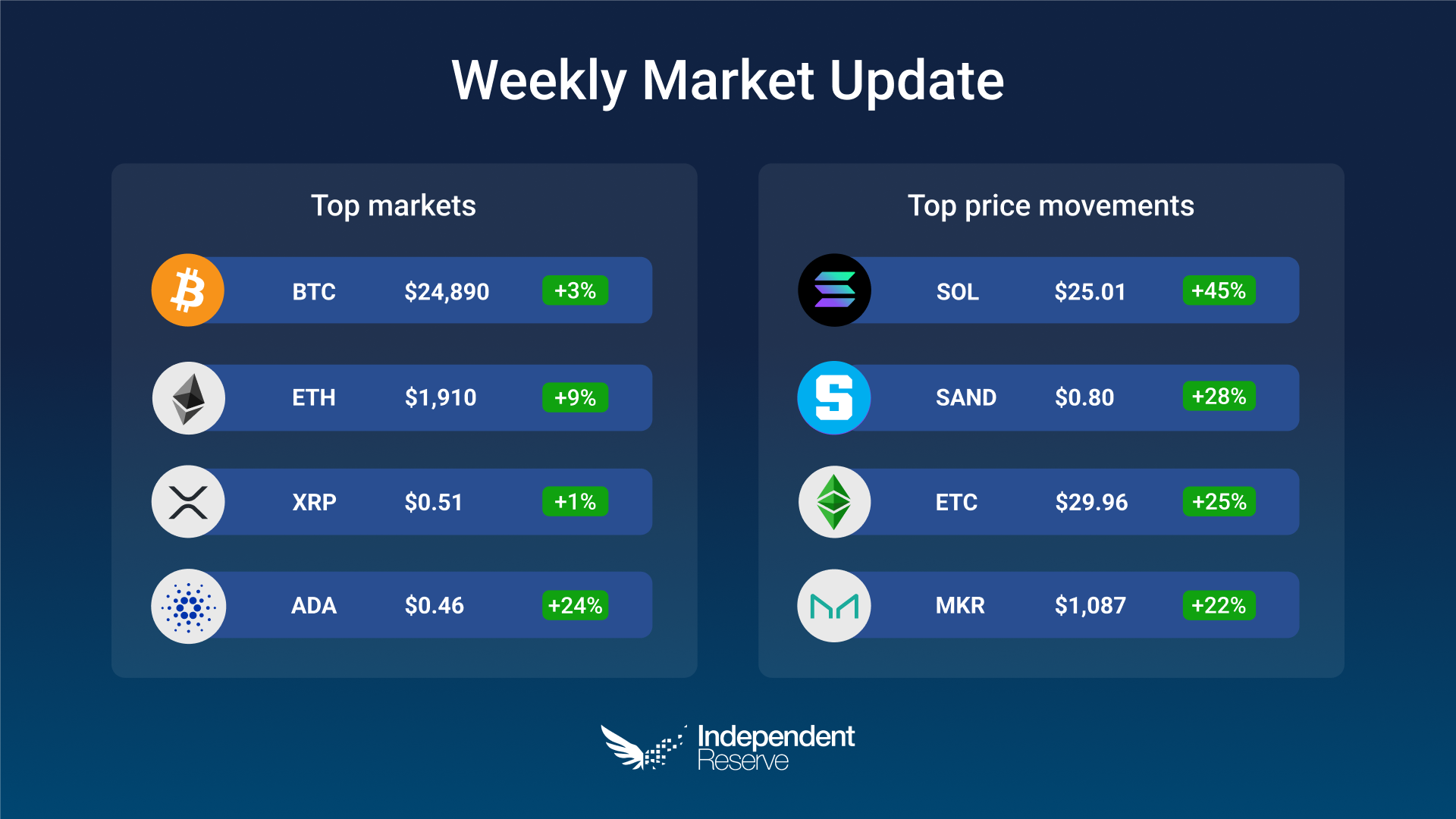

Crypto markets appeared to have finally turned a corner this week after grinding along with low volatility since the collapse of FTX in November. It’s too early however to call the bottom or work out if this is just a bull trap. Pundits linked the rise to markets expecting a lower US inflation figure this week and for interest rates to peak around 5%, but in truth it’s just as likely to be the fact that no major exchange or crypto firm has collapsed in the past couple of weeks. Bitcoin has broken through the US$17K (A$24.6K) mark and is up 3% from a week ago to trade at A$17,220 (US$24,885). Ethereum gained 8.6% to trade at A$1,910 (US$1,322). Everything else was up, including Cardano (24%), Dogecoin (6%) and Polygon (7.8%). Solana gained 46% and has more than doubled in price since its lows two weeks ago. Crypto mining companies and other blockchain-linked stocks, including Riot Blockchain, Marathon Digital, Coinbase and Silvergate have all rallied by double-digit percentages on share markets.

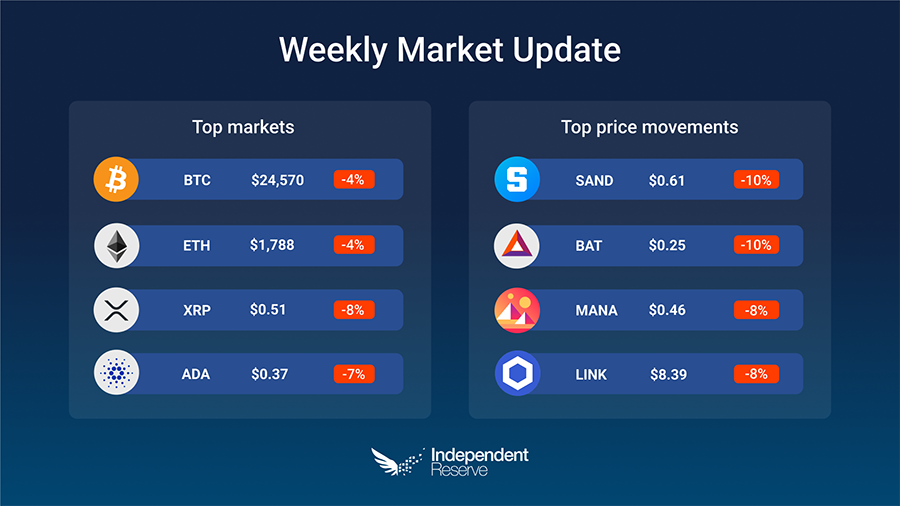

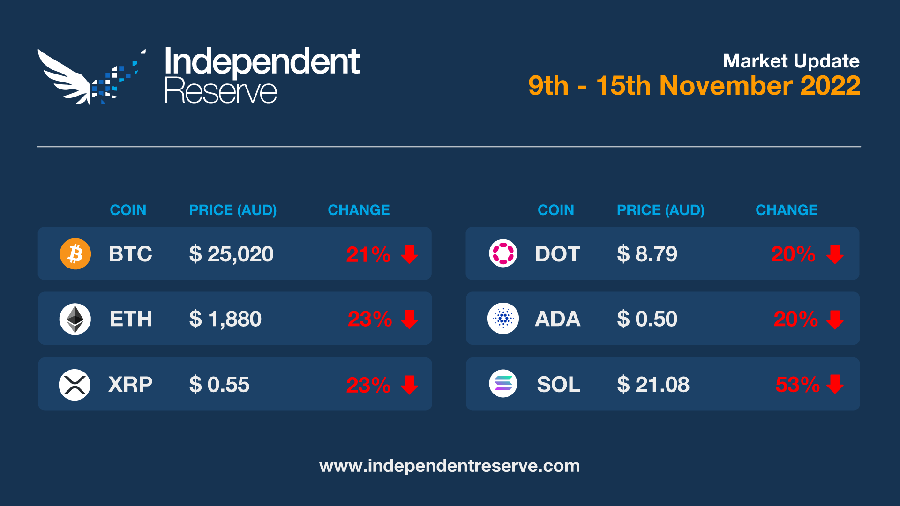

Crypto markets rose mid-week in expectation of a more positive outlook from the Federal Reserve, and Bitcoin peaked above US$18,000 (A$26.4K) for the first time since FTX collapsed. Then everything crashed after the Fed hiked rates by 50 basis points and said it will continue to raise rates into 2023. The good news is that US inflation came in at 7.1%, better than expected, and the slowest pace in nearly a year. Bitcoin finishes the week 5.5% down at A$25,045 (US$16,750) while Ethereum lost 6% to trade around A$1,780 (US$1,160). Everything else was down including XRP (-14%), Cardano (-19%) and Dogecoin (-20%). The Crypto Fear and Greed Index is at 29 or Fear.

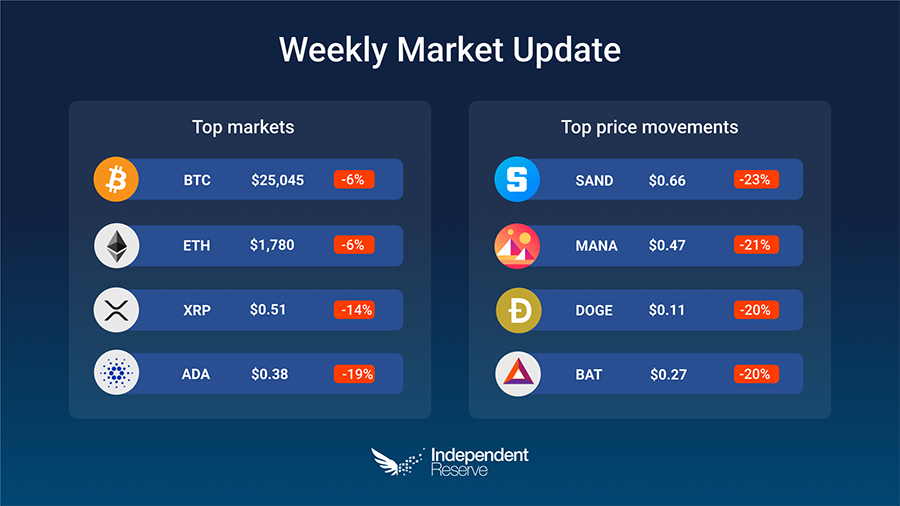

With all the paper hands and retail tourists gone long ago, crypto markets aren’t making any dramatic moves despite fresh bad news coming out daily. Bitcoin was down 2% on seven days ago to trade at A$25,485 (US$17,190) and Ethereum also lost 2% to trade at A$1,888 (US$1,273). XRP lost 4% (there are unconfirmed rumours of a settlement in the SEC case), Dogecoin fell 13% while Cardano lost 7%. November’s US inflation data comes out in the next 24 hours and markets expect the next rate rise will be 50 basis points.

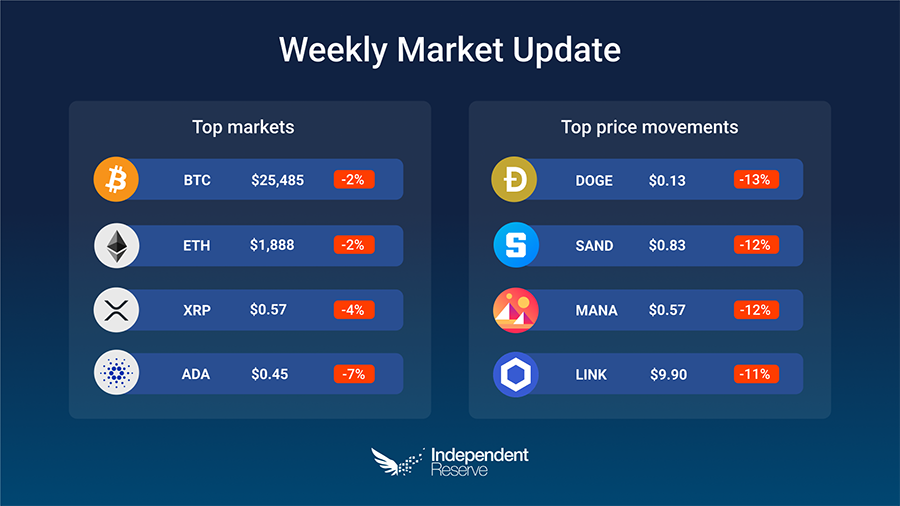

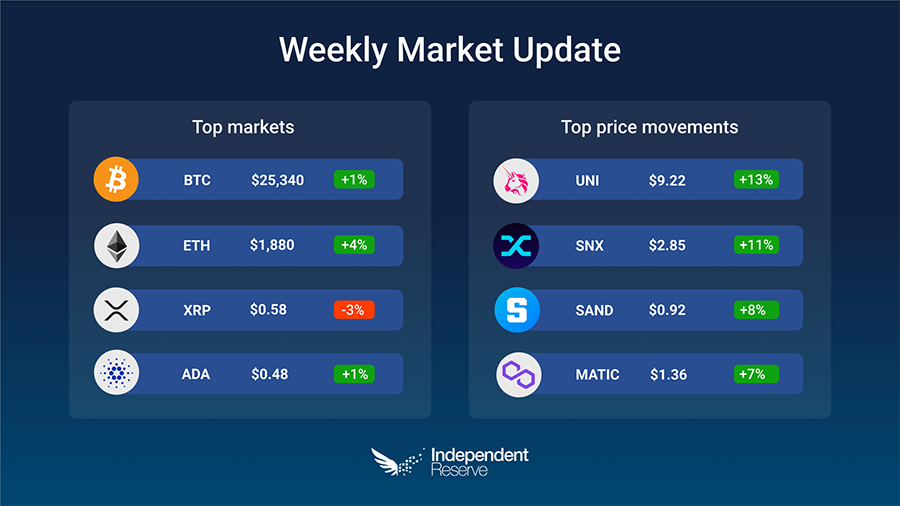

There were some green shoots this week with monthly inflation data showing a slight easing to 6.9% and pundits tipping the next interest rate rise will be 0.25%. There’s also the slim chance of a Santa Claus Rally (even if there’s not a lot of evidence of any consistent December rise over the years). Bitcoin finished the week up 1% to trade at A$25,340 (US$16,940) while Ethereum increased 4% to A$1,880 (US$1,260). XRP is down 3%, Dogecoin increased 4% (related: rumours of a Twitter Coin) and Cardano was up 1%. The Crypto Fear and Greed Index is at 25 or Extreme Fear.

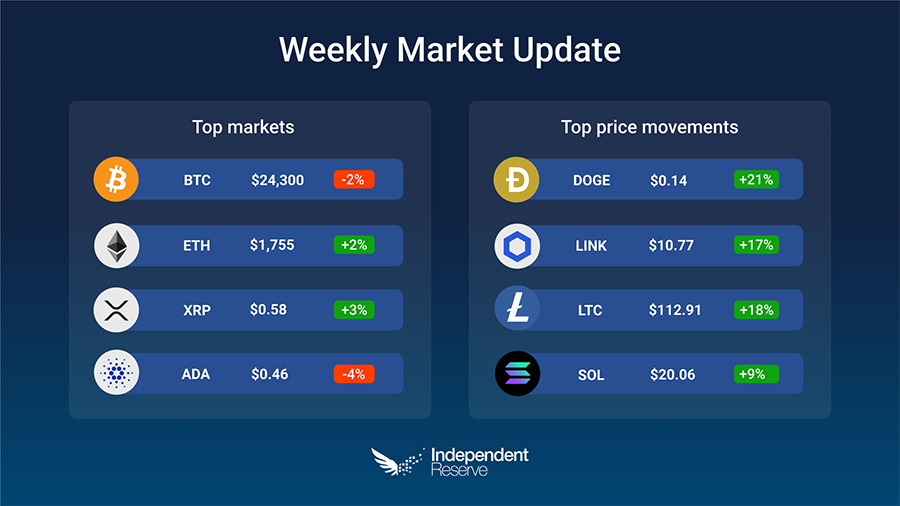

Despite acres of bad news, markets have been mostly in a holding pattern this week. Bitcoin finishes the week down 2% to trade at A$24,300 (US$16.1K), while Ethereum increased 2% to A$1,755 (US$1,167). XRP gained 3% and Dogecoin surged 21% after Twitter boss Elon Musk mentioned payments in a tweet about his new ‘everything app’. Decentrader’s Filbfilb said this week “[the] fact that we haven’t dumped harder than we actually really could have done is a good sign for the bulls,” but he also said Bitcoin could fall below A$15K (US$10K). The Crypto Fear and Greed Index increased to 26 or simply ‘Fear’.

Bitcoin has fallen to two-year lows amid the FTX fallout, with just over 51% of addresses at a loss, which compares to 55% at the bottom of the previous crypto winter in January 2019, and 62% in 2015.

However, the price crash from the collapse of the world’s second largest exchange hasn’t been as severe as may have been expected, with Bitcoin down another 8% for the week to trade around A$23,990 (US$15.8K) and Ethereum down 13% to hit A$1,670 (US$1.1K). Everything else was down including XRP (-8%), Cardano (-11%), Dogecoin (-15%) and Solana (-18%). Some true believers are still buying, with Pantera Capital reportedly snapping up A$212M (US$140M) in BTC to once again demonstrate its belief in halving cycles (which will theoretically see a turnaround early in 2023). El Salvador President Nayib Bukele plans to dollar cost average in from now on, buying one Bitcoin a day. The Crypto Fear and Greed Index is at 22 or Extreme Fear.

Normally, crypto markets would likely be heading upwards following the news that US inflation had come in below expectations by falling to 7.7%. The Nasdaq and S&P 500 certainly had their best week in six months! However, the FTX/Alameda collapse saw the overall crypto market plunge from A$1.52 trillion (US$1.02T) to A$1.235T (US$827 billion) in the space of a week. Bitcoin fell from A$32K (US$20.8K) to hit the lowest point for the year below A$24.4K/US$16K with more pain expected. Bitcoin’s relative strength index (RSI) reached an all-time monthly low of 40.5 on November 10. Bitcoin finishes the week 21% down to A$25K (US$16.7K) while Ethereum lost 23% to trade at A$1,880 (US$1,260). Everything else crashed too including XRP (-23%), Cardano (-20%), Dogecoin (-25%) and Solana plunged 53%. The Crypto Fear and Greed Index is at 24 or Extreme Fear. In some good news though, the extremely low prices mean that the number of people who own one whole Bitcoin is fast approaching 1 million.

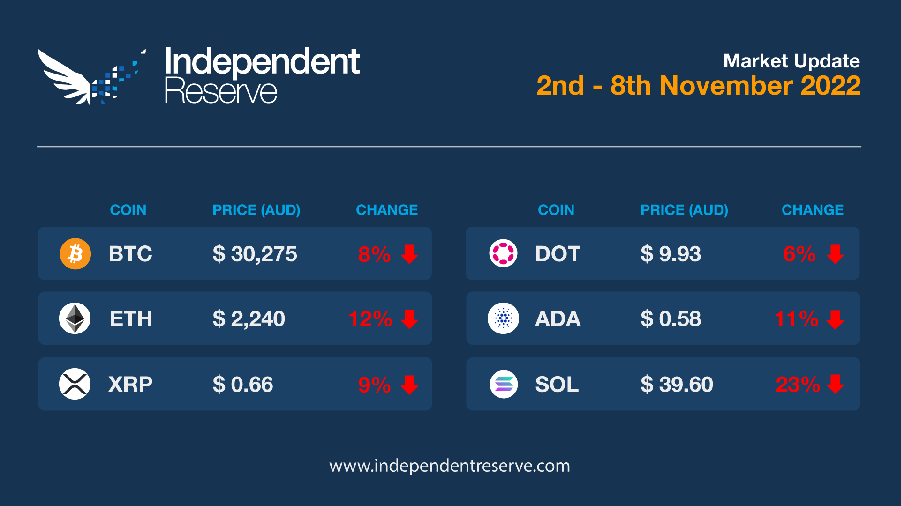

This week saw no major moves on the crypto market…untill today.. The overall market cap has dropped under US$1 trillion to around US$965M (A$1.5T). There are signs of continued hiring in the US jobs market, despite a slight rise in unemployment to 3.7%, but all eyes will be on the inflation data coming out later this week. Bitcoin finishes the week down 8% to trade around A$30,275 (US$19,540) and Ethereum which was down 12% to finish at A$2,240 (US$1,440). XRP was down 9%, Dogecoin (-32%) and Cardano finished at -11% for the week. Solana also dropped 23% for the week despite good news about partnerships with Google. The Crypto Fear and Greed Index is at 31, or Fear.

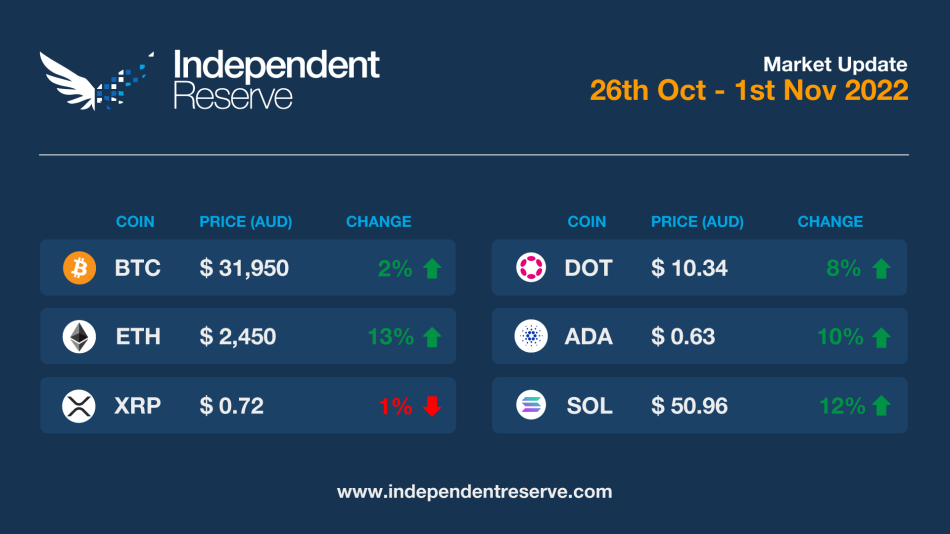

So October turned out to be ‘Uptober’ after all, with Bitcoin increasing 6.2% over the course of the month and Ethereum rising 20%. At the time of writing the overall cryptocurrency market cap was back over the US$1 trillion mark at around A$1.579T (US$1.013T). Bitcoin is up 2% on the same time last week to trade around A$31,950 (US$20,475). Ethereum gained 13% for the week to trade around A$2,470 (US$1,580). XRP was flat but Dogecoin overtook Cardano with a whopping 120% rise, thanks to honorary Dogecoin CEO Elon Musk buying Twitter. Cardano itself rose 10% while Solana gained 12%. The Crypto Fear and Greed Index has finally climbed out of the Extreme Fear zone for the first time in six weeks to sit at 31 or simply Fear.

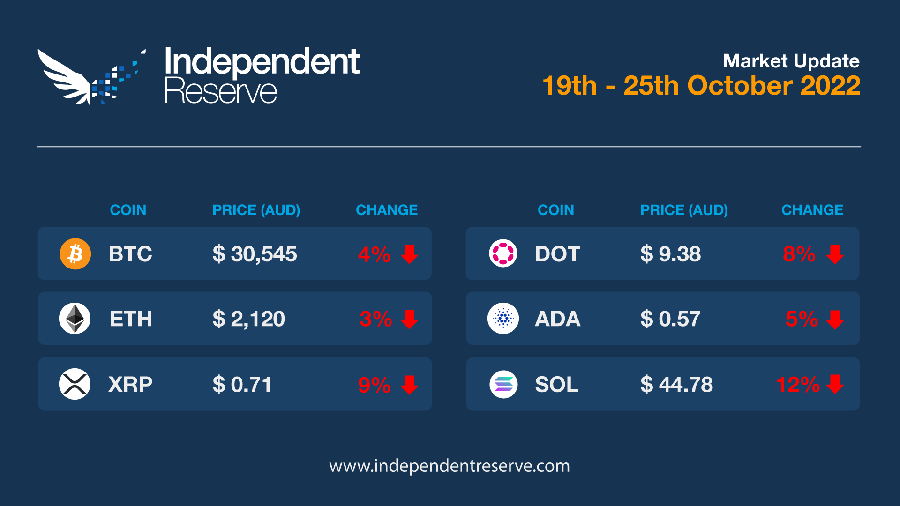

The stock markets have welcomed a report the US Federal Reserve is set to debate a less-aggressive interest rate hike in December. However, with economic turmoil in Britain and the looming spectre of recession, the overall picture remains bleak. Crypto markets are running fairly steadily with Bitcoin finishing the week at A$30,545 (US$19.3K) and Ethereum down slightly to trade around A$2,120 (US$1,340). XRP lost 9%, Cardano (-5%), Solana (-12%) while Dogecoin finished flat. The Crypto Fear and Greed Index is at 20, or Extreme Fear, which is where sentiment has been stuck since last month.

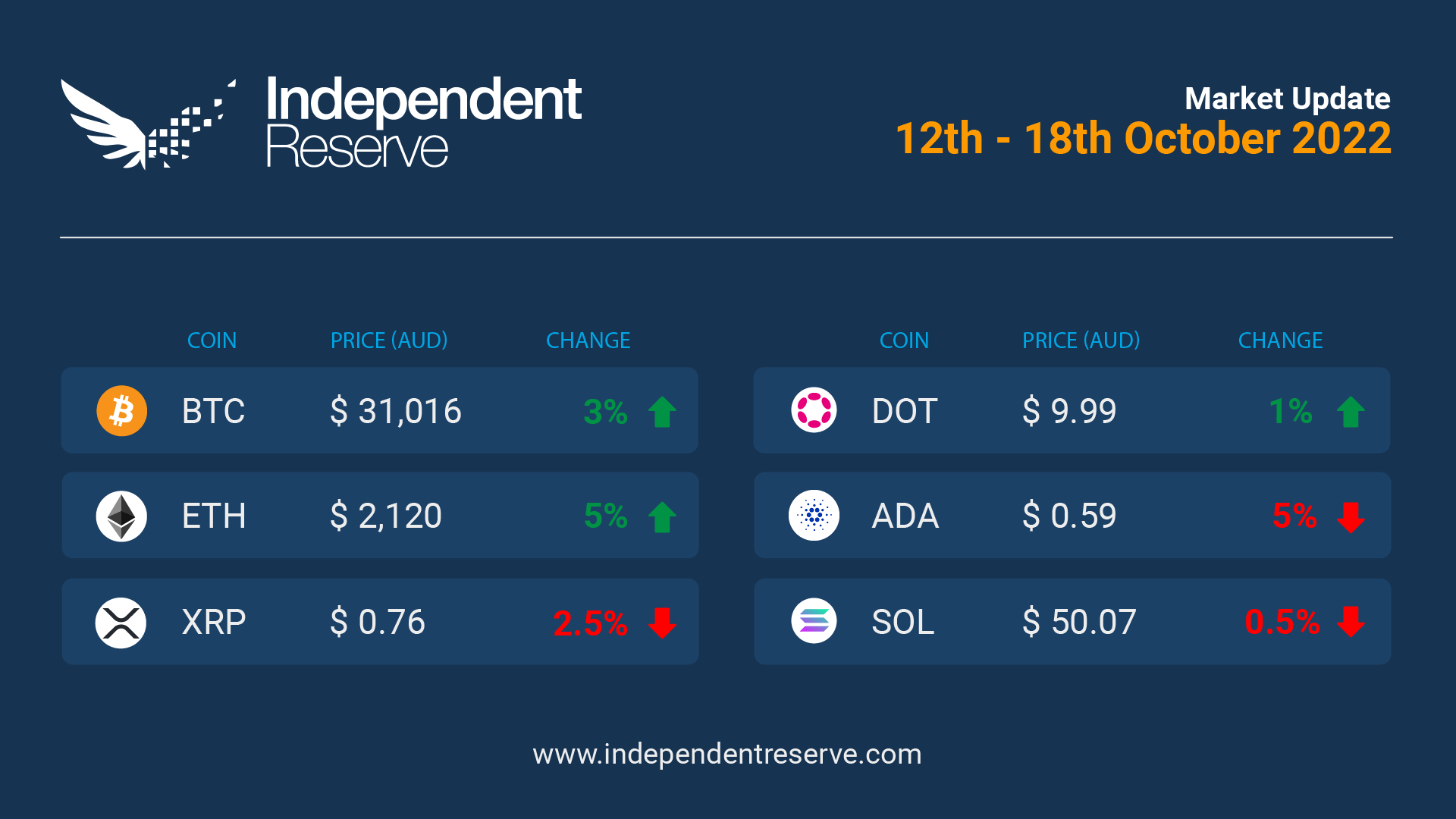

Inflation in the US rose at twice the pace forecast by economists and was up 0.4% in September and 8.2% for the year. The likelihood of a recession in the US and Europe has increased, although many pundits believe Australia may squeak through yet again. Some analysts draw comparisons with the high inflation, and the super long sideways market of 1940 to 1947 to suggest the next bull run is far away. Crypto markets appear to have found a certain amount of equilibrium at these prices, with Bitcoin up 3% for the week to trade just under A$31,000 (US$19.5K). Ethereum increased by 4.6% to A$2,110 (US$1,330). XRP lost 2.5%, Cardano dropped 5%, Solana was down 0.5%, and Dogecoin was flat. The Crypto Fear and Greed Index is at 20 or ‘Extreme Fear’.