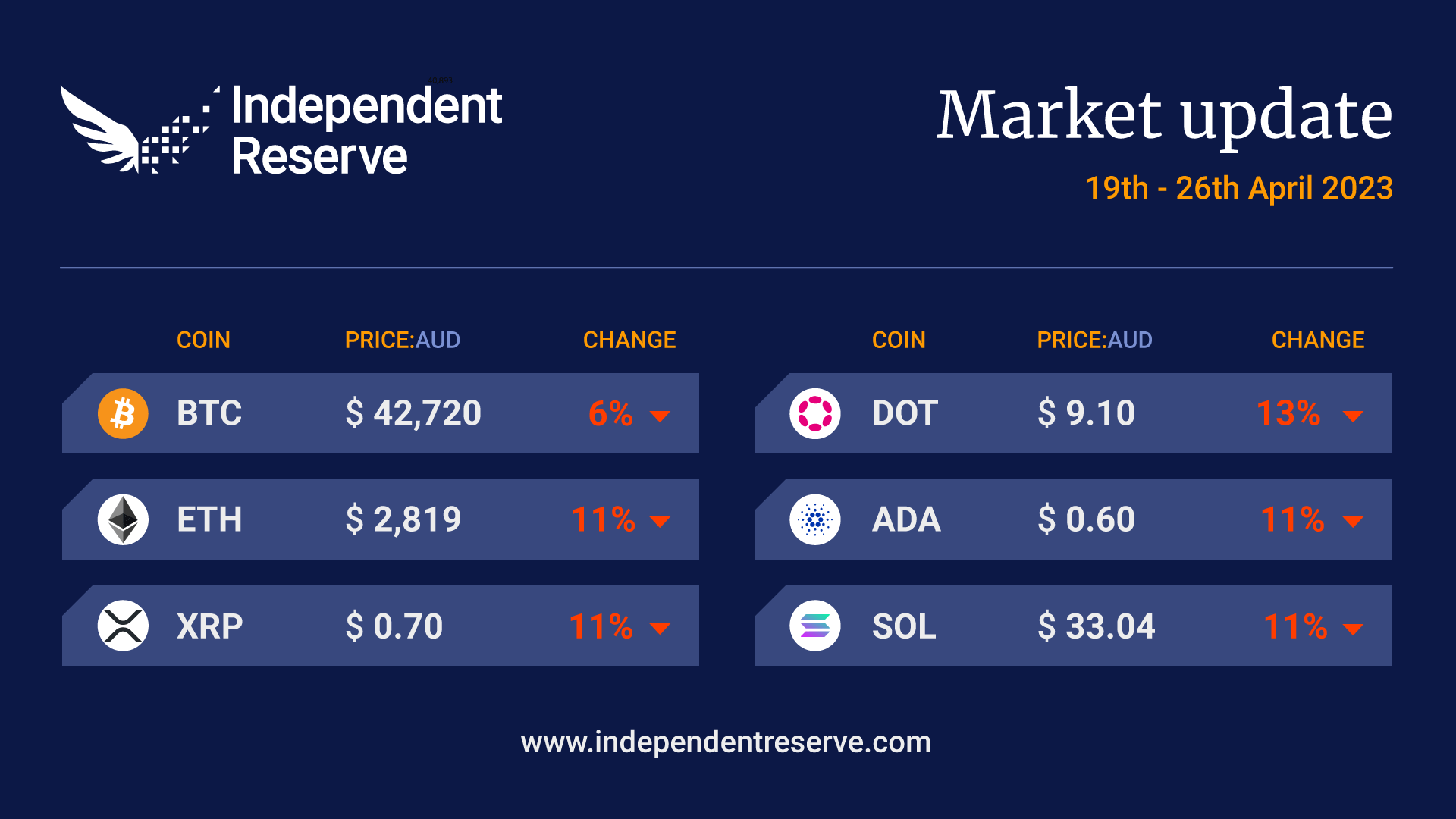

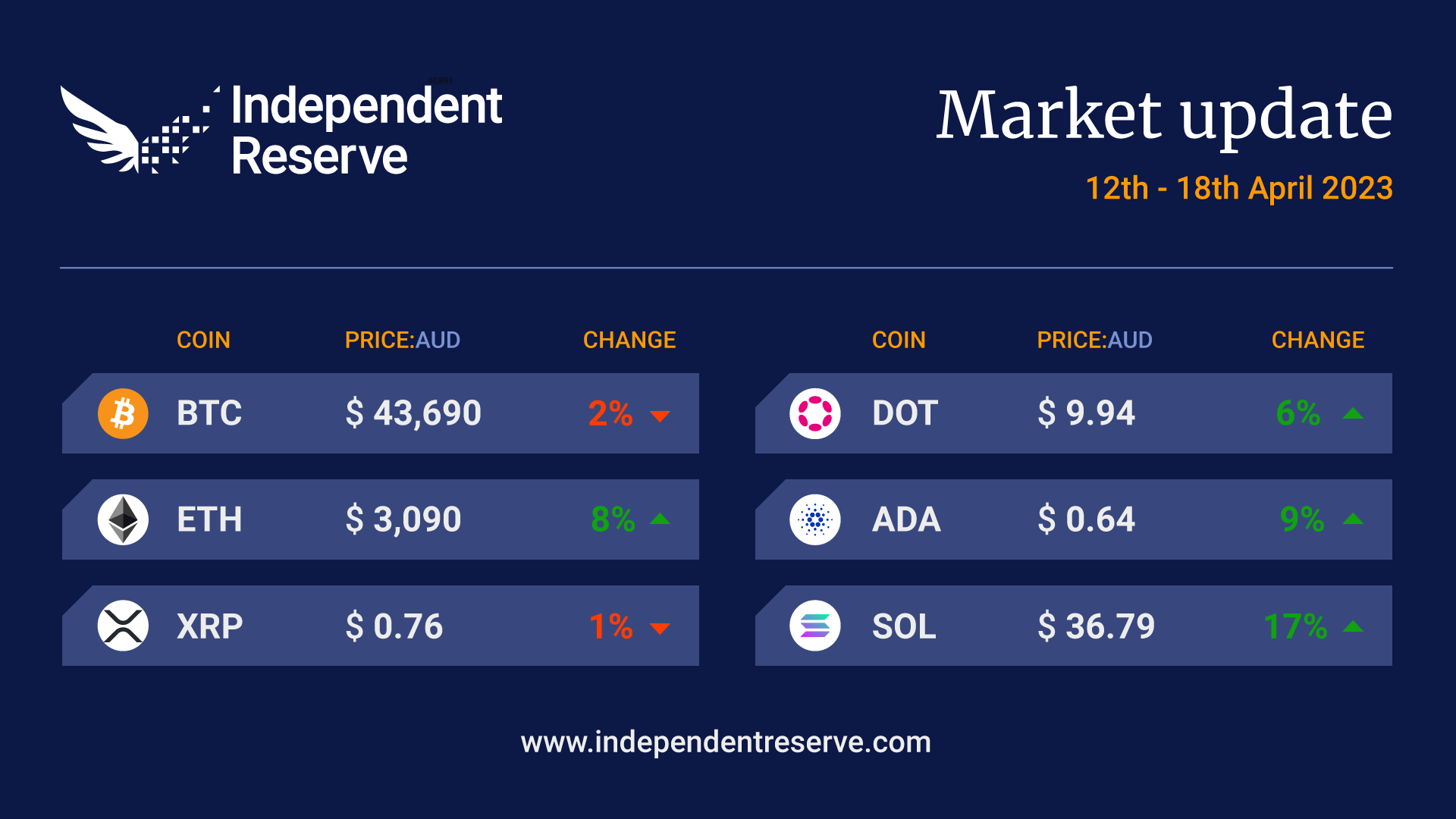

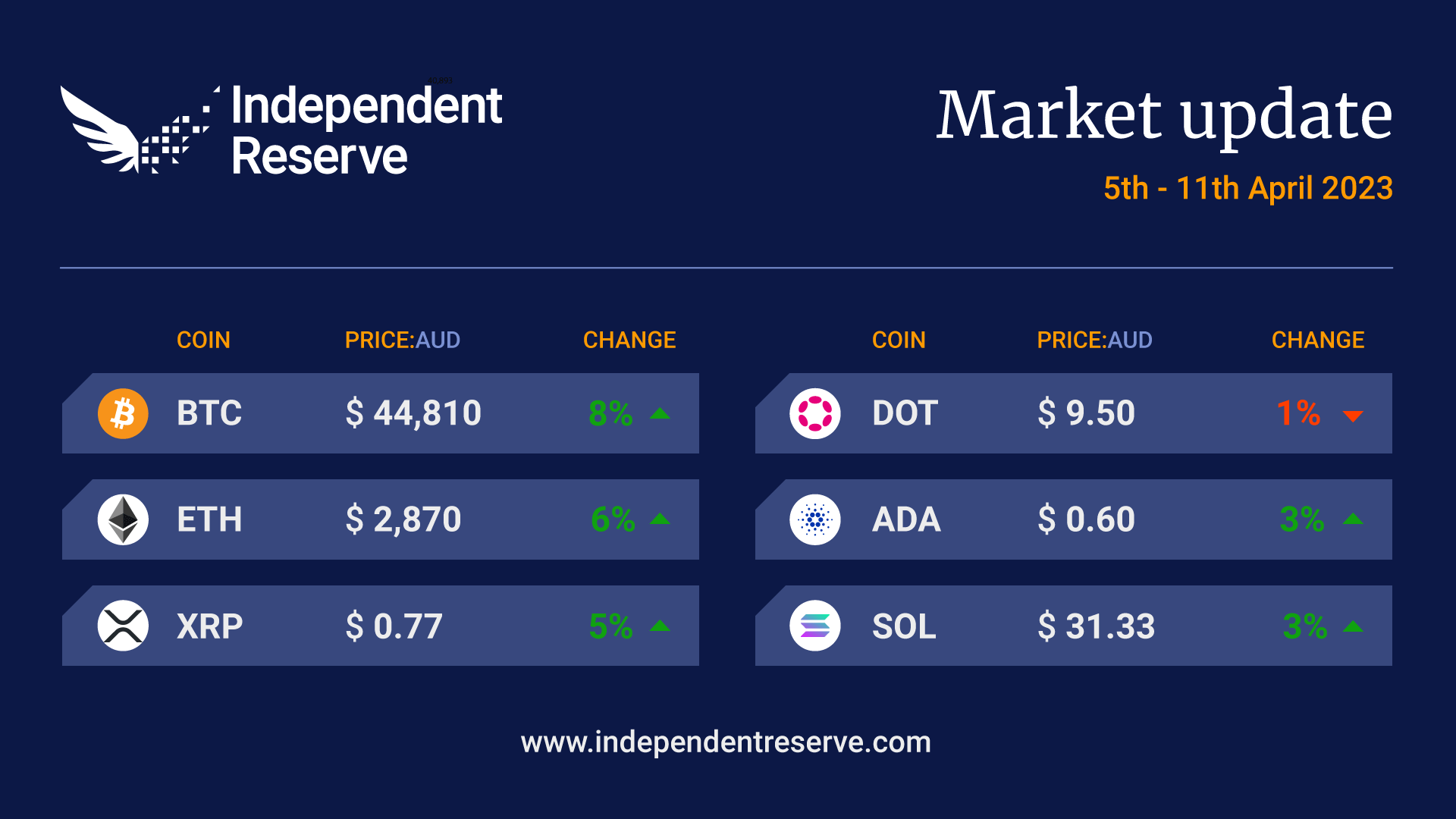

Market update

Bitcoin surged to its highest level in a year – around A$47K (US$31.4K) this week, marking an 85% rise for the year to date. Bitcoin finishes the week up 12.8% at A$45,155 (US$30.2K) while Ethereum gained 7.1% to trade at A$2,775 (US$1,859). Ripple fell 3.2% but most other coins enjoyed gains including Cardano (6.4%), Dogecoin (3.1%), Solana (1.5%) and Litecoin (12.3%). The biggest winner was Bitcoin Cash, which surged 108%, as investors reasoned the SEC will likely not declare it a security due to its similarity to Bitcoin. July is a historically strong month for prices notes Matrixport crypto researcher Makus Thielen, including 24%, 20% and 27% gains in the past three years. “Bitcoin could be at $33,000 to $36,000 by August (A$49.4K-A$54K),” he said. The Crypto Fear and Greed Index is at 55, or Greed.

After an uncertain couple of weeks, signs that the traditional finance industry still sees a future for crypto saw Bitcoin recover ground late last week. It finishes up 4% on seven days ago to A$39,400 (US$27,030). Ethereum gained 1% at A$2,546 (US$1,743). Altcoins that the SEC has alleged to be securities continued to slide, with XRP down 5% (after the Hinman emails failed to produce much in its favour), Cardano (+4%) and Polygon (1%). Solana was also up, increasing 7%, and Dogecoin was up 1.6%. The Crypto Fear and Greed Index is stuck at ‘meh’, also known as 47 or Neutral.

As Independent Reserve marks a significant milestone of 10 years in the cryptocurrency industry this week, our group CEO, Adrian Przelozny, reflects on the journey so far and shares insights into our values, achievements, and future aspirations. Thank you for being an integral part of our journey, and we look forward to the next 10 and beyond. Read Adrian’s full message here.

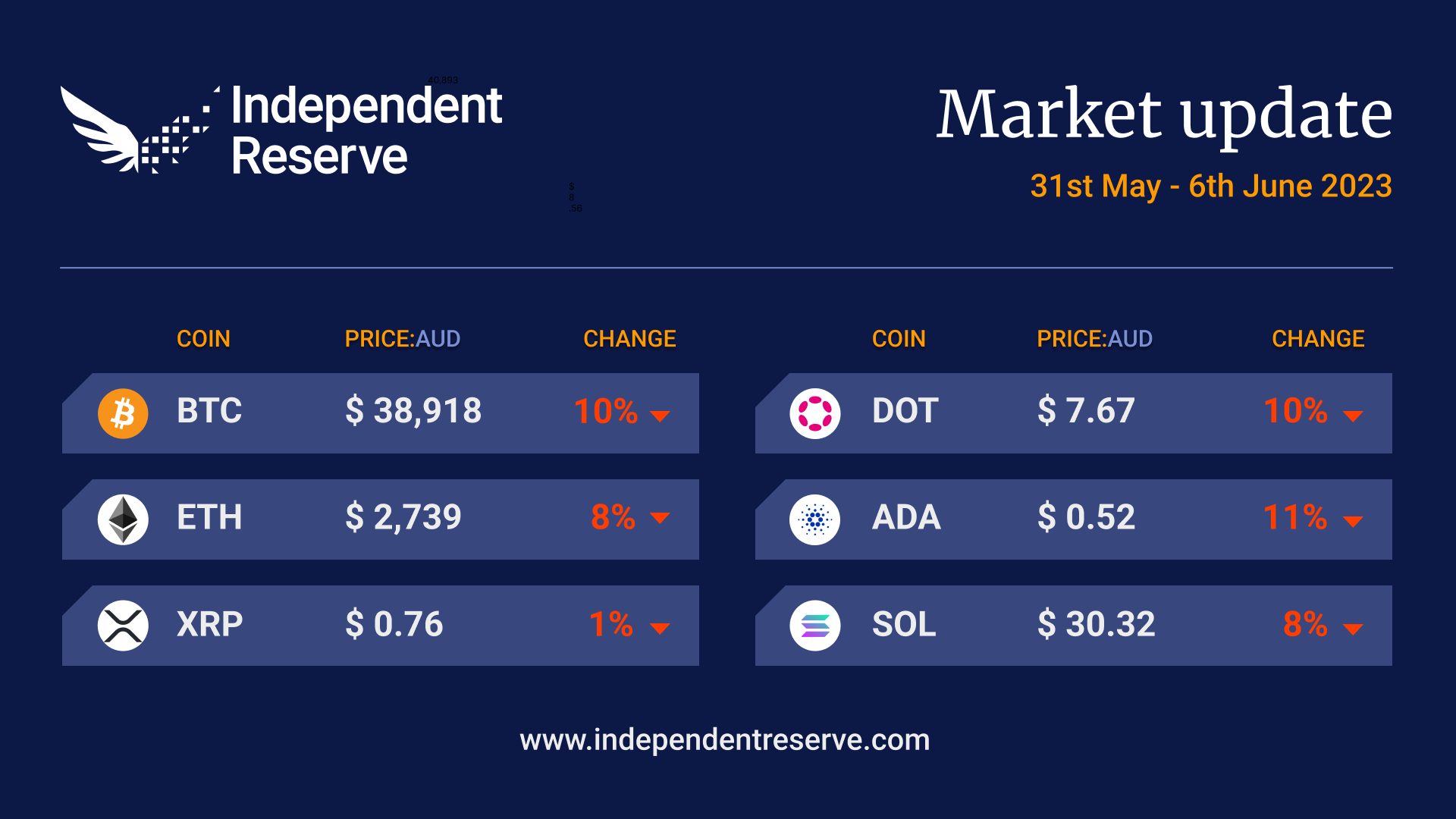

Excitement has returned to crypto markets, but it’s the bad kind, with the SEC suing Binance. Australia’s CPI also rose to 6.8% and Deutsche Bank has forecast three more rate rises this year. There was some good news, in that the debt ceiling deal passed in the US, and will shave off “a few tenths of a percentage point” of the annual US deficit. Bitcoin plunged 5% in an hour on the Binance news, with analyst Marcel Pechman saying Bitcoin could test the US$25K resistance last seen in mid-March. At the time of writing Bitcoin was down 10% for the week to trade around A$38,918 and Ethereum was down 8% to trade around A$2,739. XRP was down 1% for the week, but Cardano fell 11%, Polygon lost 10%, and Solana lost 8% — all three were labelled securities by the SEC. Dogecoin was down 9.2% and the Crypto Fear and Greed Index is at 53 or Neutral, but expect that to fall.

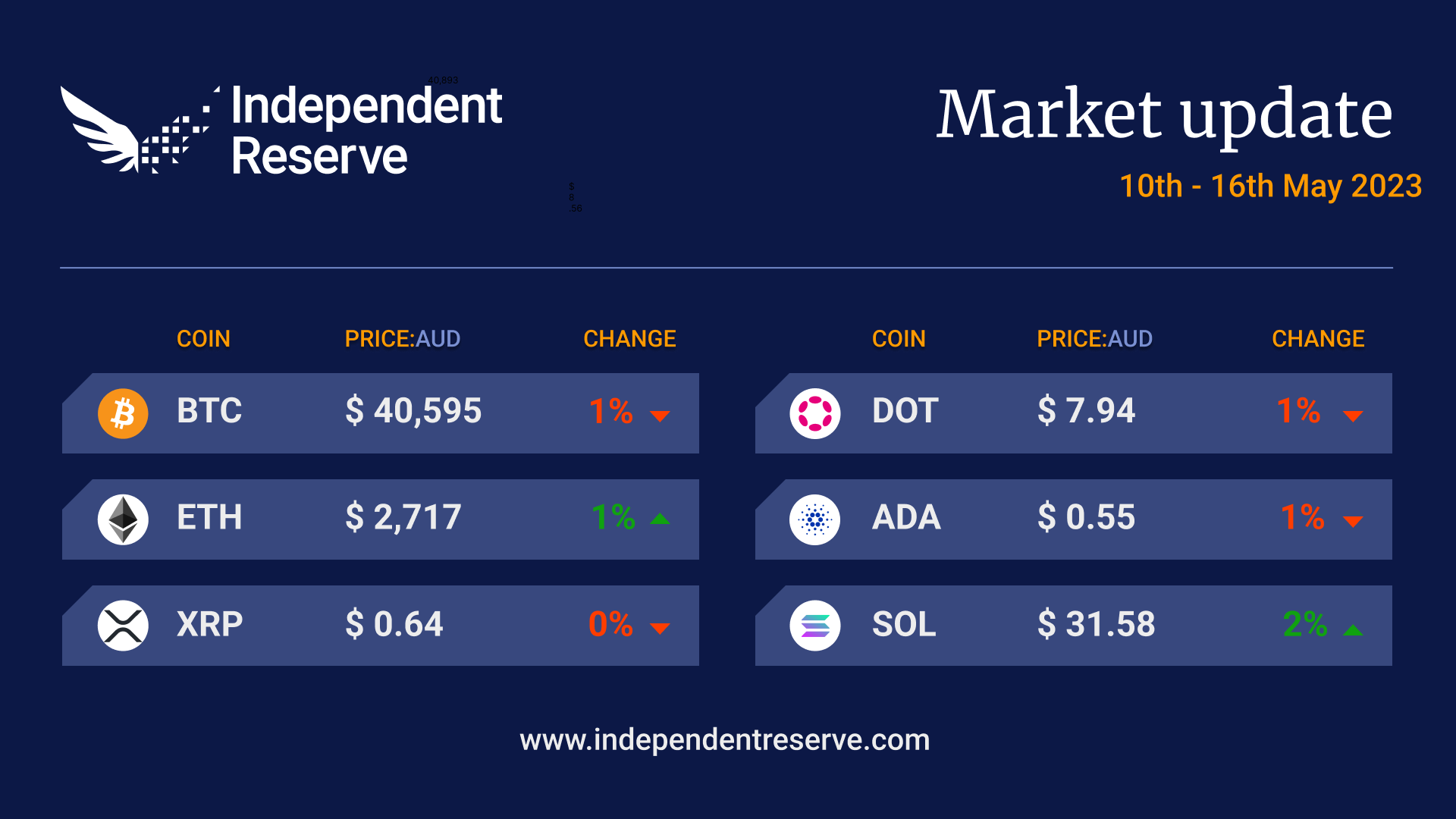

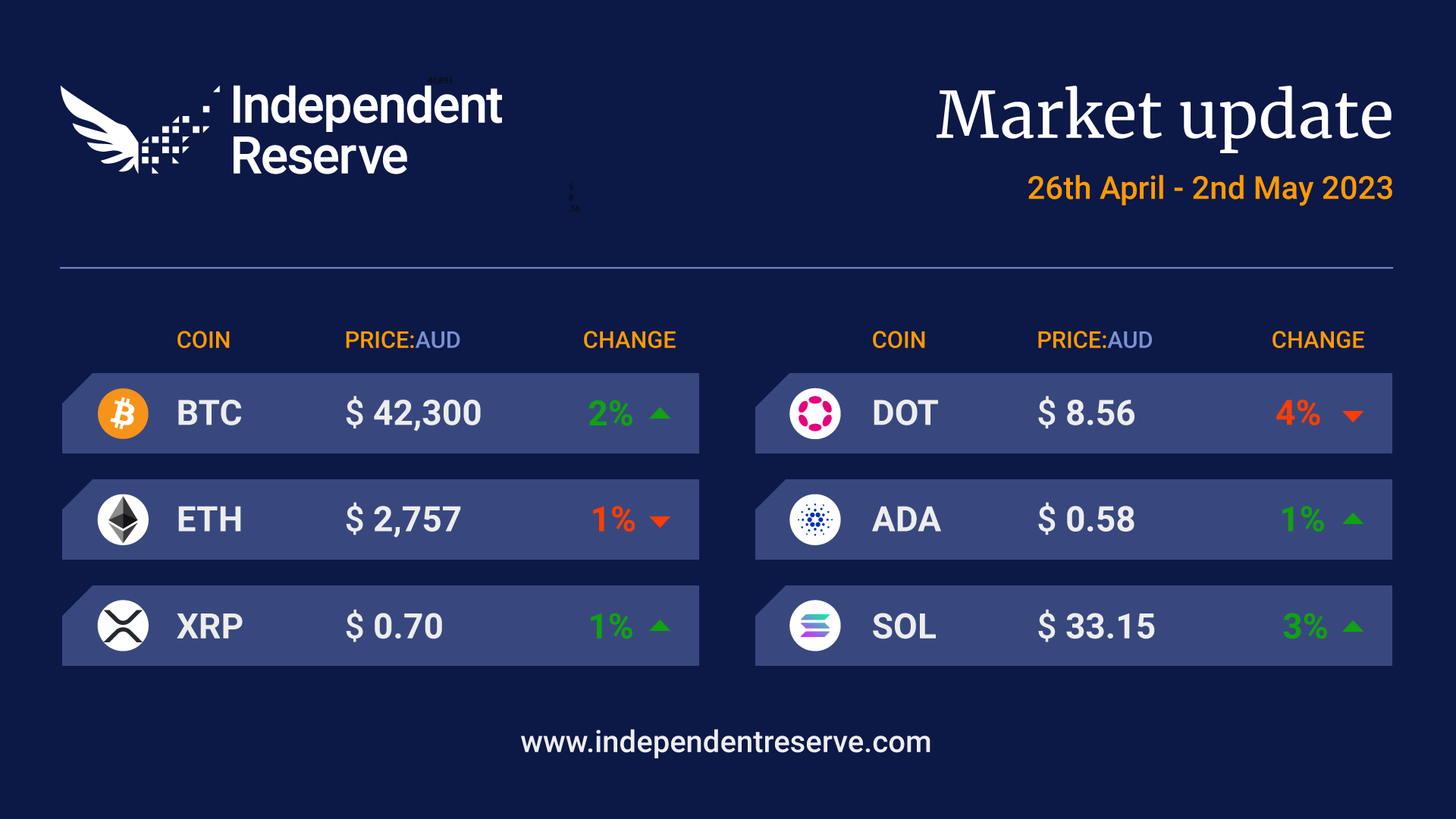

Hong Kong’s new crypto rules and the likelihood a US Government shutdown will be averted gave Bitcoin a 4.4% boost late in the week to A$43,150 (US$28,360), but the bulls haven’t convinced us they’re back in charge and Decentrader reports lots of traders are adding shorts. Analyst Michael van de Poppe believes sentiment is too bearish. “Retail is so extremely bearish on #Bitcoin and #Crypto, it’s almost insane. People are stuck in the 2022 mindset.” The in-principle debt limit deal could still fail to gain enough approval (as it has opponents on both sides), interest rates could rise further and the AI hype powering share markets could moderate, so it’s not a clear picture right now. Bitcoin finishes the week up 2.9% to trade at A$42,300 (US$27.7K) while Ethereum gained 4% to trade around A$2,895 (US1,893). XRP was up 6.6%, Cardano (2.7%), Polygon (3.8%) while Dogecoin was flat. The Crypto Fear and Greed Index remains at 52 or neutral.

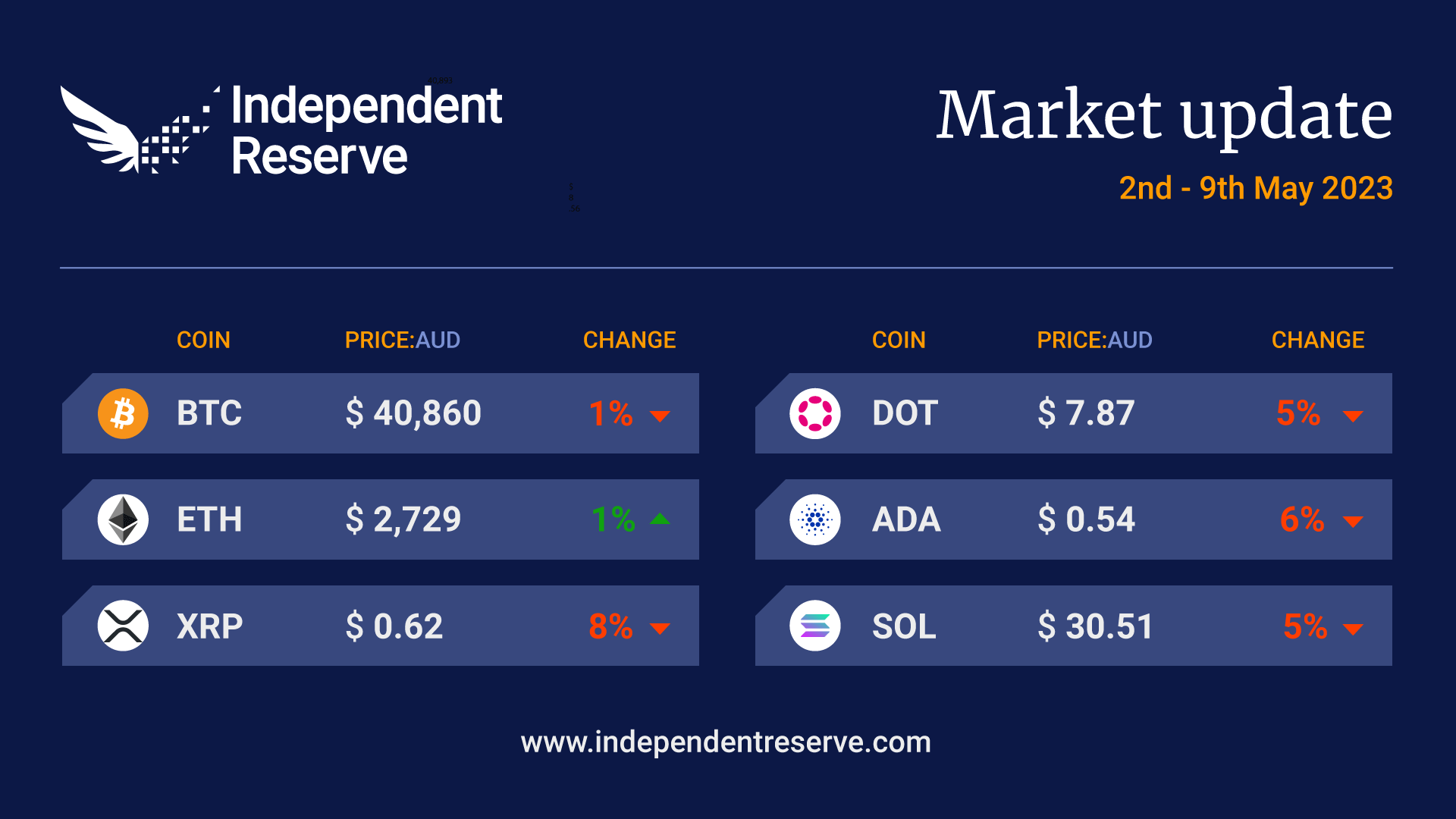

Crypto markets have been kind of dull lately, with low volatility and little of the usual drama. According to the chart whisperers, the trend is slowly down with Bitcoin in a descending wedge formation since mid-April, with the total market capitalisation for crypto down to A$1.69 trillion (US$1.125T). Analyst Marcel Pechman suggests this bearish formation could last until mid-July. Veteran trader Tone Vays calls it a frustrating “consolidation” but suggests US$34K (A$51.1K) is on the cards in the near term as the halving is less than a year away. Bitcoin consolidated within a tight range of 3.4% over the week, and finishes 1.7% down on the same time seven days ago to trade around A$41,000 (US$27,300). Ethereum was pretty much even at A$2,800 (US$1,850). Ripple gained 8%, Cardano (-1%), Dogecoin (-9.1%) and Polygon (-14.7%). Fittingly, the Fear and Greed Index is at 49 or Neutral.

Bitcoin didn’t look healthy this week, dipping to two-month lows under A$39.1K/US26K a few days ago. Depending on who you talk to, Bitcoin’s chart either looks like a classic bearish head and shoulders pattern, or we’re about to see a short squeeze and shoot upwards. Bitcoin finished the week down 1.2% to trade around A$40,650 (US$27.5K) and Ethereum was down a similar amount to trade around A$2,710 (US$1,820). XRP and Dogecoin were flat, Cardano gained 1.4% and Solana rose 2.4%. The Crypto Fear and Greed Index is at 50, or Neutral.

Bitcoin again faced resistance at the A$44.2K (US$30K) mark and finishes down 1.5% on seven days ago to trade around A$40,950 (US$27.6K), with the blockchain groaning under the weight of memecoins, Ordinals and skyrocketing fees. Ethereum had a dose of nostalgia with surging fees like in the old days and finishes the week flat at around A$2,735 (US$1,855). The spectre of further banking collapses and the periodic game of chicken over lifting the US debt ceiling — a looming economic “calamity” according to Treasury Secretary Janet Yellen — are also weighing on markets. XRP lost 8%, Cardano fell 6%, Dogecoin was down 8.2% and Polygon lost 6.2%. The Crypto Fear and Greed Index is at 60 or Greed.

The takeover of First Republic Bank by JP Morgan appears to be causing volatility on crypto markets. Does the second largest US bank failure ever highlight that the crisis is getting worse (there’s a narrative this would be good for crypto), or is the fact the banking system has successfully navigated the challenge indicate things are stabilising? There’s not a lot of clarity just yet, and there are a multitude of other headwinds for crypto, including the regulatory crackdown in the US and the likelihood of a 25-basis point hike in US interest rates this week. Analyst Nicholas Merton’s “long term thesis” is that we “are still in a bear market and that this is an exacerbated relief rally of around 100% from those relative lows.” Bloomberg Intelligence analyst Mike McGlone says he’s “very bullish” on Bitcoin in the longer term but worries about “a rug pull in the stock market” sending prices below US$20K (A$30.2K). At the time of writing Bitcoin had fallen 4.7% in 24 hours, but was still up 2% on a week earlier to trade around A$42,240 (US$28K). Ethereum fell 3.6% in 24 hours but was roughly the same as a week ago at A$2,750 (US$1,830), XRP, Cardano and Dogecoin were all flat, and Polyon lost 3.1%. The Crypto Fear and Greed Index is at 63, or Greed.

Crypto Spring was lovely while it lasted, but the cold weather has returned once again. Bitcoin tumbled from more than A$45K (US$30K) a week ago down to A$40,600 (US$27.2K) but has since recovered to $42,600 ($28.3K). The price got a bump this morning after Fox Business journalist Charles Gasparino reported sources at First Republic Bank say Government receivership is likely due to a lack of interest from the private sector. Bitcoin is currently down 6.9% on a week ago. Ethereum lost 10.6% and is trading at A$2,810 ($1,860), Ripple was down 11.1%, Cardano lost 11.3%, and Dogecoin was down 14.6%. Confidence took a dive too, with the Crypto Fear and Greed Index falling to 53, or ‘neutral.’

There are mixed signs on the health of the US economy, with Morgan Stanley CIO Mike Wilson stating that a “credit crunch has started” due to a very sharp decline in lending related to the collapse of Silicon Valley Bank. Balancing that out, BlackRock CEO Larry Fink said that the large amount of stimulus flowing into the economy will prevent “a big recession” (though a small one will probably happen). We’ll get a better view of what’s happening soon, with Morgan Stanley, Netflix, and Tesla all set to report first-quarter results this week. Bitcoin threatened the US$31K mark (A$46K) but finished the week close to where it began at A$44K (US$29.5K). Ethereum surged to an 11-month high following its latest upgrade topping US$2,100 (A$3,130). It remains up 9.2% on last week at A$3,100 (US$2,080). XRP finished the week flat, Cardano gained 10.1%, Dogecoin (8.5%) and Polygon (3.3%). The Crypto Fear and Greed index is at 69 or Greed.

After trading around the US$28K (A$42K) mark for three weeks, Bitcoin surged overnight and has broken the US$30K barrier. US nonfarm payroll employment figures suggest unemployment is rising more slowly than predicted, which raised market expectations the Fed may hike rates again. However, the CPI figures due this week are expected to show inflation falling to 5.1% and, complicating matters even further, earning season is kicking off which could highlight weakness in the economy. Edward Moya, the senior market analyst at Oanda, told clients this week could be pivotal. “This is the week that could tell us that the US consumer is no longer showing resilience and in fact is rather weak,” Moya wrote. Michael Saylor’s Microstrategy bought another 1,045 BTC and now owns 1 in every 150 Bitcoin ever created. Bitcoin is up 8% on a week ago to trade at A$45k ($30.1K) while Ethereum was up 6.2% to trade at $2,895 (US$1,920). XRP gained 4.1%, Cardano (2%), Dogecoin lost 12.6% after the latest Elon Musk/Twitter pump subsided and Polygon gained 2.1%. The Crypto Fear and Greed Index is at 62, or Greed.