Market update

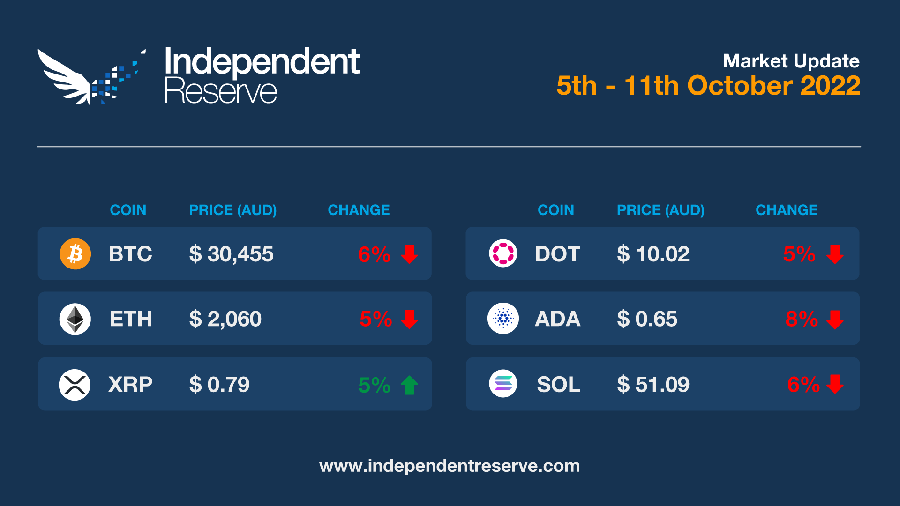

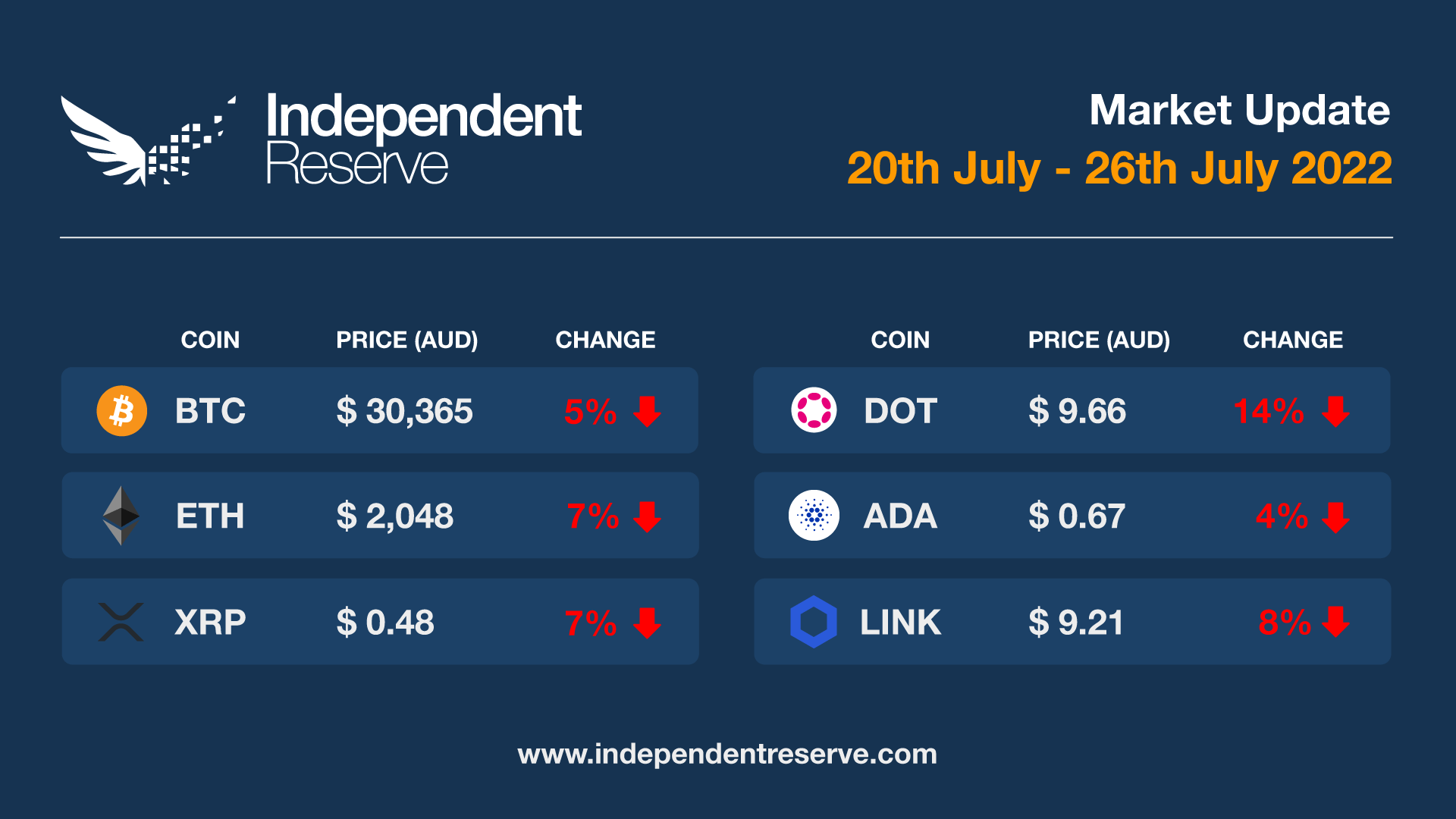

The S&P 500 has been on one of the longest slides in history and has dropped 24 weeks of the year in 2022, putting it second only to 1931 when it dropped for a total of 33 weeks (five years have seen worse total losses). Given all that, crypto isn’t doing too badly: Bitcoin dropped just 3.11% in September while the S&P 500 lost 9.34% and the Nasdaq lost 10.5%. It also outperformed most other asset classes throughout Q3. Bitcoin finishes the week 5.5% down at just over A$30,400 (US$19.15K) and Ethereum is down 5.4% to A$2,060 (US$1.3K). XRP gained 4.7%, Cardano lost 8%, Solana lost 5.9% and Polkadot -4.5%. In good news the total supply of Ether dropped 0.02% (annualised) in the past week, and we are 60% of the way to the next Bitcoin halving which historically always provides a bullish narrative. The Crypto Fear and Greed Index is at 24, or Extreme Fear.

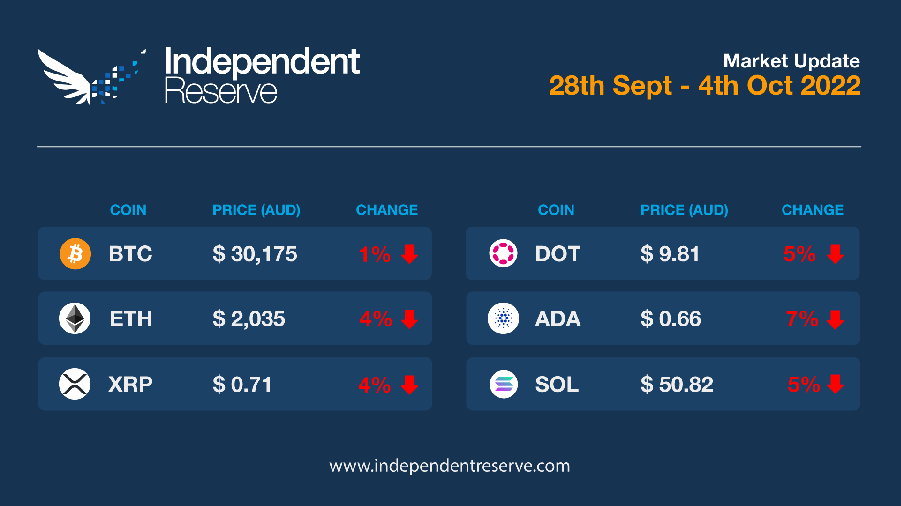

Sadly ‘Uptober‘ is in danger of being cancelled this year due to an ocean of grim economic news. The UK has begun emergency money printing again after the pound hit near parity with the US dollar, the UN is warning that interest rate hikes to tame high inflation could spark a global recession and an ABC reporter tweeting a rumour about an unnamed investment bank “on the brink” sparked fears that Credit Suisse or Deutsche Bank is about to collapse in a new Lehman Brothers moment (he has deleted it and the ABC is not at all pleased by the attention). The Reserve Bank is also due to hike rates again today, the only question is by how much, and are we in danger of one hike too many? Despite the news, Bitcoin finished flat to trade at just over A$30,000 (US$19,550), while Ethereum was down 4% to trade just over $2,020 (US$1,320). XRP lost 4%, Cardano (-7%), Solana (-5%) and Polkadot finished -5% for the week. The Crypto Fear and Greed Index is at 24 or Extreme Fear.

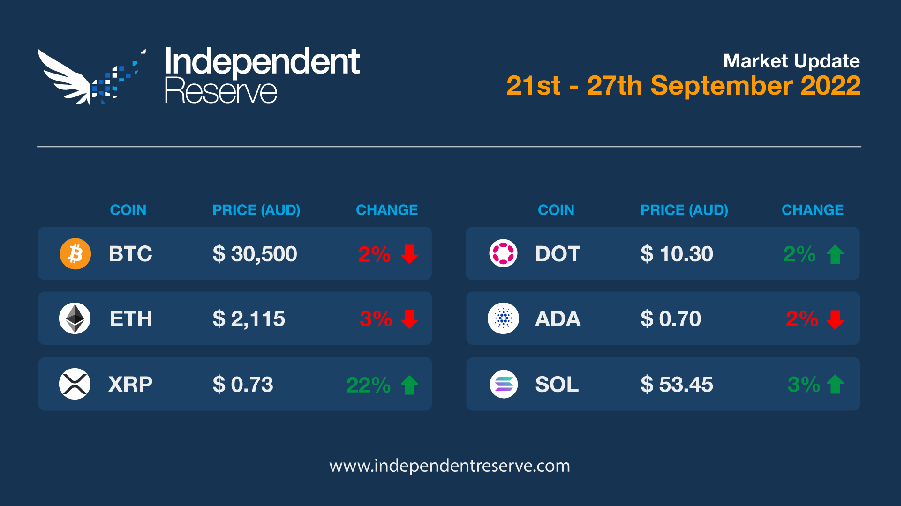

Crypto markets are still bearish after the Federal Reserve hiked interest rates by another 75 basis points. Rates are now headed towards 4.6% and the Fed is sounding very hawkish on bringing inflation down. A turnaround doesn’t seem likely in the short term with Glassnode’s latest report noting that rising volumes amid a bearish trend are a bad sign: “Whenever spot volume backs a downward trend, it tends to extend into the near future, and a reversion requires substantial buying pressure.” The good news however is that adoption continues to grow and the current Crypto Winter can’t last forever. At the time of writing Bitcoin was down 2% for the week to trade around A$30,500 (US$19.7K) and Ethereum had lost 3% to trade at A$2,115 (US$1,360). Despite the price dips, around 51% of ETH holders are currently still in profit. XRP shot up (22%) on speculation about a resolution of its court case, Cardano lost 2% and Dogecoin gained 3% after Ethereum cofounder and Doge fan Vitalik Buterin suggested it could move to proof of stake. The Crypto Fear and Greed Index is at 20 or Extreme Fear.

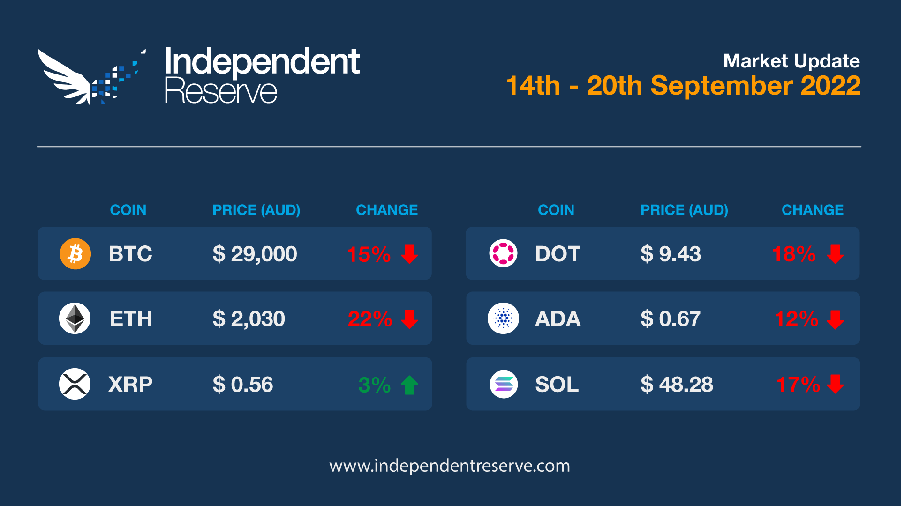

Interest around the Ethereum merge saw a massive increase in market volume, with the seven day moving average spiking from A$26.7B (US$18.1B) on September 6 to A$42.8B (US$28.8B) on September 16. Unfortunately, everything tanked after the merge on macroeconomic news with inflation running at 8.3% in the US and markets bracing for a 0.75% to 1% rate rise. Bitcoin dipped as low as A$27.6K (US$18.5K) and finishes the week down 15% to trade around A$29,000 (US$19,450). Ethereum is back to mid-July prices, sliding 22% to A$2,030 (US$1,365). XRP was up 3% on hopes of a court victory against the SEC, Cardano fell 13%, Solana (-15%) and Dogecoin (-11%). The Crypto Fear and Greed Index is at 21, or Extreme Fear.

After a lacklustre few weeks, Bitcoin suddenly shot up 10% on the weekend due to a reported short squeeze. MicroStrategy announced its doubling down again, major buying from whales, and positive signs on traditional markets. Bitcoin is trading just over A$32,200 (US$22.2K) to be up 7% for the week (though it’s still lower than mid-August). The impending Ethereum merge (Google has thoughtfully created a countdown clock) has the token trading flat for the week to sit around A$2,500 (US$1,720). Positive sentiment could come to a screaming halt with the imminent release of the US inflation figures this week and a possible “sell the news” reaction following the Merge. XRP was flat, Cardano (-5%), Solana (+7%) and Polkadot (-4%). The Crypto Fear and Greed Index is at 25, or Extreme Fear.

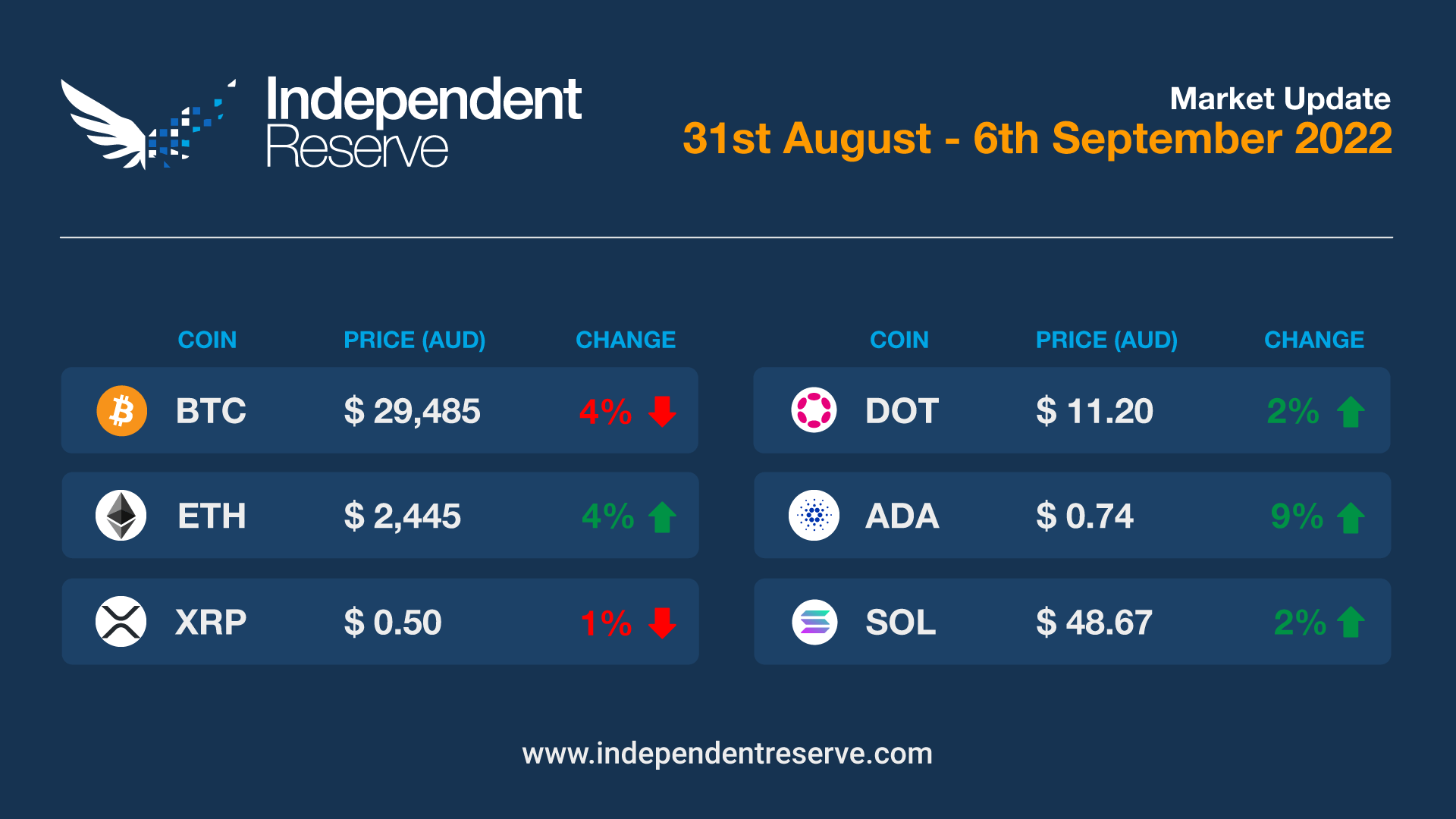

Septem-bear is generally a pretty rubbish month for Bitcoin prices, with nine out of the past 12 years seeing prices finish in the red. The three outliers saw only modest gains too, apart from one outlier year where it increased 15%. On average Ethereum loses 12% in September and the overall crypto market cap loses 7.5%. Spiralling energy prices, the US dollar hitting new highs and sentiment tanking don’t seem to suggest this month will buck the trend either. The Bitcoin price has just been crawling sideways for the past week, trading in a $1,000 range. It finishes the week down 4% to trade just around A$29,500 (US$20,100). Ethereum increased 4% to trade around A$2,450 (US$1,665). Cardano leapt 9% on the news the Vasil hard fork has a date while XRP and Solana were flat. The Crypto Fear and Greed Index is at 23, or Extreme Fear.

Markets fell this week after Federal Reserve chair Jerome Powell indicated the Fed will continue its aggressive approach to curb inflation despite the “unfortunate costs.” “A failure to restore price stability would mean far greater pain,” he said. Bitcoin plunged below the US$20K mark (A$29K), the S&P 500 fell 3.4% on Friday while A$46B was wiped from the Australian sharemarket on Monday. The local market is also bracing for another half a percentage point interest rate rise next Tuesday. Bitcoin is currently down 8% for the week to trade around A$29,300 (US$20.2K) while Ethereum has fallen 9% to trade around A$2,240 (US$1,540). Most other coins fell including XRP (-6%), Cardano (-6%), Solana (-12%) and Polkadot (-6%). Synthetix climbed 17.8% on the back off news it can now survive on actual revenue. The Crypto Fear and Greed Index is at 24 or Extreme Fear.

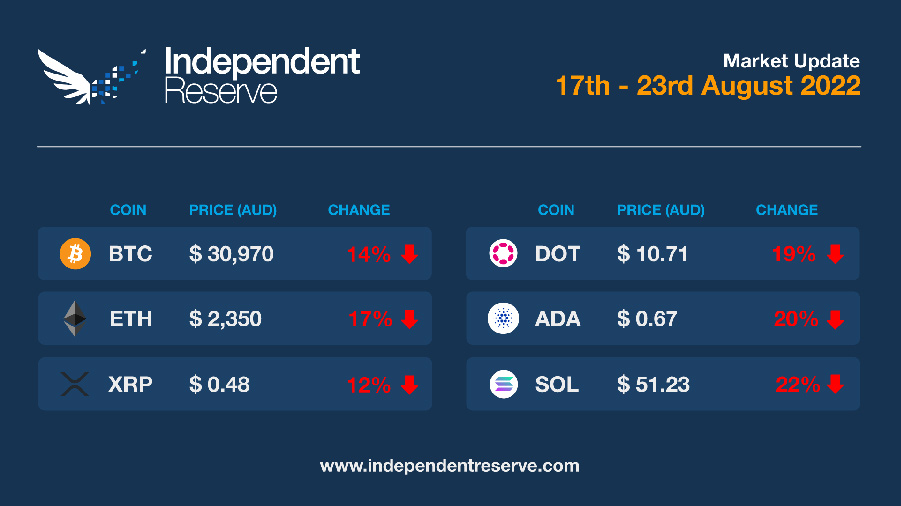

The bear market rally ran out of puff on Friday with Bitcoin falling below the 200-week moving average. It’s currently down 14% for the week and trading around A$30,970 (US$21.3K). Ethereum fell 17% to trade around A$2,350 (US$1,620), possibly related to fears over decentralisation and transaction censorship in the fallout from the Tornado Cash sanctions. Traditional markets are in the red too due to macro factors including comments by the Federal Reserve Bank of St. Louis President James Bullard who said he favoured a 75-basis point hike in interest rates next month. The last hike of that magnitude saw crypto market turmoil. Everything else was down on the week, with XRP falling 12%, Cardano (-20%) and Polkadot (-19%). The Crypto Fear and Greed Index is at 29 or Fear, down from 45 last week.

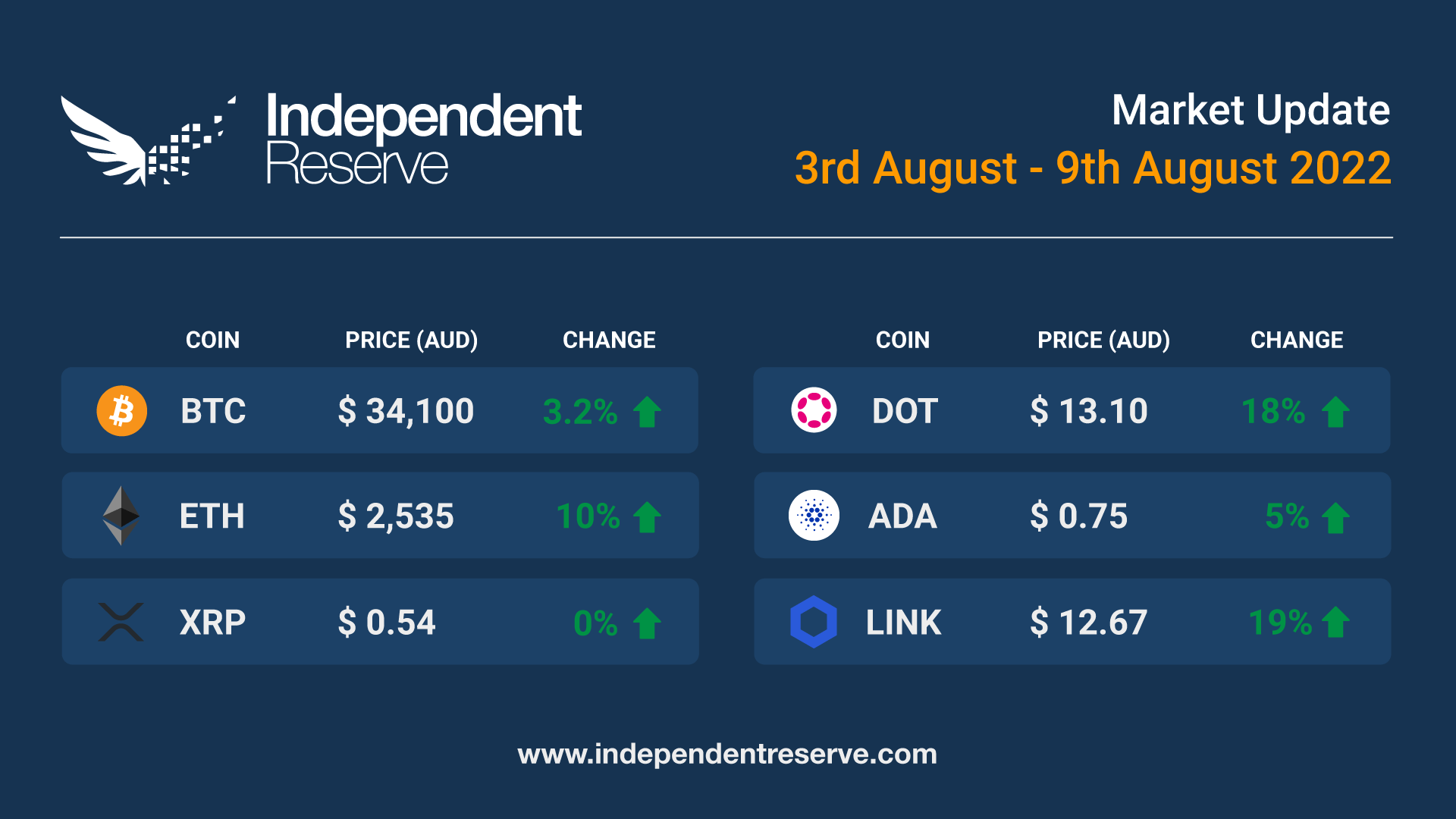

Ethereum reclaimed the US$2,000 (A$2,850) mark briefly on the weekend for the first time since May following news the Merge is just one month away. It’s currently trading around US$1,900 (A$2,720) marking a 7.7% gain for the week. Bitcoin is also up 1.1% on seven days ago to trade around US$24K (A$34.3K). Cardano increased 3.1%, with co-founder Charles Hoskinson insisting that testing on the delayed Vasil hard fork is going well. XRP lost 1.1%, Solana increased 3.8% and Dogecoin was up 10.4%. The Crypto Fear and Greed Index hit Neutral this week for the first time since April but is currently at 45 (Fear). Interestingly, the Bank of America’s Bull and Bear Indicator for traditional markets has been stuck at 0 or ‘extreme bearish’ for nine weeks in a row. Analyst Jack Dorman argued this week that while Bitcoin is still correlated with the Nasdaq, other digital assets including blue chip DeFi coins and Ethereum decoupled months ago.

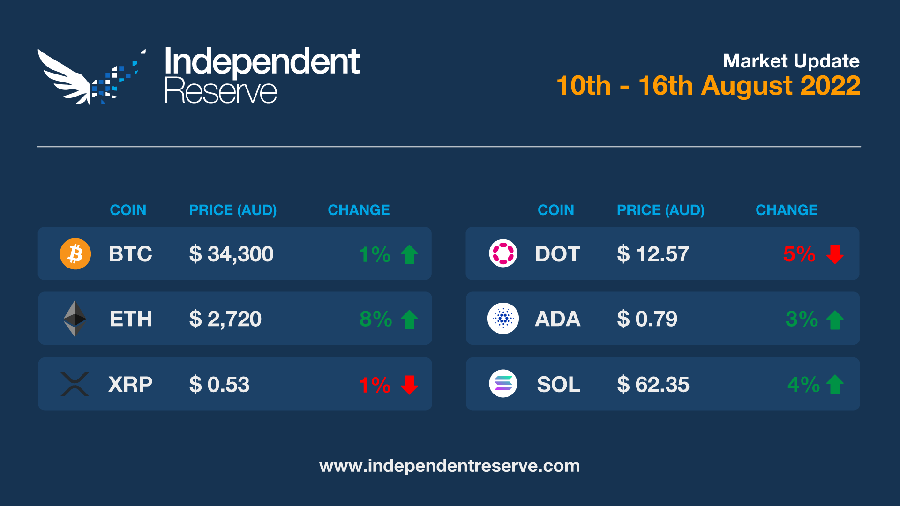

In the week just past, BTC has been range-bound – stuck in a channel 4% wide. Last night there was an attempt to break out to the upside, but as most of this has been given back, we resume the “crab” market. Bitcoin is currently up 3.2% to trade around A$34k (US$23.7k), Ethereum continues its merge exuberance and is trading 10% up – currently A$2,526 (US$ 1,765). XRP is flat, Cardano is up 5%, Solana (2.4%), Dogecoin (3.5%). The Crypto Fear and Greed Index is at 42, and while technically “Fear”, this is on equal footing with high on the 30th July, and the highest it’s been since April.

Brace yourself for a potentially bumpy week with the US Federal Reserve expected to hike interest rates by 75 basis points, and the release of the Q2 US Gross Domestic Product figures potentially showing a recession (two quarters of negative growth). Australia’s inflation rate figures also come out and are expected to be awful, and a bunch of big tech company earnings reports are coming out too. Perhaps in expectation of possible bad news, everything has fallen considerably in the past 24 hours. Bitcoin finished the week flat at just over A$31,000 (US$21.5K), while Ethereum was down 1.1% to around A$2,120 (US$1.5K). The imminent Vasil hard fork saw Cardano gain a modest 1.8% while Ripple fell 4%, and Dogecoin lost 3.1%. After a record 73 days at Extreme Fear, the Crypto Fear and Greed Index returned to simply Fear this week, and it’s currently at 30 (Fear).

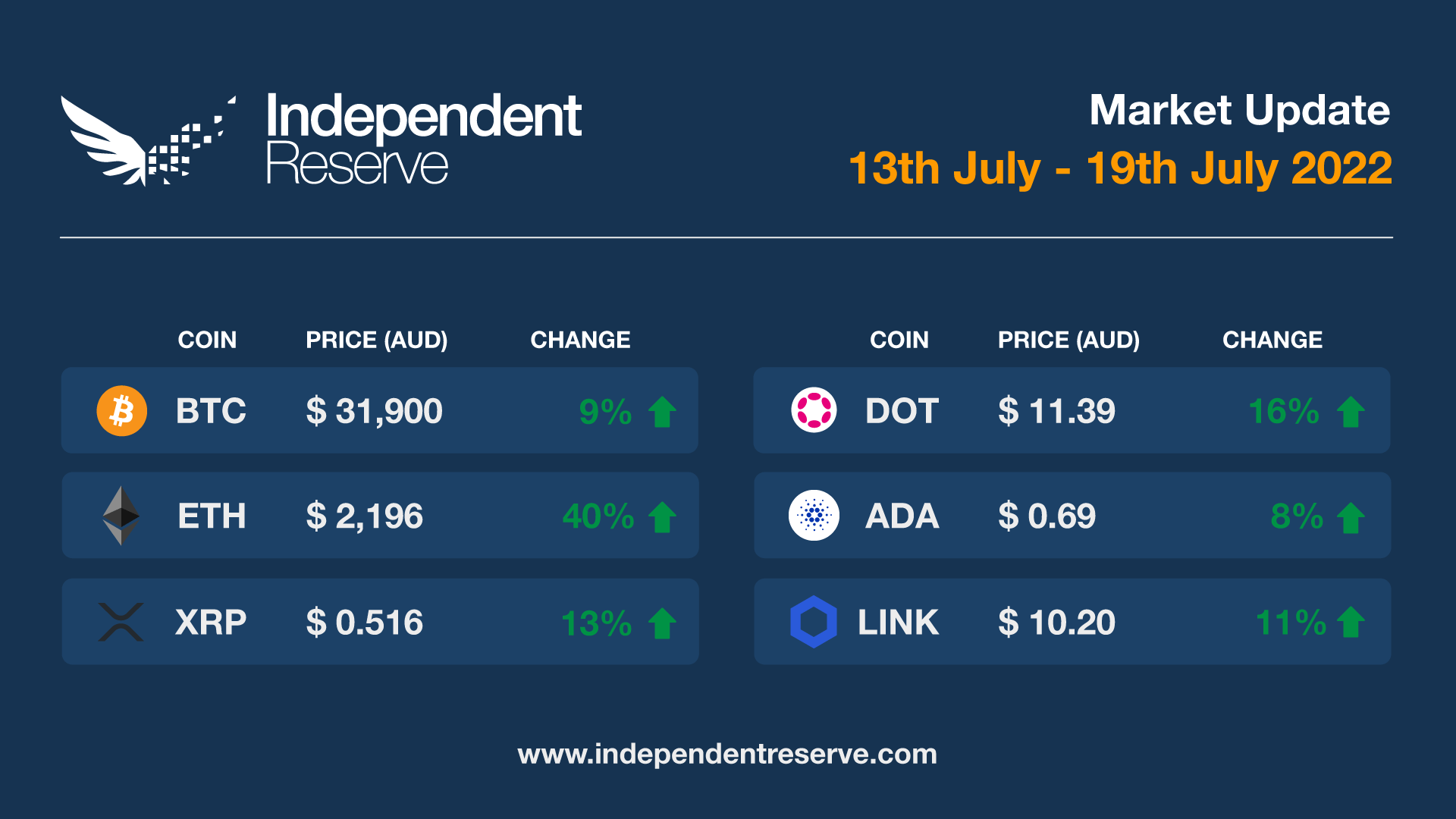

Crypto markets turned around this week, thanks to a bullish narrative that the Ethereum Merge will actually happen in September, and perhaps guarded optimism from some in traditional markets that inflation may have peaked in the US at 9.1% due to falling commodity prices and supply chains clearing up (plenty of others think that idea is totally wrong, however.) The overall crypto market cap has returned above the US$1 trillion mark (A$1.47T), leading to loose talk about a new bull market. It’s worth noting that the market is still down US$2T (A$2.93T) from November’s peak, and Glassnode points out that the average time Bitcoin normally trades below the realised price during a bear market is 197 days. The current bear has just 35 days on the clock. Still green is good, and Bitcoin finishes the week up 9% at A$32,070 (US$21.7K), while Ethereum has shot up 40% to A$2,200 (US$1,500). Ripple (XRP) was up 13%, Solana jumped 28%, and Dogecoin increased 6.6%. The Crypto Fear and Greed Index is at 20 – that’s still Extreme Fear but a lot higher than one month ago when it was 6.