Market update

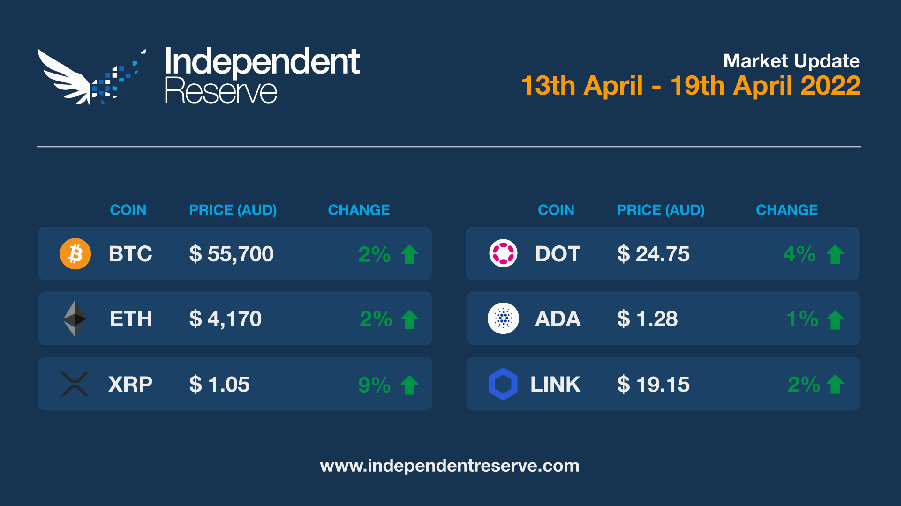

In the absence of a clear overall bullish or bearish narrative driving the Bitcoin price firmly up or down, the price has been meandering above and below the US$40K mark (AU$54.4K) for most of 2022. Bitcoin dropped below that level a few times this week, but finished up 2% to US$41K (AU$55.7K). Ethereum was up 2% to just over US$3K (AU$4,100). Promising signs in the SEC case against Ripple helped XRP to gain 9%, Cardano was flat and Polkadot gained 4%. The Fear and Greed Index is at 24, or Extreme Fear.

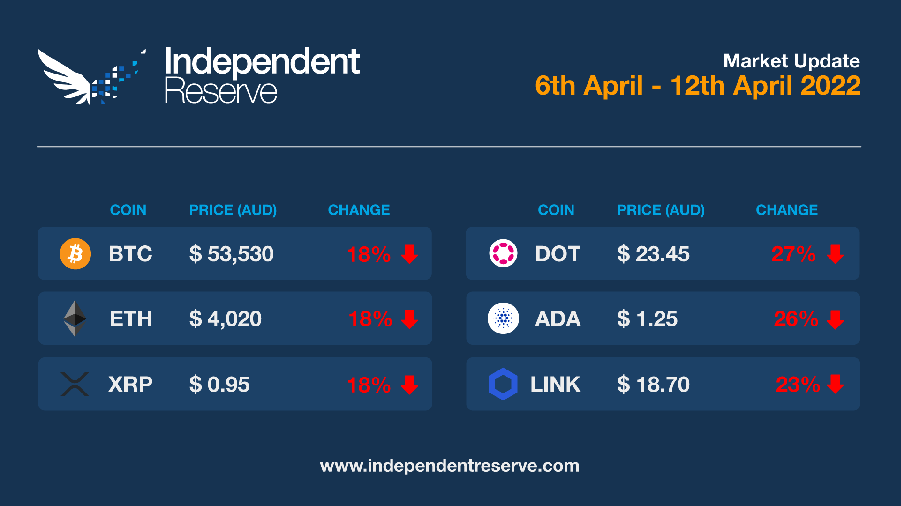

In crypto’s ongoing game of snakes and ladders, we’ve just hit a ladder, with Bitcoin down 8% in the past 24 hours and 18% down for the week to trade around AU$53,500 (US$39,600). The overall crypto market cap is down to AU$2.46T (US$1.82T). Pundits point to Bitcoin’s increasing correlation with equities markets as a possible explanation – the correlation is at the highest point since October 2020 and all the major US markets were down on Monday, with the tech heavy Nasdaq losing 2.2%. The Ukraine war, interest rates, and inflation are weighing heavily and former BitMEX CEO Arthur Hayes thinks it’ll get worse before it gets better, tipping BTC will test US$30K (AU$40.4K) and ETH US$2,500 (AU$3,370) before the end of June. Ethereum lost 18% this week to trade just over AU$4,000 (US$2,960) and everything else lost ground including XRP (-16.7%), Polkadot (-27%), Cardano (-26%) and LINK (-23%). The Crypto Fear and Greed Index is at 32, or Fear, though expect that to dip further today.

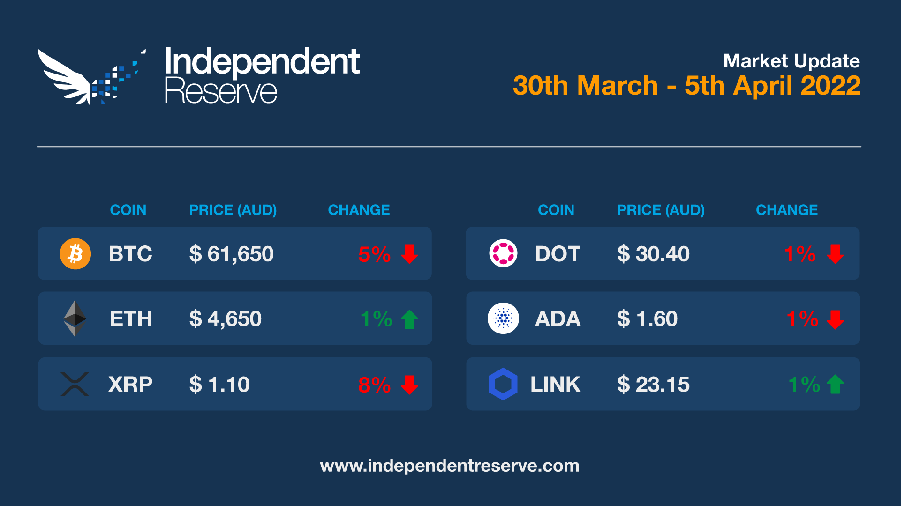

After a shaky first quarter, Bitcoin hit a new high for the year on March 29 around AU$65.6K. Glassnode reports that over the past week a net US$1.5 billion (AU$2B) worth of Bitcoin and US$1.7B (AU$2.25B) of Ethereum departed exchanges, while a net US$451.8M (AU$599M) of USDT flowed in. The Bitcoin price however finished the week down 5% at AU$61,650 (US$46.5K), while Ethereum increased 1% to AU$4,650 (US$3.5K). Cardano was down 2%, XRP lost 8% and Dogecoin also finished flat despite a spike in the aftermath of Elon Musk buying a slice of Twitter. The Crypto Fear and Greed Index is at 52, or Neutral.

Normal service has resumed, with Bitcoin now up by 35% since Russia’s invasion of Ukraine tanked markets in February. Analyst Will Clemente observed: “Bitcoin has closed above short term holder cost basis for the first time since Dec. 3. Hard to be bearish as long as BTC is above.” Tether just printed 1 billion USDT in four days, Ethereum gas fees for DeFi transactions are back around US$20 (AU$27) and memecoin insanity has returned because of course there’s already a Will Smith slap token and a DAO. The BTC price is up a whopping 11% since this time last week and currently sits at around AU$63,000 (US$47,100). Analysts who were bearish recently, are now talking about a new all time high. Ethereum gained 11% and is trading around AU$4,500 (US$3.3K), XRP was flat, Cardano added 24% and Polkadot was up 13%. The Crypto Fear and Greed Index is at 60, or Greed, for the first time in March.

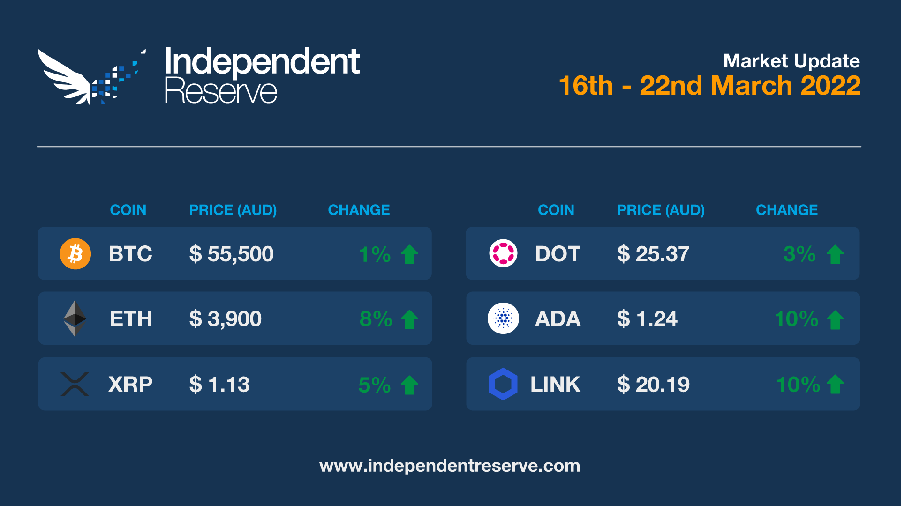

With the market growing more accustomed to the Ukraine war, and inflation and interest rate rises, the Crypto Fear and Greed Index has recovered slightly to 30, or simply ‘Fear’. Bitcoin has spent most of the week in the mid AU$50Ks, and it’s currently 1% up on seven days ago to trade around AU$55,500 (US$41K). With signs the years-in-the-making Merge is finally coming closer to reality Ethereum jumped 8% to trade at AU$3,900 (US$2.8K). Separately, XRP increased 5% and Cardano and LINK are up 10%.

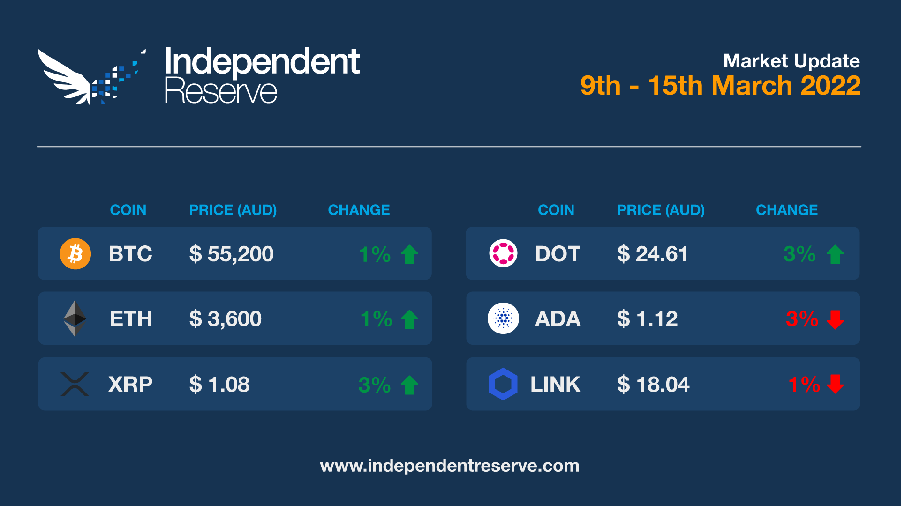

With inflation at a 40 year high in the US, and the Federal Reserve expected to start raising interest rates this week, Bitcoin’s ‘inflation hedge’ narrative is being put to the test. After a short-lived sugar rush from President Biden’s Executive Order, Bitcoin spent most of the week trundling along under US$40K (AU$55.6K), and it is currently flat on the last seven days, trading just around AU$55,200. Ethereum was up 1% to around AU$3,600 (US$2.5K), XRP gained 3%, Cardano is down 3% and Polkadot is up 3%. The Crypto Fear and Greed Index is at 23, or Extreme Fear, the same as last week.

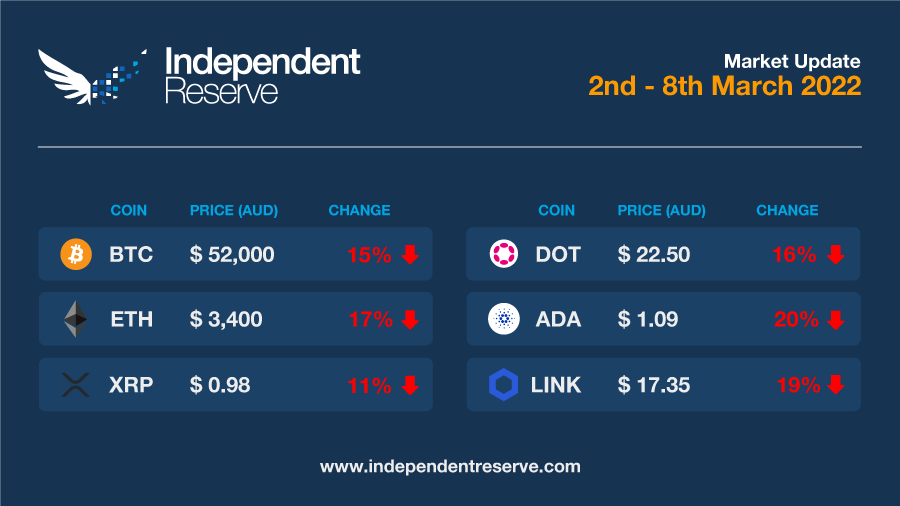

With the possibility of a nuclear exchange (relatively) high, a financial war ramping up, and increased regulatory pressure in the US and Europe, crypto markets are again under pressure. Bitcoin is down 15% for the week to trade just under AU$52K (US$38.3K) while Ethereum’s slide continues, losing another 17% to around AU$3,400 (US$2.5K). XRP lost 11%, Cardano (-20%) and Polkadot (-16%). The Crypto Fear and Greed Index moved above 50 earlier in the week but is now back around 23 or Extreme Fear.

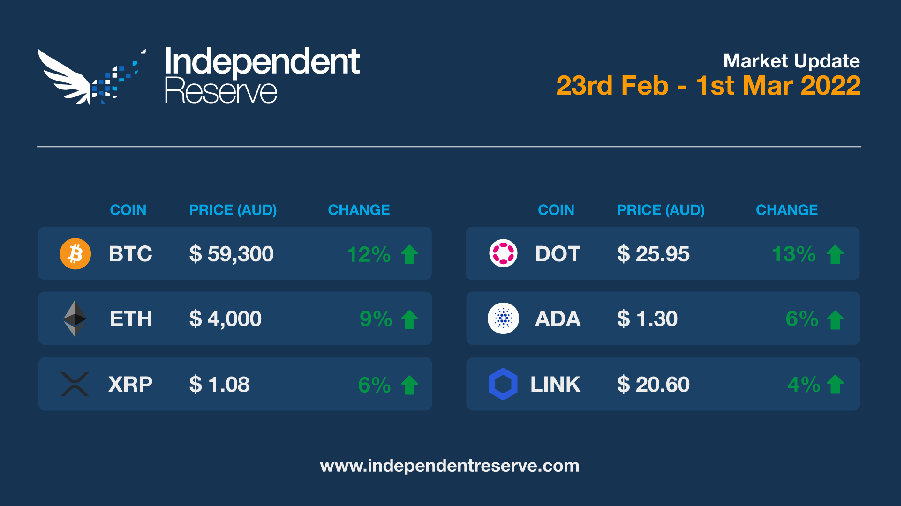

Bitcoin went on a rollercoaster ride this week, plunging more than 10% on the news that Russia had invaded Ukraine. It bottomed out below AU$48,000 (US$34K), recovered a little bit as markets digested the implications, and then suddenly jumped almost 15% in the past 24 hours to AU$59,300 (US$43K). As usual, the reasons aren’t exactly clear but there are reports Russians are buying up crypto as the country’s financial system gets hit hard by sanctions. Markets also seem to prefer certainty to uncertainty and news emerged today that eBay is looking at adding crypto payments. Bitcoin is up 12% for the week at the time of writing, with everything else up too including Ethereum (9%), XRP (6%), Cardano (6%), and Polkadot (13%). The Crypto Fear and Greed Index is at 20, or Extreme Fear. Bitcoin dominance is edging back towards 44%, the highest it’s been since November, and there are now 800K wallets with at least one whole Bitcoin, and non-zero addresses are at an all-time high above 40 million.

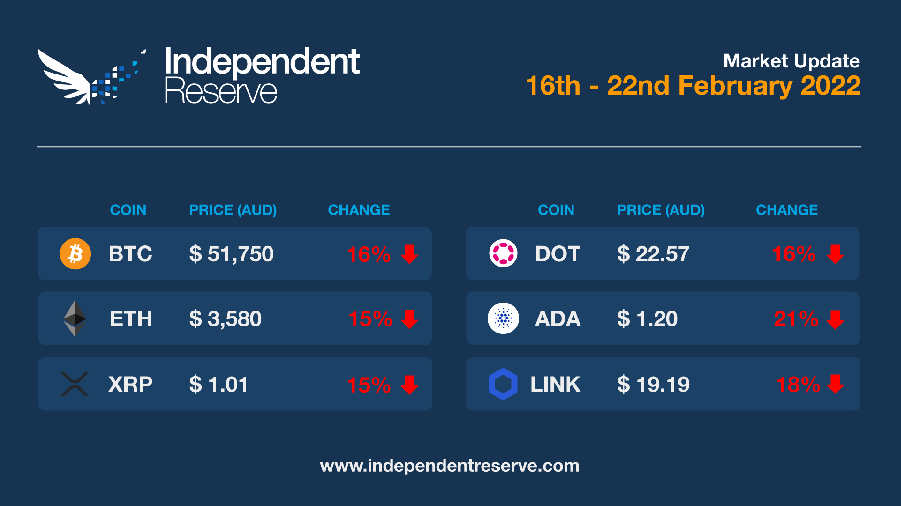

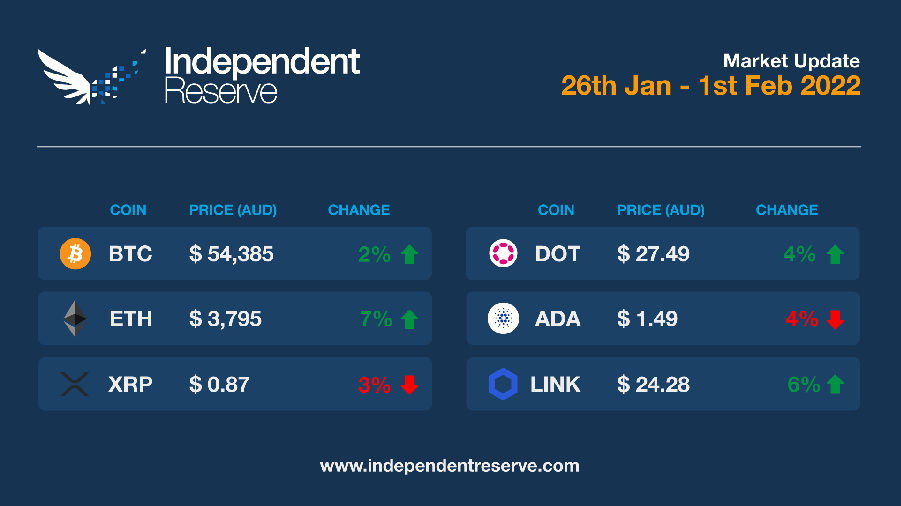

The year started with a US$2.21 trillion (AU$3.1T) crypto market cap but it’s declined 25% since and hit US$1.69 trillion (AU$2.35T) as of today. The threat of regulatory clampdowns and the possibility of war with Ukraine is weighing heavily on markets. Bitcoin fell below the US$37K (AU$51.5K) mark earlier today and the Fear and Greed Index is at 25 or Extreme Fear. At the time of writing, Bitcoin is at AU$51.7K for a 16% loss this week. Ethereum lost 15% to trade just below AU$3,600, XRP fell 15% and Polkadot lost 16%. Activity on the Bitcoin network has fallen back to mid-2019 levels, from 400K daily entities transacting in November down to around 275K today “indicative of tepid demand from new users,” Glassnode commented. In more positive news, El Salvador’s GDP soared by 10.3% in 2021 for the first time, showing that at the very least the Bitcoin Law didn’t tank its economy.

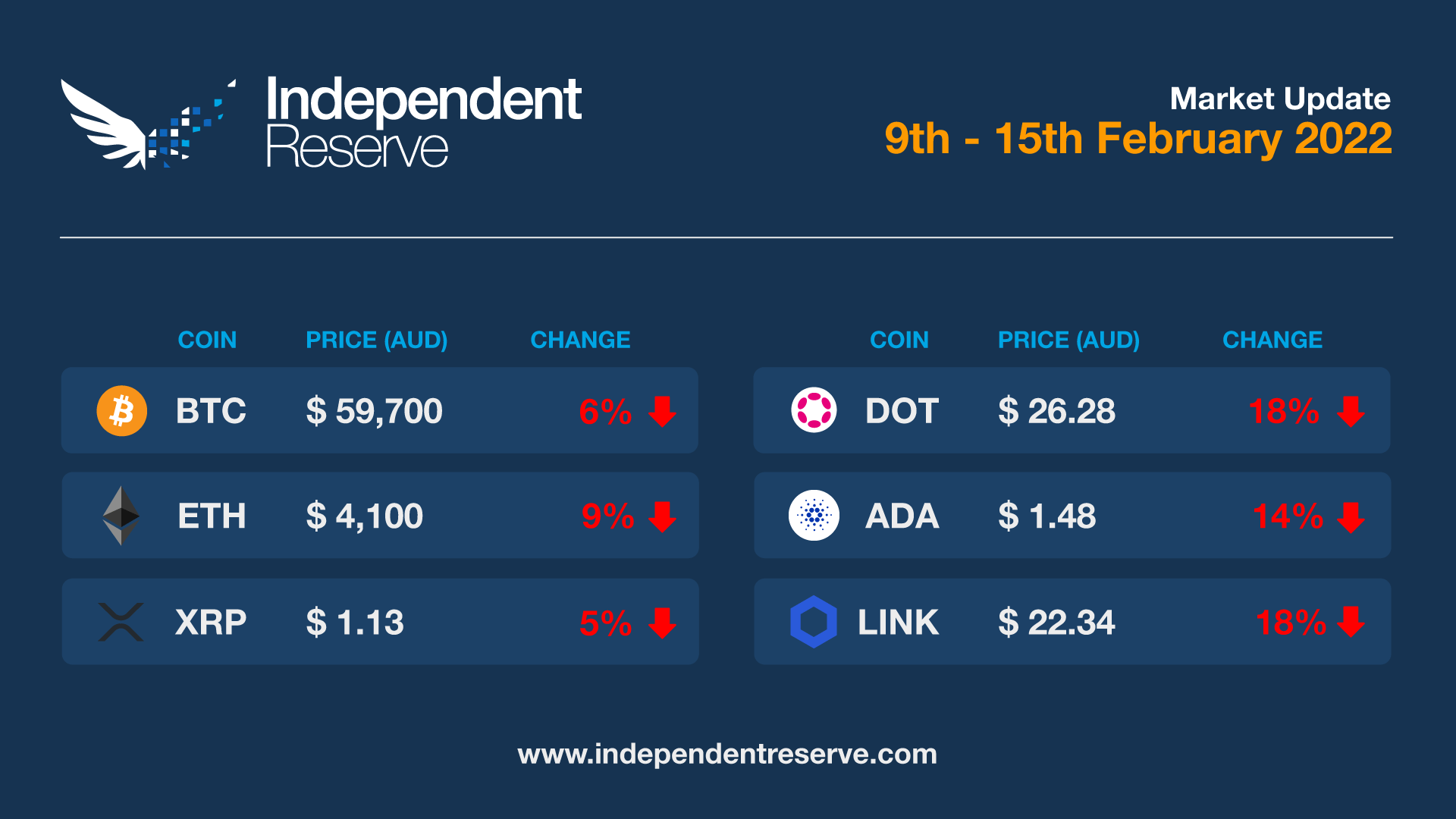

After an all too brief spell of fine weather last week, normal service has resumed, with Bitcoin falling 5.6% this week to trade around AU$59,700 (US$42.6K). Ethereum fell 9.2% to AU$4,100 (US$2.9K), while XRP was down 5.3%, Cardano (-14%), and Polkadot (-17.6%). The falls in crypto markets mirror falls in traditional markets which most blame on mounting fears of an imminent Russian attack on Ukraine. After hitting a local high of 54, the Crypto Fear and Greed Index has again fallen to 46 (Fear). In more promising news the Bitcoin hashrate has hit a new seven day average all time high of 201.3 terahashes per second (TH/s). It’s up 20% since the start of the year and peaked at 248 TH/s in the past 24 hours.

And just like that, ‘Crypto Winter 2022’ appears to have been just a couple of weeks of unseasonably cold weather. Of course, everything could still flip tomorrow, but the weather is fine and sunny this week with Bitcoin up 14.5% to trade around AU$62,000 ($US44K) and Ethereum up 13% to trade above AU$4400 (US$3.1K). Everything else was up by double figures, including Cardano (10%), XRP (29%), and Polkadot (11%). Influencer Lark Davis summed up the price action, tweeting yesterday: “Bitcoin has been in a downtrend since November, we have now broken out of that trend. Next stop? MOON.” The Fear and Greed Index has risen to 45 (Fear) – up from 26 last week – and the total market cap of all cryptocurrencies is up nearly half a trillion this week to AU$2.814T (US$2T).

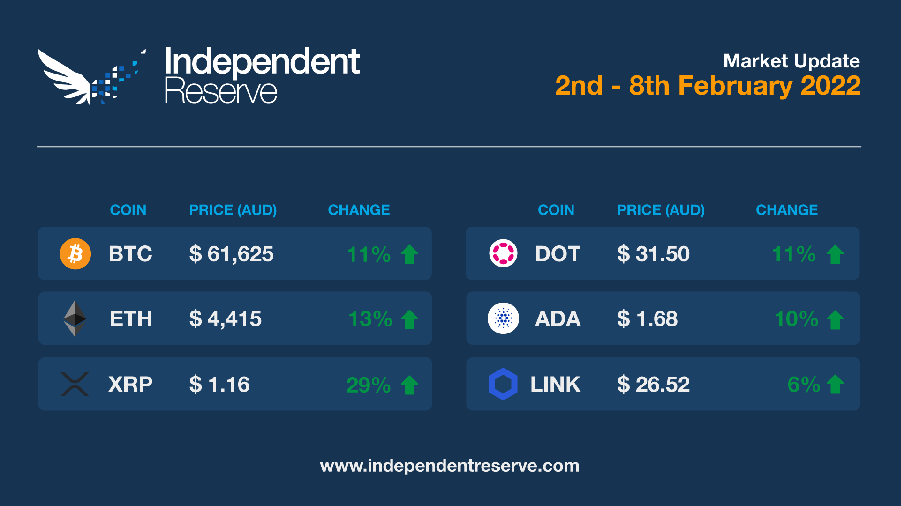

Let’s face it: January was not a great month for the crypto markets, with the market cap for all cryptocurrencies plunging from almost AU$3.2 trillion down to AU$2.47T today. It’s the worst start to a year since Crypto Winter began in 2018. There were only 11 green days this month and cryptocurrencies across the board lost double digits as prospective rate rises in the US spooked markets (here in Australia the RBA is expected to end the AU$4 billion a week bond buying program and open the door to interest rate rises after inflation reached the central bank’s target for the first time since 2014). Bitcoin is down 19.5% on a month ago, and Ethereum is down 29%. The good news is that February has started with a bounce and BTC is up 2% in the past week to AU$54,385 (US$38,475) and ETH is up 7% to almost $3,800. Cardano lost 4%, Ripple was flat and Polkadot increased 4%. The Crypto Fear and Greed Index is at 20, which is still ‘Extreme Fear’ but heading in the right direction after bottoming out last week around 11.